Frank Thoughts

#90: Does monetary plumbing matter? Is credit souring? Will labor crack?

Here are some frank thoughts.

On Monetary Plumbing…

It’s been interesting to watch the growing attention to the alphabet soup of monetary acronyms that long-time readers will be all too familiar with…. TGA, RRP, QRA, QE, QT, BTFP, ETC. Between the Treasury’s new borrowing announcement (the QRA) and the Federal Reserve’s Open Market Committee, this was a banner week for plumbing nerds to tout their stuff and everyone else to wonder quietly or aloud whether any of it actually matters?

Yes, plumbing matters. Kind of.

The gritty details of monetary plumbing are complicated but necessary to be truly fluent in modern monetary policy1. But if your main concern is whether the S&P 500 prints red or green, there’s an easier way.

A surgeon should have an intricate knowledge of the cardiovascular system. The rest of us simply understand that a severed jugular is bad for your health.

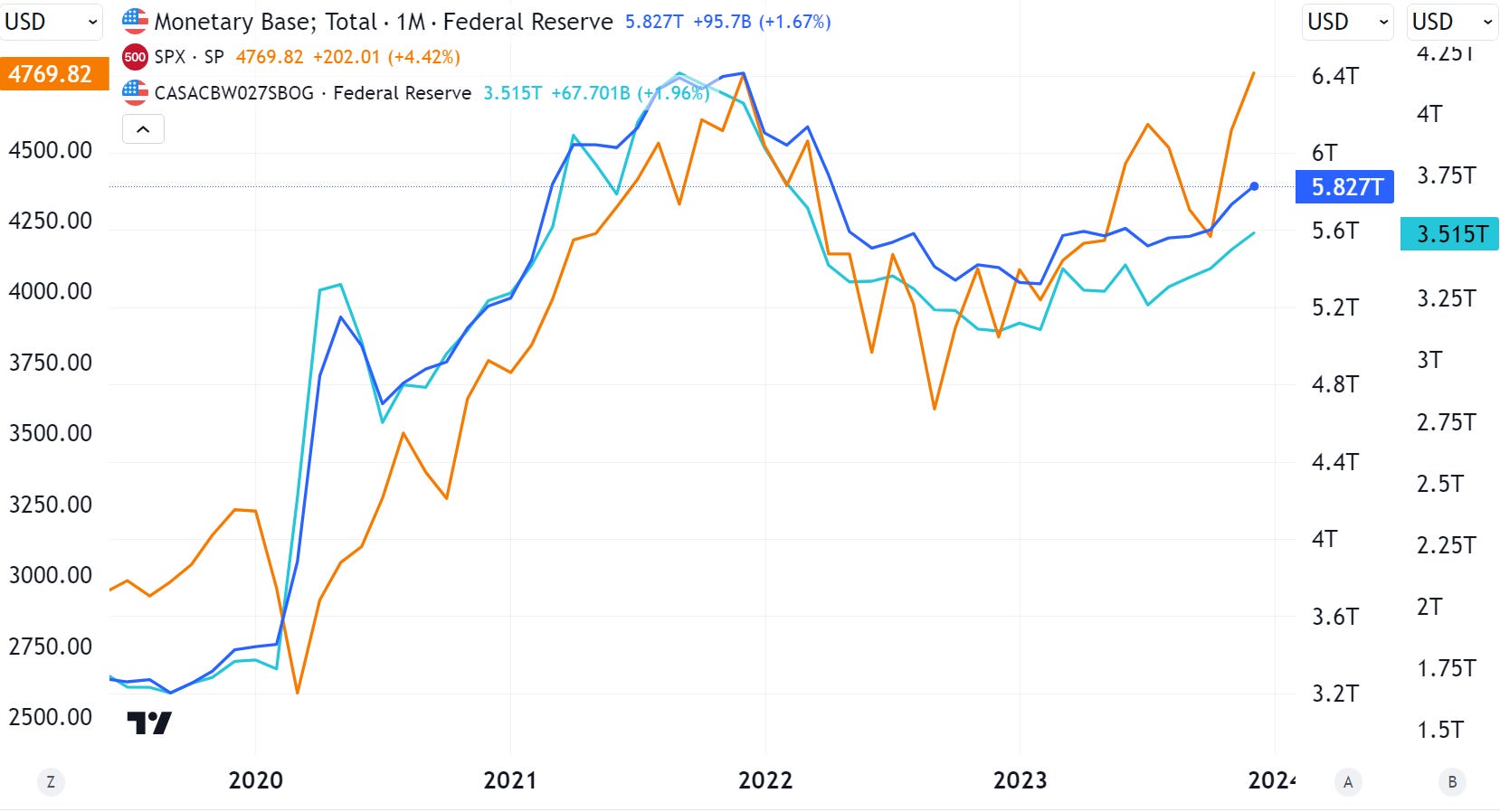

What I mean is that recognizing the directional flow of liquidity in or out of the financial system gets you most of the way there. In 2020, recognizing that firehose QE would benefit financial assets was important. In 2022, this liquidity dynamic reversed as trillions of dollars of cash fled the commercial banking system in favor of the RRP, up until the Silicon Valley Bank failure.

Most recently, in July 2023, I wrote that the decline in RRP usage “bodes well for both financial markets and bank stability… despite ongoing quantitative tightening”. And on November 3, 2023 after the TGA had been refilled, I noted that ongoing RRP drain would “lead to an outright improvement in banking sector liquidity and deposits, and even M2 money supply”. (Goldman Sachs noted the same thing, six weeks later). Sure enough, since November, M2 has trended higher, bank reserves have risen to the highest level in nearly two years, and the S&P has risen by over 12.6% to all-time highs.

I don’t believe in some strict or formulaic relationship between liquidity and asset prices2. But, other things equal, I do think that introducing more base money and bank deposits into the private sector is positive for risk assets priced in nominal terms. Ben Bernanke, the father of U.S. quantitative easing, agrees3.

Think of it this way — in a closed system, private market buys and sells net to zero. But if new money is being introduced to the private market (via the Fed, Treasury, or RRP), the sum of all private sector transactions turns positive. The private sector ends up with more money than it started with, providing more buying power for assets, and more dry powder (reserves) for banks to lend and make markets. The entire stated purpose of quantitative easing is to suppress interest yields by increasing bond prices, which according to basic finance theory should increase valuations of all other risk assets.

