The Return of the Calls

#40: On Leverage, Call Options, and The Gamma Squeeze.

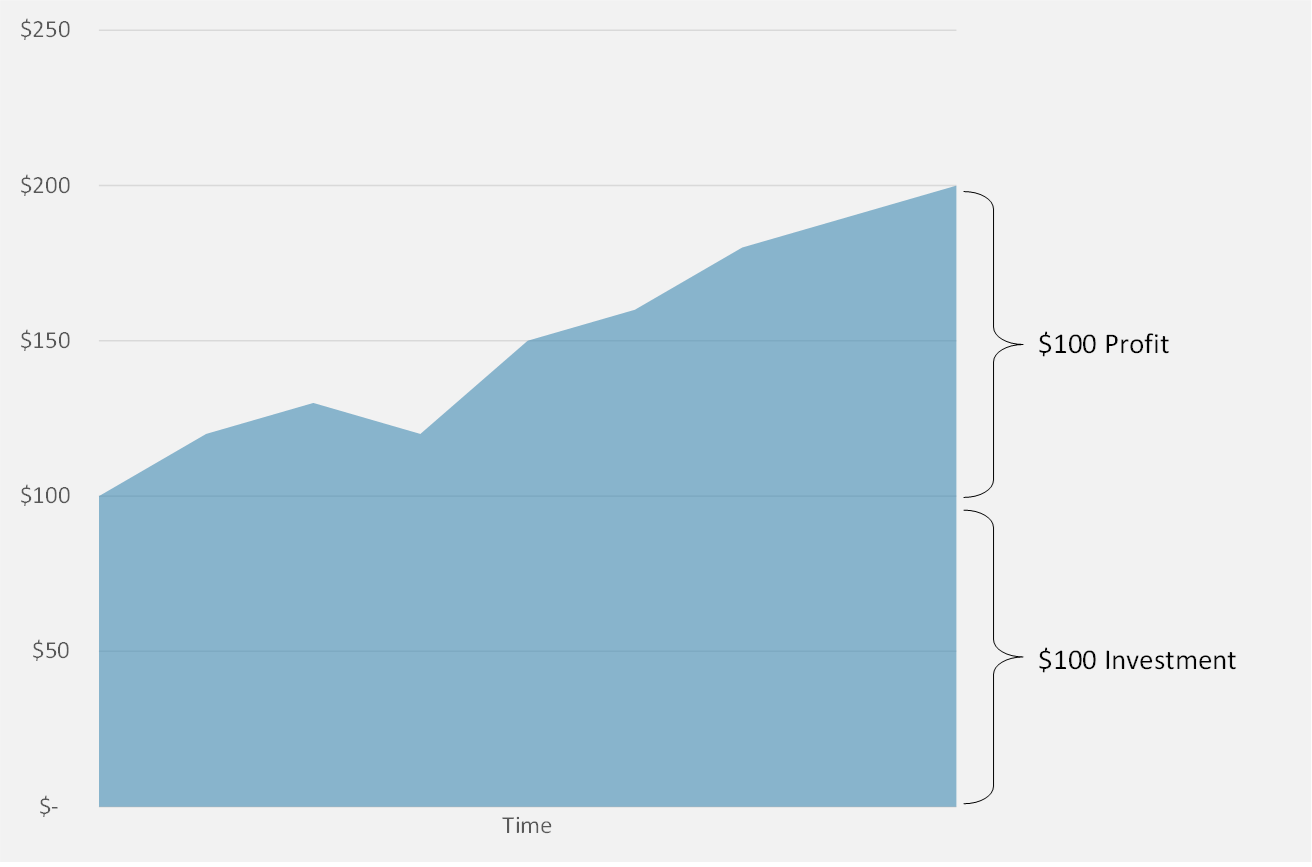

If you have $100, you might decide to buy $100 of stock.

If the stock doubles to $200, you will make $100 - a 100% return.

Or, you can use leverage.

