The Case for Higher Rates

#2: The Folly of the Fed and a Call for Change.

What is the role of the Federal Reserve?

At its core, the role of the Fed is to promote economic stability. Indeed the dual mandate of price stability and maximum employment suggests as much. The Fed has abdicated this duty, with great cost.

The primary way the Fed seeks to influence the economy is through interest rates, the cost of money. When money is cheaper, people have a higher propensity to borrow, expanding money supply, increasing economic growth and improving employment. When money is more expensive, the opposite occurs. Or so the thinking goes.

This is the knob that the Fed turns. In order to spur economic growth, it lowers interest rates, and to cool the economy down, it increases rates. Under this framework, the Fed uses its judgement to tilt the economy hotter or cooler with its rate policy.

However, there are two problems. First, the impacts of interest rate policy are far more complex than this simple framework suggests, particularly when near the lower bound of zero percent. Second, the Fed’s judgement about what the economy truly needs may be misguided.

For the past forty years since Fed President Paul Volcker broke inflation in the early 1980s, the Fed has made money ever cheaper in order to stimulate economic growth. After exhausting its traditional tools at the zero percent lower-bound, the Fed has moved on to new, exotic methods of lowering nominal rates, such as Quantitative Easing.

In doing so, the Fed has cast aside its core mandate as an economic referee ensuring stability, in favor of being a cheerleader and driver of economic growth. While this may not be immediately problematic, the Fed’s most essential role is to stabilize - which means counterbalancing the animal spirits of the private economy or signs of excessive money growth and inflation before they take hold. But the Fed has made it clear it no longer seeks to play referee. Its policy is all gas, no breaks.

The result is a bloated and debt-ridden economy, massive wealth inequality, unstable financial markets hopelessly addicted to the Fed’s largesse, and now, the true Achilles heel of low rates - inflation like we haven’t seen since the days of Volker.

To analyze the true impact of Fed policy, we will consider the topics below in detail:

Diminishing Returns of Low Rates

Debt, Wealth & Inequality

Financial Stability

Inflation

What we desperately need today is higher rates, not merely as a temporary measure or to restore a sense of near term credibility, but higher for longer, in order to promote long-term economic vibrancy. In the near term, this will cause economic pain and wealth destruction. But the pain is merely the hangover - a necessary step on the road to sobriety - and the wealth that may be destroyed was not the product of meritorious productivity, but manufactured by the Fed in the first place. In the long run, this will lead to a more prosperous, productive and equally distributed economy. I hope the Fed has the courage and wisdom to do so.

Diminishing Returns of Low Rates

In the introduction, I suggest that lowering the cost of debt boosts the economy because it makes it easier for people to borrow money to do economic activities. In other words, it encourages productive investment. This theory is at the heart of the lower interest rate policy, and is directionally true. However, as rates fall, the incremental benefit diminishes, and at some point reverses.