But practically speaking, should the average investor care if the Treasury has shifted a billion dollars of new issuance from the 10 year bond to the 7 year in the latest Quarterly Funding Refunding document? Probably not.

I would encourage two simplifying concepts.

First, have a sense for size. When thinking about aggregate monetary flows:

>$1 trillion is big and matters.

i.e. the Fed printed $3.0 trillion from March 2020 - June 2020, or RRP usage has decreased by $1.7 trillion over the past 8 months

$500 billion is medium and is worthy of some attention.

i.e. since SVBs failure, total bank reserves have increased by $601 billion

<$100 billion is small, and probably doesn’t mean a whole lot.

Second, understand the direction. Is private liquidity rising or falling? Importantly, this is not as simple as looking at the Fed’s total balance sheet. For much of the past two years, the two have moved in opposite directions.

One can predict the trajectory by carefully calculating the effects of QE/QT, with TGA and RRP flows. Or much more simply, just look at the weekly commercial bank cash assets data or the monthly monetary base data on FRED and see if it’s rising or falling. This latter approach gets you 80% of the value with ~2% of the work.

Here is my current assessment of monetary dynamics:

Ongoing bill issuance combined with economic incentive4 should continue to reduce RRP usage, offsetting the negative draw of QT and providing a supportive backdrop for risk assets (other things equal). This dynamic will turn negative if the Fed continues its balance sheet roll-off after the RRP has been entirely depleted (or if bill yields fall below the RRP award rate). Finally, any mention of a tapering or pause of QT will be a major positive for markets.

But this “negative-liquidity” inflection point probably won’t happen for at least several months, and possibly longer depending on April tax receipts. So for the time being, it may be wise to table these concerns and focus elsewhere — on earnings, industries, macroeconomics. I will continue to monitor these monetary dynamics and dutifully report back as circumstances shift.

Speaking of the market….

On Rates and Credit…

On Wednesday, Powell pushed back against a March rate cut, which the market placed at a ~60% probability heading into the meeting. I was a little surprised by the comment and think it was meant to mostly counterbalance the “party-on” dovish December FOMC, and the significant easing of financial conditions that has already occurred over the past several months.