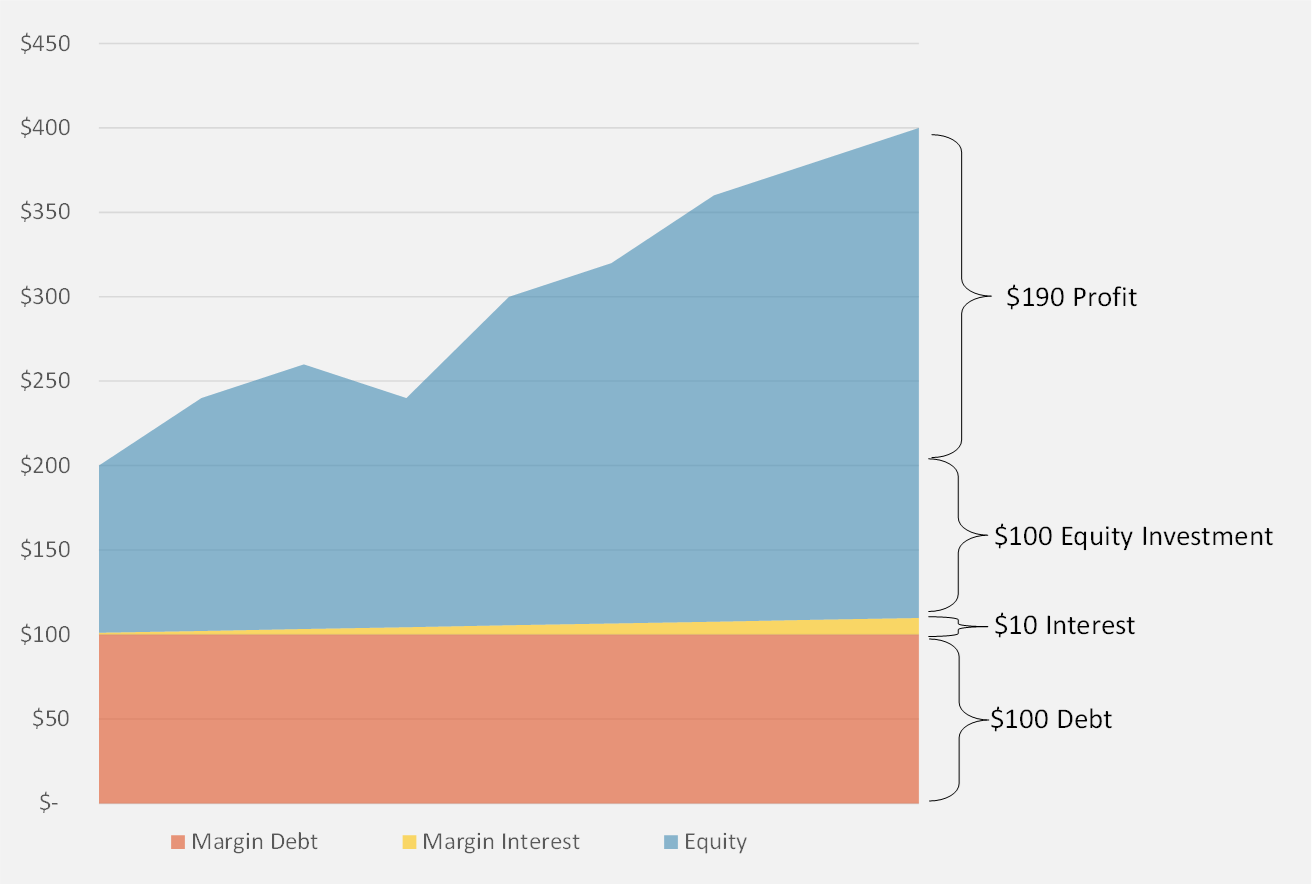

You can take your $100 and borrow another $100 and then buy $200 of stock. Then, if the stock doubles, the total value of stock you own increases to $400. After backing out the $100 you borrowed and $10 of interest, you are left with $290 in total proceeds.

In this instance, a $100 investment yields $290 in net proceeds - a $190 profit, or 2.9x multiple of invested capital - and nearly double the the return of the unlevered investment.

Borrowed money increases the purchasing power of stock buyers, driving prices up and magnifying returns. Higher asset prices in turn provide buyers even more debt capacity.

Margin debt - the traditional method for leveraged stock buying - often increases dramatically during bull runs and then rolls over with the market. On the way up, leverage is a positive reinforcing cycle. On the way down, the process works in reverse as leveraged investors have a less capacity to withstand losses before becoming forced sellers.