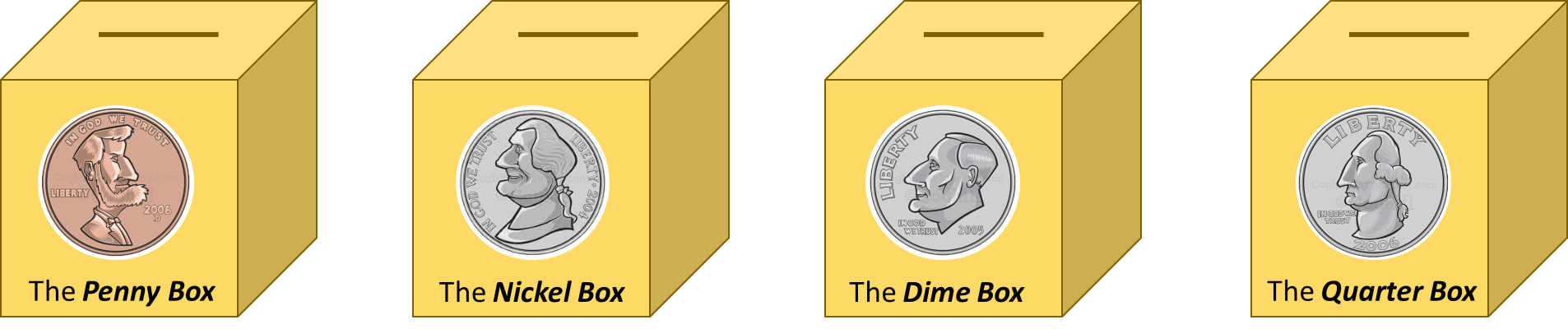

Let’s say you invent a Box that can literally mint money. This box can produce one real US coin per year, and it will cost you exactly $1.00 to build. The only problem is that you don’t have any money to build the box. Should you borrow a dollar to build it?

Well, you need some more information - which box is it, and at what rate can you borrow.

If this is a Nickel Box that produces one nickel a year, and the interest rate is 6%, then your interest cost of 6 cents exceeds the 5 cents the box produces, and you lose money. But, if interest rates were to suddenly drop from 6% to 4% it would change your opinion - it is now profitable to borrow and build the Nickel Box.

If you were building a Dime Box, you would borrow at either 4% or 6% to build it since the box produces more than either interest expense. Under neither circumstance would you build a Penny Box.

This elementary school example is meant to make an important financial point that you may gloss over if you read on its own: for debt to be accretive, the asset you are financing must have a higher return than the cost of debt. In this sense, the interest rate sets the bar for a minimum productivity of new assets that can be financed.

When the Fed lowers interest rates from 15% to 5%, it “unlocks” assets that return between 5% - 15% to be debt-financed. This likely leads to healthy, productive investment and economic growth. But as rates continue lower and lower, the Fed can only unlock less and less productive assets. This is the diminishing economic returns of lower rates. At some point, the only things left to unlock are the worst assets - Penny Boxes.

A CFO of a fast growing and profitable manufacturing company is going to build a new factory with a 10-year payback whether rates are at 0% or 5%, because the economics of his endeavor justify it. Penny Boxes have a payback period of 100 years.

When your growth is reliant on unlocking Penny Boxes, you have reached the end of the benefit of low rates for economic growth, and likely have already become counterproductive, as assets almost always produce less than you expect when you build them. This results in misallocation of capital, an increase in money supply and debt load, without a corresponding level of productivity to show for it, ultimately zombifying the economy.

But of course productive investment is not the only way debt is created…

Debt, Wealth & Inequality

Rather than funding new productive investment, debt can also be obtained against an asset that already exists, particularly if there is a reliable price marker and a reasonably liquid market.

Examples of assets that can be borrowed against are homes and stocks. Such collateralized borrowing could either be provided to a new buyer in order to finance the acquisition of an existing asset (i.e. a new mortgage to buy an existing house, or new margin debt to buy a stock), or by the existing owner of an asset to cheaply and tax efficiently monetize an asset they already hold (i.e. a home equity loan, or a $12.5 billion margin loan to buy Twitter).

This kind of borrowing does not create anything new, it merely provides cash to sellers of assets, financed by debt accumulated by the buyers, thereby benefitting those who already own assets. Even if an asset owner isn’t a seller, he or she will still see the value of the equities or house increase as cheap debt allows new buyers to bid up the broader market.

But this is only the beginning. New debt need not be created to benefit existing asset holders. When interest rates decline, the value of financial assets increase mathematically.

Fixed rate debt such as US Treasuries and corporate bonds are priced relative to the prevailing floating rate of debt in the market at any time. This means, if you buy a 10-year US Treasury when rates are at 5%, and then rates fall, the value of the bond you bought increases.

To see this in practice, consider the TLT ETF, a fund of long-term US Treasuries.

The price of TLT was $120 at the peak of the Fed’s hiking cycle in late 2018. By April 2020, in the earliest days of a pandemic that halted global economic activity, the price of those exact same securities had increased to $170 - a 42% increase in just over a year. This increase was driven almost entirely by the decision of the Fed to cut rates to zero and embark on unlimited QE1. Considering these assets are supposed to provide an annual return (yield) of ~3%, this was an extraordinary windfall for those who owned these securities.

