Saylor's Quotient

#94: Dumb Luck (Kodak), Big Beats (Celsius), and Perpetual Premiums (MicroStrategy)

Dumb Luck

In late January, I bought some shares of the Eastman Kodak Company (KODK). I don’t recall how I stumbled upon it, but on some basic metrics the company looked cheap (~4.0x trailing P/E, 0.3x book value). Kodak had posted some real earnings in recent quarters, and seemed to have enough cash lying around to keep it afloat. Plus, KODK has had a “volatile” history in the meme-stock era and seems up for a nice rally every six months or so. Good enough for a punt.

Further investigation into the company may have revealed that the key source of both Kodak’s recent earnings and healthy book value was due to outsize investment gains in the company’s employee pension plan, which through fairly aggressive and successful investment over the past several years has notched a cool $1.1 billion in profits. These excess returns, combined with actuarial adjustments, leave the pension pool overfunded by $1.2 billion, or roughly 4x Kodak’s $278 million market capitalization as of Wednesday’s close.

Around 3pm Thursday, Bloomberg reported that the company was mulling a “pension reversion”, which as ChatGPT frantically explained to me, returns overfunded pensions back to the company, subject to hefty income and excise taxes. Even with steep penalties, the net proceeds to Kodak could be transformational. The stock surged 52% in half an hour, on the highest volume in 18 months.

I won’t pretend that the timing was anything other than fortuitous.

But with Kodak now at a $424 million market cap and $837 million enterprise value, is there more upside? The company hasn’t even officially confirmed its plan, let alone the net proceeds or tax implications but… maybe?

With 62 million shares outstanding, theoretical net proceeds of $500 million (>50% tax rate) would equate to a touch over of $8 per share in cash. The company could also save ~$50 million a year in interest expense alone by paying down its $435 million term loan which bears 5% cash plus 7.5% PIK interest. And there’s always the chance that yesterday’s price action puts the stock back on the meme trader’s radar.

I’m not pushing my luck, but I’ll stick around at least one minute longer, just in case. Sometimes life gives you lemonade.

[Update 9:33AM: Out of KODK. 9:37AM back in at 1/3 size]

Celsius Sizzles

Truth be told, I almost missed Kodak’s move entirely since my attention was focused on Celsius Holdings, Inc (CELH) which reported 4Q 2023 earnings before the bell on Thursday. Readers know that Celsius has been one of my favorite long names (particularly paired against Monster Beverage Corporation (MNST)) as it benefits from enhanced distribution and broad appeal outside the traditional energy drink market.

Based on price action alone, the report was a blowout. The stock came into earnings just shy of its all-time-highs and surged 20.4% on the day to close at a new record of $81.58 (or $244.74 on a pre-split basis). Since profiling the company back in October, (#75: Caffeine in a Can), the stock is now up 51%.

I’m happy for the move, but truthfully, I don’t think the stock reaction was deserved.

Topline and bottom line results did beat expectations ($347M revenue vs $331M expected, $0.17 EPS vs. $0.157 expected), but this was the thinnest “beat” in the past four quarters. I was hoping to see less negative seasonality in 4Q revenue and better margins. Since the company’s valuation already assumes significant growth, upside in the stock requires not just growth but a re-rating of expectations higher. And indeed, the stock traded off ~6% pre-market, which didn’t seem too unreasonable to me given the context.

But once the cash session opened at 9:30AM it was off to the races. Perhaps endorsements from the likes of Davey Day Trader Portnoy combined with short-covering added fuel to the fire. I won’t complain.

For the long-term, I remain optimistic. On the conference call, management provided an upbeat tone of the company’s 2024 retail planning re-sets, new product launches, and international expansion. My real-world observations — which have always been a key driver in my conviction — remain positive. I think the fundamental story for long-term growth remains intact. And so long as Monster maintains its $61 billion valuation despite declining domestic volumes, I think Celsius is attractive on a relative value basis.

But readers should be aware the company has gotten significantly more expensive without a significant increase in earnings expectations, and that the stock is accustomed to a high degree of volatility. A hiccup to the growth story could open an air pocket below.

Elsewhere…

Saylor’s Quotient

Love it or hate it, Michael Saylor’s MicroStrategy Incorporated (MSTR) remains one of the more fascinating stories in the market. Since transforming from sleepy software to satoshi stashing, MicroStrategy has accumulated an impressive 193,000 bitcoin, worth $11.9 billion at today’s price of $61,700. At present, the company has notched an impressive $5.8 billion gain on its bitcoin holdings.

But what’s maybe even more astonishing is how much more MicroStategy itself is worth, at a fully diluted enterprise value of $22.2 billion. After backing off the value of the software business (generously assumed at $1.5 billion here) and net debt, the residual value ascribed to the company is 74% greater than the market-to-market price of its bitcoin holdings. In other words, it would take a $107,653 investment in MSTR to indirectly own a single bitcoin, as opposed to simply buying bitcoin at the market for $61,700.

Of course, MicroStrategy’s “premium” isn’t news — It’s been a distinct feature of the stock over the past several years. And of course the premium can fluctuate widely in short periods of time. For example, in just the past week the premium has soared from ~40% to over 70% as MSTR stock has far outpaced the move in bitcoin — a move worth billions.

Pulling back the analysis back to 2020, we can see that MSTR has enjoyed a significant premium to its underlying holdings basically since the day it began acquiring bitcoin. By my calculations, MSTR’s market price implies a 36% average premium over the past three years, with periods exceeding 100%, and occasionally dipping negative. By these standards, today’s premium appears elevated but not unprecedented.

Usually when something trades at two different prices, there is an arbitrage opportunity — buy at the low price, sell at the high price and pocket the spread. In this case, sell MSTR and buy BTC. But this theoretical exercise doesn’t necessarily work in practice1. An investor can’t convert a share of MSTR into its pro-rata ownership of bitcoin or cover a MSTR short buy buying BTC.