This market cycle has been no different. Margin debt peaked in October 2021 at $935 billion, and has since fallen 35% to just $606 billion by December 2022 - roughly back to pre-COVID levels.

But while traditional margin debt added fuel to the recent rally and decline, a new powerful form of leverage has taken center stage.

Option Leverage

There are many ways to think about options. A textbook might say that an option is an equity derivative that prices a number of variables including implied volatility, strike price, interest rates, and time to expiry.

More simply, options provide leverage.

A deep in-the-money (ITM) call option functions similarly to traditional margin debt. For example, if a stock trades at $200, a call option with a strike price of $100 may cost $110 to buy. This option price consists of $100 of intrinsic value1 and $10 of option value. We can think of the strike price as the "borrowed money", the intrinsic value as the “equity investment” and the option premium as "interest"2.

If the stock doubles to $400 by the expiry of the option, the call option will pay out $300.

In this instance, your $110 call option returned $300 in proceeds - a $190 profit or 2.7x multiple of invested capital - a similar payout as the levered investment above.

In other words, if you wanted to make a 2.0x levered investment in a given stock or the S&P 500, you could either borrow 1:1 on margin or you can buy call options with a strike price 50% below current values. Given the dramatic rise in options volumes and the inherent leverage that options provide, traditional counts of margin debt significantly underestimate the level of effective leverage in the market.

But there is a key difference between margin leverage and option leverage.

Margin debt - a form of asset-backed lending - is constrained by the current price of the stock at any given time. Margin lenders can only provide a fraction of the total funding, governed by a maximum loan-to-value (LTV) ratio. The remainder must be funded by equity of the borrower, with the LTV setting the limit on leverage available. This gives the lender a margin of safety to liquidate the asset without sustaining losses in the event that the asset price falls.

Options have no such constraint. Rather than working on a LTV basis, the inherent leverage of an option is dictated by its strike price.

An at-the-money (ATM) call option (where the strike price equals the current market price) has an intrinsic value $0 and is similar to buying a stock with 100% debt funding. At expiry, the call buyer receives all the gains above the current market price at expiry, or nothing if the stock goes down. The buyer’s net profit is determined by the payout at expiry minus the option premium they paid3.

The real juice comes with out-of-the-money options.

Out-of-the-money (OTM) calls have no intrinsic value but also cost much less than ATM calls because they have a lower probability of being exercised. By betting on an unlikely outcome, a call buyer can gain greater notional exposure to the underlying stock with fewer dollars at risk. Deep OTM call options provide nearly unlimited leverage for highly risky bets on stock price appreciation.

To use a concrete example, one could buy 100 shares of Tesla at Thursday’s closing price of $188.27/share for $18,827. If Tesla’s share price doubles in the next six weeks, the buyer of 100 shares earn $18,827 in profit, 2.0x their investment.

Alternatively, for the same investment one could buy 21,600 shares of notional exposure to Tesla via 216 contracts4 of $300-strike March-17-2023 calls, which last traded at $0.87 per share. If Tesla doubles by mid-March, the call buyer would earn $1,634,471 in profit5, or 87.0x their investment.

While this seems like a crazy bet, there are 69,722 Tesla $300-strike March-17-2023 call contracts outstanding today worth $5.9 million and current market prices, and covering 6.9 million underlying shares at just this one strike and expiry. If you were to sum all strikes and expiries, you would find the current open interest of call options represent a substantial portion of the entire float of the company.

Hedging Calls

So far, we have focused on call buyers making levered bets on upside appreciation. Now let’s consider the sellers.

The seller of a call option might be an unhedged speculator making an equal and opposite bet of the call buyer. But more likely, the seller is a market maker who is in the business of pricing options, hedging their underlying exposure, and capturing the option premium.

Hedging options is complicated in practice but fairly simple in theory.

If a market maker knew for certain that an option would be exercised, they would simply buy the same number of underlying shares that they sold via the option contract. The gain/loss of the underlying shares would offset the gain/loss of the sold call, and the market maker would lock in the option premium as profit.

But not all options are exercised. If a market maker simply bought its total notional exposure, it would be over-hedged (or net long) for all contracts that aren’t exercised. Therefore, the market maker hedges its exposure dynamically on a probability-weighted basis, which changes every second that markets are open.