US Treasuries are at the foundation of all financial asset pricing, as all other risky assets theoretically price at a spread or premium to Treasuries, which are considered the “risk-free” rate. Therefore, by lowering rates the Fed mechanically, mathematically increases financial asset values. Fantastic, if you own financial assets.

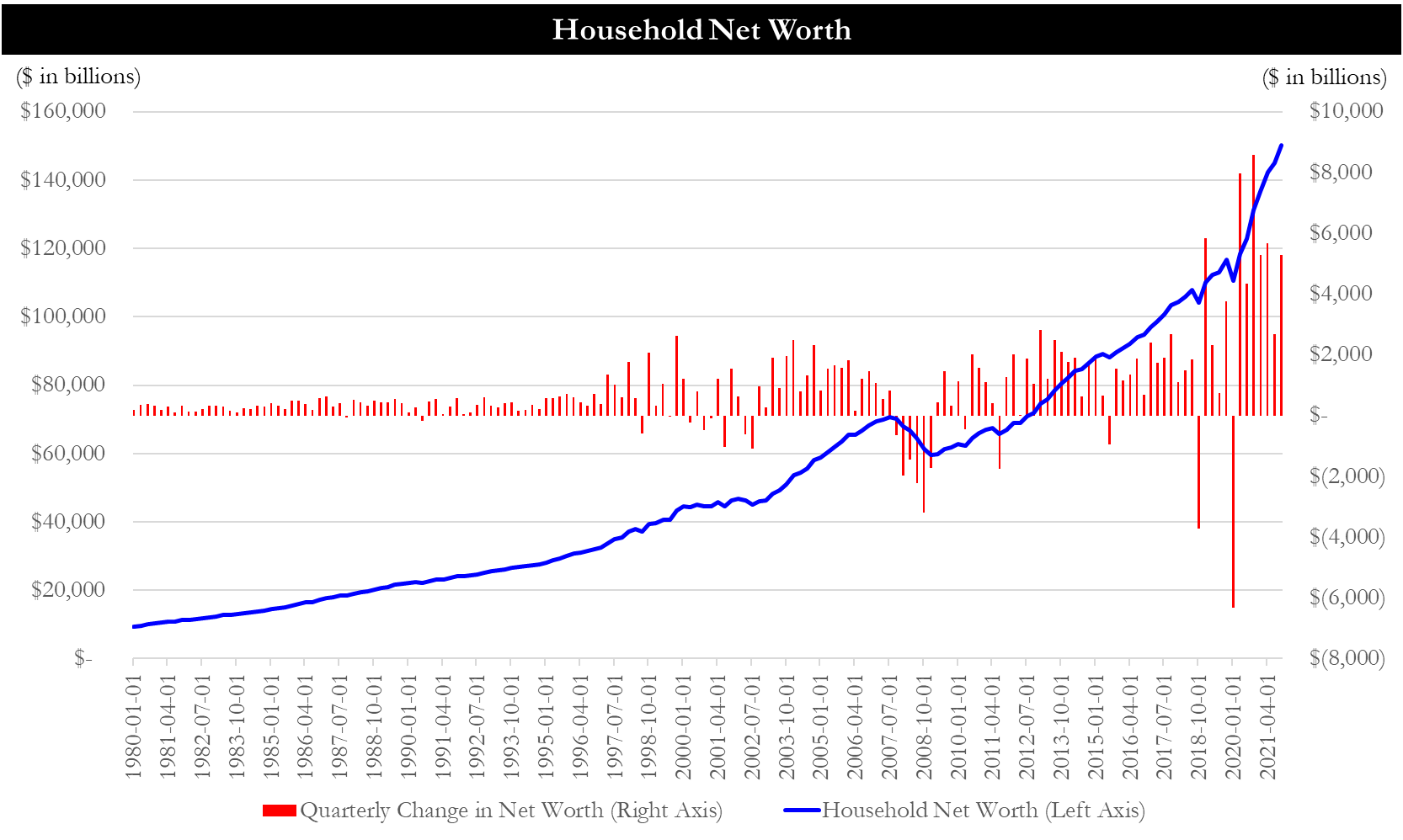

This isn’t populist rhetoric, it’s the Fed’s own data.