And regardless of the spreadsheet math that suggests MSTR is overvalued relative to BTC, the spread has shown little signs of converging. Even a well-reasoned trade could turn widow-maker if the spread expands.

But while the arb isn’t available to the public, it is available to Saylor. MicroStrategy can issue new equity shares and use the proceeds to buy BTC. So long as this MSTR premium exists, issuing equity to buy bitcoin is actually accretive to existing shareholders (in terms of BTC ownership per share), and grows the total size of MSTR’s bitcoin holdings. For Saylor, whose only objective is to acquire the most possible bitcoin at the cheapest price, it is a no-brainer.

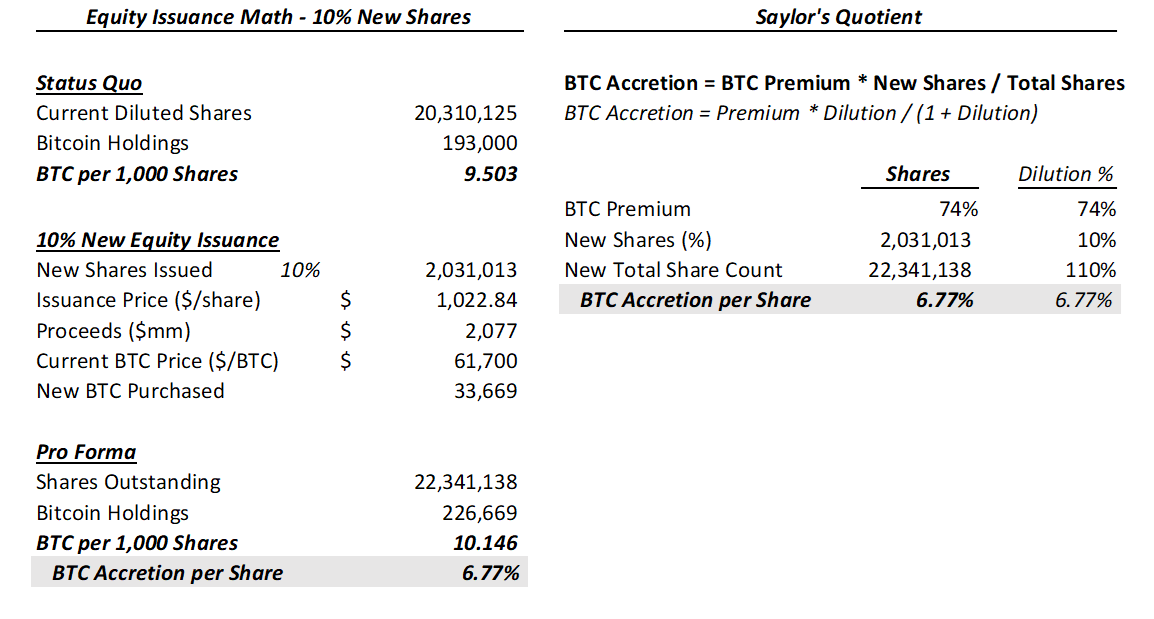

After playing around with the numbers, I’ve distilled this arbitrage opportunity into a simple formula. I call it Saylor’s Quotient:

BTC Accretion = BTC Premium * New Shares Issued / New Total Share Count

Or more simply…

BTC Accretion = Premium * Dilution / (1 + Dilution)

To demonstrate, below is an example of a new equity issuance for 10% incremental MSTR shares at current prices, which results in the bitcoin per share increasing by 6.77% (“bitcoin accretion”).

And indeed, this is Micro’s key Strategy. In 2023, the company raised $1.9 billion of new equity in at-the-market (ATM) offerings, which it used primarily to purchase new bitcoin. In its conference calls and investor presentations, the company subtly hints at this unusual arbitrage opportunity as a distinct strategic advantage.

So long as the premium exists, expect the company to continue issuing new shares into it. This week, MSTR exhausted its existing authorization for share sales under its prospectus, so it is temporarily sidelined from issuing new stock, but I would expect to see a new prospectus filed very soon. After all, there is a 74% premium to capture.

But why does this premium exist in the first place?

There is no obvious answer. The “proxy premium” argument2 was always weak in my book, and even weaker now that spot bitcoin ETFs exist. Similarly, the argument of “leverage” doesn’t make sense either. If you want levered bitcoin exposure, you can buy bitcoin with leverage. There is nothing inherently value-enhancing about MSTR’s structure.

One explanation might be that MSTR simply trades on its historical correlation to bitcoin, which essentially preserves the premium, and traders simply don’t care about the fundamental gap.

A more abstract and circular argument could be that the value is in the arbitrage itself. If the premium persists, Saylor’s Quotient allows existing shareholders to earn an ongoing “BTC yield” through the accretive equity issuance, while still generally mirroring the exposure to the underlying. In exchange, investors take the risk that the MSTR stock price might back to fair value - a massive plunge. Ironically, this perpetual motion motion machine is oddly familiar to the “yield-farming” schemes we learned about in 2021. Nothing goes wrong, just as long as everyone plays ball. Three years in and the premium persists.

I may be out over my skis on this one, but alas. These are the thoughts that rattle around my head at night and arrive in your inbox in the morning.

Dutifully,

The Last Bear Standing

Although one could still look at the “relative” premium and try to time when it is looks high or low by historical standards, or perhaps scan for meaningful short term deviations.

The idea that prior to broader access, investor’s were willing to pay a premium to gain exposure to the underlying via MSTR as a proxy.

Each week you push my comprehension and analytical skills in the market, thank you Bear.

Better lucky than smart! Nice work.