Deep ITM calls have a high probability of being exercised and therefore must be hedged immediately. Meanwhile, far OTM calls have a low probability of being exercised, so a market maker will only buy a very small percentage of the notional exposure in the underlying stock to hedge this low-probability event.

But if the stock price starts rising…

The Gamma Squeeze

If a stock begins to rise, the probability that OTM call options will be exercised rises as well6. Market makers will therefore buy more underlying stock as a hedge. This hedging activity from market makers in turn puts more upwards pressure on the stock.

In the meantime, naked call-sellers7 will buy back their short positions (making hedged market makers shorter), at the same time that the rising price action attracts new buyers to the stock and options market.

This reinforcing feedback loop has come to be known as a Gamma Squeeze. While this term has become shorthand for price spikes associated with high call-buying activity, it’s important to understand the dynamics that are at play.

Recall, the strike price is the “borrowed money” of options leverage. Buying a far OTM call means you are buying an extraordinary amount of price-contingent leverage from the market maker. As the price rises, more and more of that leverage is unlocked. The result is like a margin debt feedback loop on steroids - one that can play out in the course of hours or days, rather than years.

But while the leverage is potent, it is fleeting. Unlike margin debt which can remain outstanding indefinitely, options leverage is temporary - it only lasts until the options expire or buyers close their positions.

The result is a historically odd price pattern that nevertheless has become very familiar over the past several years. Rising prices that accelerate in speed, often with an extraordinary blow-off top.

On a chart, they kind of look like a “j”.

Like these j’s…

…or these…

…or these.

Conclusions

The 2021 meme-stock frenzy may have been the call buyer’s coming-out party - the moment when yolo-ing calls burst off message boards and derivative desks and onto the public’s radar. But even as market enthusiasm has waned over the past year, the growth of the options market has not.

The recent run up in stocks since the beginning of the year has been punctuated by the return of call-buyer. Many of the underlying stocks in question are familiar suspects, even if most remain well off their bubble peaks. Tesla, the long-time gorilla of single stock options trading, set consecutive volumes records last week, as the price surged over 80% in 18 trading days.

On Thursday, the Chicago Board Options Exchange (CBOE) recorded 68 million contracts traded - an all-time record in volume. Now, the question is how long this buying can be sustained and what happens when that leverage vanishes.

Most bull runs are aided by new, exotic forms of leverage. The OTM call is merely the latest innovation, though one with undeniably entertaining outcomes. A rose by any other name would smell as sweet. Leverage is leverage - potent and fleeting.

If you enjoy The Last Bear Standing, please subscribe, hit “like”, and tell a friend! Let me know your thoughts in the comments - I respond to all of them.

As always, thank you for reading.

-TLBS

The difference between the $200 current market price and the $100 strike price.

The option premium compensates for both the probability that the stock falls below the strike price as well as the use of counterparty’s capital. The premium is paid up front with the purchase of the option, rather than interest which accrues over time in the case of margin debt.

Note, the option premium is greatest when the strike price is close to the market price. Therefore at-the-money options have a much higher option premium than deep in-the-money or out-of-the-money options. In our example, we assumed that the deep ITM option had an option value of $10, which means that an ATM option would cost substantially more than $10.

To continue with this example, assume an ATM call option on a $200 stock cost $30. If the stock doubles to $400, your net proceeds would be $200 less the $30 premium - equating to $170 dollars of net profit or a 6.6x multiple of invested capital.

A single call contract covers 100 common shares.

$376.52 (price at expiry) - $300.00 (strike price) - $0.87 (option premium) = $75.67 profit per share x 21,600 shares = $1,634,471 total profit.

The probability increases both because the current share price is close to the strike price, but also possibly because the implied volatility of the stock has increased as well, meaning the distribution of potential returns is wider.

As well as those short the stock outright.

Makes a lot of sense, especially with the popularity of 0 dte options.

Outstanding. That was the best description of a gamma squeeze I've read yet. I love your "J" illustration, so simple and concise. Not to be left out, yesterday I bought options for the first time in my life. Some June 30th puts on the SPX @ 3700, I am betting that the party is nearing the 4am closing bell. We shall see.

Cheers for another great article.