Per the Federal Reserve, total Household Net Worth before COVID-19 was $110 trillion. Two years later on 12/31/21, it clocked in at $150 trillion - a 36% increase - the largest increase ever over such a time period.

Isn’t it odd that during a period of economic turmoil, household wealth increased by the most on record? Indeed this strange dichotomy can be understood in large part by low rates and QE.

None of this activity, enacted at the pen-stroke of unelected officials at the Fed, is likely to increase true productivity or societal benefit. Rather, it’s the cheap alchemy of financial wealth.

While the pandemic put this force into overdrive, this trend of financialized wealth gains outpacing economic growth long preceded the COVID era, and is a result of a much longer trend of ever lower rates dating back to the 1990’s.

From 1950 - 1990, the ratio of Net Worth to GDP remained fairly steady between 3.0x and 4.0x. However, since the 90’s, this multiple has rapidly expanded, and is now double those levels at >6.0x. The alchemy of wealth.

While not generally publicized, the Fed is well aware of this wealth creation and likely sees it as a benefit of lower and lower rates. After all, if people are richer, they will spend more and stimulate the real economy.

The trouble is that not everyone is rich. Rather, it is the existing asset holders (i.e. people who are already rich) that benefit. For those who don’t own houses or stocks, this merely makes assets less obtainable, or forces them to take on ever more debt to buy them, with the cash proceeds going to the seller.

The share of this wealth held by the top 1% has consistently grown since the Fed's data began in 1989, reaching new highs of over 32% in the COVID era.

While the media breathlessly reported the hundreds of billions of dollars that accrued to billionaires like Bezos, Zuckerberg, Gates, or Musk, it’s important to understand that these people did not make billions of dollars. Rather, the share price of Amazon, Facebook, Microsoft and Tesla increased.

The wealthiest are the beneficiaries of the Fed’s generosity, while the average citizen is no better, and is arguably worse then they were. This is unsustainable and ultimately unjust. This wealth was written into existence by the Fed, and it is now the Fed’s responsibility to reverse this policy. Bezos will be okay.

Financial Stability

While the Fed’s ability to create wealth by fiat may seem like a cheat code, it is a double-edged sword. Up until this point, I’ve implied that the Fed controls interest rates. Of course, this is not really true.

While the Fed has near unilateral control over short-term interest rates, which form the basis of all interest rates, it does not by itself determine long-term rates, which price at a premium (a “term premium” or “duration premium”) which is determined by the public market2. Together, the short-term interest rates and the term premium combine to make the nominal long-term interest rate.

Below is the 10-year US Treasury disaggregated into these two components, the “Policy Rate” (approximated below by the yield on 3-month US Treasury bills) which is the short-term interest rate determined by the Fed, and the “Market Premium”.

Now, I’ve charted the same two series disaggregated below.

The driver for lower rates over the past 40 years has been the reduction in Policy Rate, while the Market Premium reliably fluctuates between a relatively tight band of 0.0% - 4.0%3. While this provides credence to the notion that lower rates are largely a policy decision of the Fed rather than driven by market forces, there is another important point to draw.

Since the Policy Rate has declined by over 10% in the past 40 years, and the Market Premium has not expanded or contracted outside of its cyclical range, the Fed has gradually ceded control over nominal rates to the market. In the extreme, when policy rates are at zero, the nominal rate entirely is determined by the market. It is precisely because the Fed emptied the chamber on its Policy Rate, that it was forced into its extreme tool of QE in order to regain its influence on long-term nominal rates.

The trouble is that the market is fickle and unpredictable. While this piece argues for the need for higher interest rates in general, the Fed ultimately needs to be a counterbalance to the market, which means lowering Policy Rate in moments of market stress to counterbalance rate increases and maintain relatively steady nominal rates.

Nowhere can this be seen more clearly than in 30-year mortgage rates, which have increased by 2.40% since September 2021 - the Fed’s Policy Rate only increased by 0.25% in this period, meaning market rates drove the fast majority of the move. By comparison, the most mortgage rates rose in the same time frame during the popping of the 2000’s housing bubble was just 0.87%.

