The Last of First Republic

#51: On First Republic's odds of survival.

Just as the dust appeared to be settling from Silicon Valley Bank’s (SVB) failure, First Republic Bank (FRC) is now circling the drain.

On Monday, in its first quarter earnings call, First Republic revealed the gruesome balance sheet damage caused by the mid-March bank run and the treacherous precipice on which it now stands. Management’s refusal to take investor questions said the rest.

The consequences extend beyond a single bank. A fourth bank failure in two months could shatter the growing confidence that the SVB fallout has been contained, and reignite deposit flight and funding stress for similarly positioned institutions.

First Republic will test regulators’ resolve. While the bailout of SVB’s depositors under the systemic exemption happened too fast for any real objection, there has been considerable blowback in the aftermath. The U.S. government does not want FRC to fail, but it also does not want to bail out the bank or its depositors. Further, a choreographed show of confidence in FRC has put $30 billion of external bank capital on the line, complicating the path forward.

The clock is ticking.

First, let’s dive into the First Republic’s pro forma net interest margin (NIM), profitability, and net asset value. Then, weigh the regulatory considerations and prognosis for survival.

Irreparable Harm

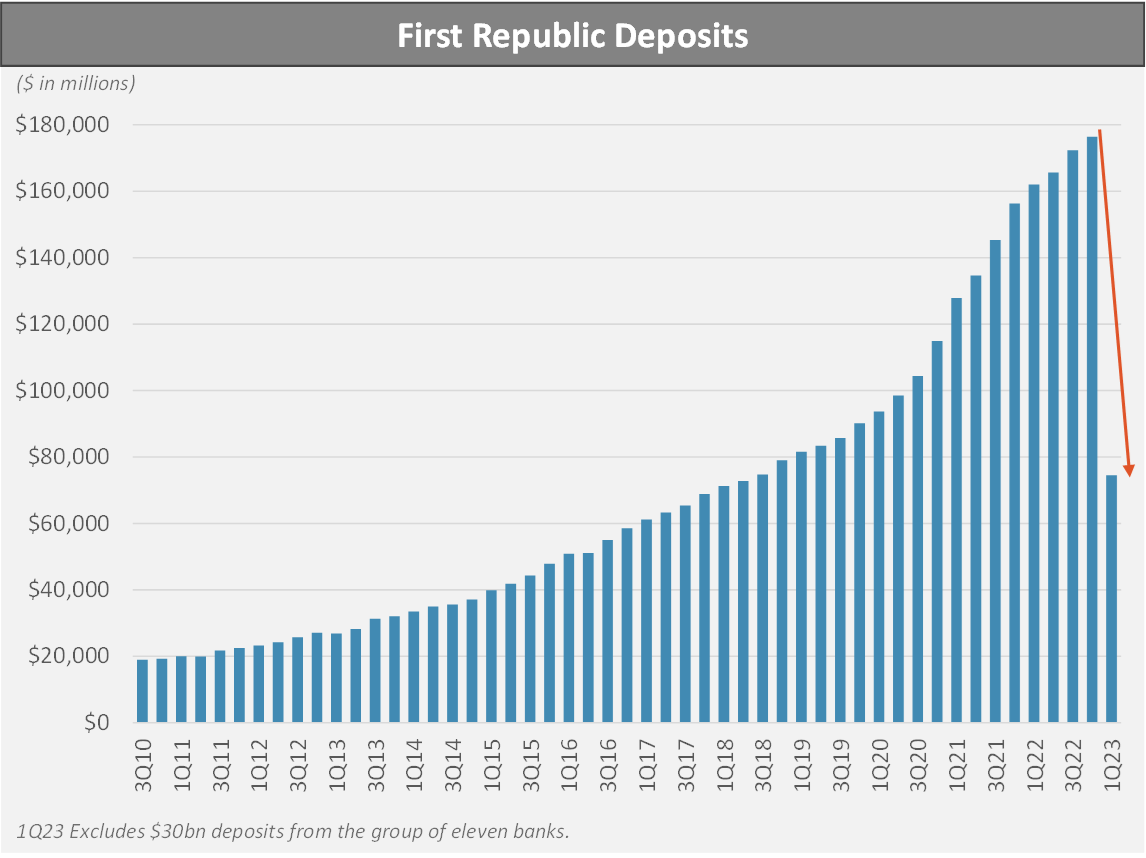

While Silicon Valley Bank’s deposits began falling in early 2022, First Republic saw healthy deposit growth through the year, reaching an all-time high of $176 billion by year-end. Instead, the downfall of FRC came from its proximity to SVB1. As Silicon Valley Bank’s failure awoke California’s cash-flush depositors to the evidently arcane notion of a $250,000 FDIC limit, the bank run spread to First Republic.

In a week, the bank lost an astonishing 58% of its deposits to the run. To meet this extraordinary demand for liquidity, FRC tapped the Federal Reserve and Federal Home Loan Banks (FHLB), borrowing up to $138 billion by March 15th. The next day, a group of the nation’s eleven largest banks agreed to provide a $30 billion capital infusion via uninsured Certificate of Deposits (CDs), allowing FRC to repay a portion of its borrowings.

The government’s bailout of SVB depositors, the creation of the Bank Term Funding Program (BTFP), and the show of confidence by the large banks stemmed the bank run, but for First Republic the damage was done.

In total, the bank replaced $102 billion of deposits at a weighted average cost of 1.24% with borrowings and CDs with a weighted average cost of 4.80% - a $3.6 billion profitability hit to a bank that has never made $3.6 billion in profit. Using the 1Q23 earnings report, we can estimate FRC’s pro forma net interest margin and earnings per share based on its current capital structure.