Making matters worse, is duration. While changes in interest rates have a near-linear impact on the price of short-duration assets, longer duration assets have significant convexity.

The present value of $100, 30 years from now at an interest rate of 10% is ~$5. At a 5% rate, that present value increases to $23. At a 1% interest rate, the present value is $74.

As nominal rates go lower and lower, the movement in present value (i.e. bond prices) is much greater. The result is headlines like this.

By pushing interest rates to the minimum, the Fed pushes financial asset prices to their maximum. The resulting unwind means massive and potentially disorderly value destruction. Particularly when this occurs in fixed income or treasury markets, which are the bedrock of financial markets, the global financial market becomes deeply unstable - the opposite of the the Fed’s mandate.

Inflation

To date, the Fed seems unperturbed by the points above. Rather, their answer to “how low can we go” is to observe measures of consumer price inflation as the sole indication of overly loose policy. In other words, the Fed feels it can continue to juice financial assets and exacerbate wealth inequality so long as the average person doesn’t notice price increases - true trickle-down economics.

The fact that headline inflation remained subdued for the past decade despite the advent of QE has given the Fed and its cheerleaders enough evidence that their policies are not somehow inflationary.

While headline inflation remained in check for much of the past 40 years of declining rates, there are many non-monetary factors that impact consumer prices - and further, there is a lag between monetary policy decisions and their feedthrough to consumer prices.

Until recently, commodity prices - energy being the most important - remained well below overall consumer price trends. For much of the past decade, both oil and natural gas prices were a fraction of their price in the prior decade - a powerful deflationary force.

Even though this inflation test is inadequate by itself, it has been screaming trouble for over a year. Rather than abide by these tell-tale warning signs, the Fed instead abandoned its strict inflation target for an “average inflation” paradigm - tacitly acknowledging that inflation would exceed its 2% average target, and relying on the wishful thought that it would prove transitory. Now, real disposable personal income per capita has fallen in 10 out of the last 12 months.

Make no mistake - inflation is a regressive tax. The impact is far greater on those who spend nearly all their income on necessities, rather than the financial class, and pro-stimulus economists, who write off the phenomenon as tolerable. To the financial class and pro-stimulus economists, it is indeed tolerable because they occupy the high income segment of society. For those who have been left behind by the low-rate, money printing Fed, it is not.

Conclusions

The reason why I write so frequently about monetary policy is because it is so important. We have witnessed a failure of leadership by the most economically influential institution in the world - the Federal Reserve.

The folly of the Fed should have been acknowledged long before it got to such extremes. But that is not where we are.

The benefits of low rates has run dry. For a more productive, vibrant and equal society, we need higher rates, now.

The Fed was not merely content with lowering interest rates to zero but instead went full bore on its newest favorite toy - Quantitative Easing.

The Fed likely named this toy Quantitative Easing because a more honest description would reveal its obscenity. While QE is described as a way to keep yields restrained, yield is merely the inverse of price. Quantitative Easing is dollar printing with the explicit purpose of bidding up asset values.

There is considerable debate about how longer term rates are determined in practice - a chicken or the egg question. Does the Fed respond to the market in its rate policy or does the market respond to the Fed. In practice both are somewhat true and there is reflexivity between the two.

However, longer term rates (almost) always price at a premium to short-term rates. I also see no reason to believe that the Fed doesn’t unilaterally control short-term rates - that is why we wait breathlessly on FOMC day to hear what it decided. Taken together, the traditional understanding that the Fed determines short-term rates while the market controls a term premium is the best explanation of long-term nominal rates, until I see convincing data to the contrary.

While not shown on the graph, if you were to include recession shading on the charts, you would note that the market premium tends to go negative (yield curve inversion) prior to recessions, and then expands through the recession, ultimately reaching its high point at the early recovery stages.

A reader was kind enough to note it is “Volcker”. My apologies to Paul!

Incredibly interesting & insightful; 2 for 2! Thank you