Loads of Natural Gas

#18: With $9 Henry Hub, has the U.S. natural gas market finally turned?

Until recently, there hasn’t been a compelling reason to analyze the U.S. natural gas market. Charts and tables were just a complicated way to tell a simple story. Throughout the last decade, the U.S. has been awash with cheap, abundant natural gas. As a result, natural gas prices experienced a decade-long slump, trading around $2 - $4 per mmbtu1, nearly unchanged from the 1990’s in nominal terms.

Yet, for the past two years, natural gas prices have been on the rise. On August 22, 2022, natural gas futures at Louisiana’s Henry Hub closed at $9.68 / mmbtu, the highest price since August 1, 2008, 5,134 days ago. From the lows, gas prices have increased 554%.

Is $10 gas a temporary anomaly, poised to crash back to the levels of the past decade, or has there been a structural shift resulting in a tighter U.S. gas market?

The answer lies in a gradual yet monumental shift in U.S. natural gas infrastructure.

U-Turn

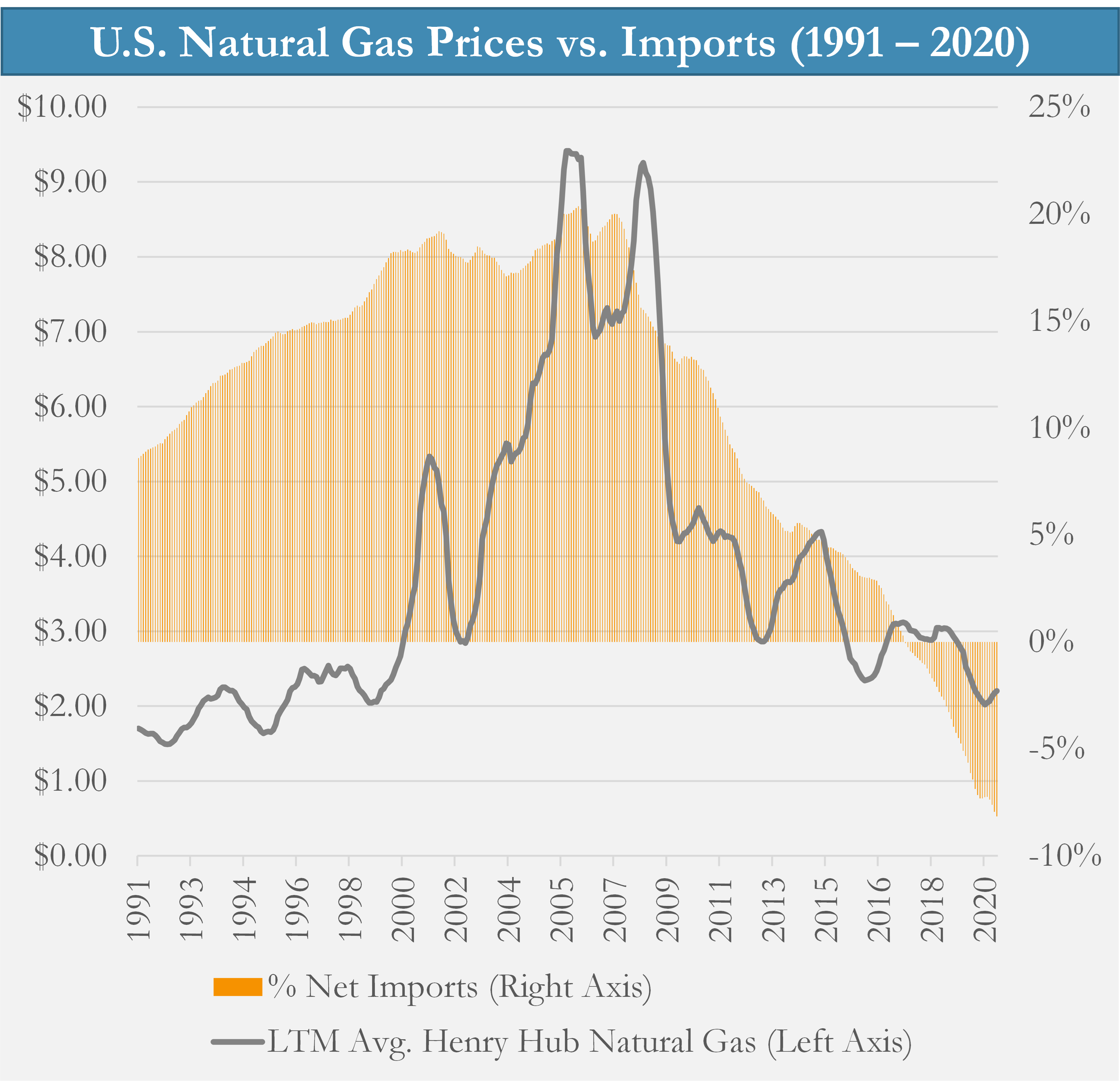

The U.S. has not always been long on gas. Not long ago, the country suffered from the opposite problem - demand was growing faster than supply. From the late 1980’s through the mid-2000’s, domestic consumption increasingly outpaced domestic supply. The U.S. was structurally short gas and getting shorter.

To fill the gap, U.S. net imports of gas reached 10 billion cubic feet per day (bcf/d), or 20% of domestic consumption. Unsurprisingly, gas prices rose from $2 in 1991 to over $9 in 2006 incentivizing new development, imports and pipeline infrastructure.

With dwindling local supply and rising prices, the U.S. was focused on finding diversified foreign supply. While pipelines from Canada supplied a majority of imports, the U.S. was also preparing to take advantage of the newly emerging seaborne market for natural gas - LNG (liquified natural gas)2.

In 2007, the U.S. EIA published a report titled U.S. LNG Imports - The Next Wave, which predicted a strong increase in U.S. LNG imports in the coming years.

At the time, U.S. already had nearly 5 bcf/d of onshore LNG import capacity scattered on the East Coast and Gulf Coast and three massive new regassification terminals were nearing completion. Freeport, Sabine Pass and Cameron were all slated to come online by 2008, doubling total import capacity to over 11 bcf/d.

Then came shale. The technology of shale - the combination of horizontal drilling and new fracturing technique - was decades in the making3, but its first successful commercial application came in the Barnett Shale in 2005. By 2008, horizontal shale wells dominated new gas development in the region.

This new technology unlocked enormous volumes of previously unrecoverable natural gas reserves across the country. For the first time in years, U.S. natural gas production was growing. Rather than increasing reliance on foreign imports, the U.S. would solve its gas shortfall through domestic drilling.

Overnight, the U.S. natural gas balance flipped on its head. The nation was poised to become a natural gas exporter.

Ironically, the EIA’s report calling for a new wave of LNG imports bottom-ticked the U.S. supply deficit and top-ticked U.S. natural gas prices. None of these new LNG facilities would import a single molecule of gas, and the existing terminals shut down to reverse their flows.

The Bakken Dilemma

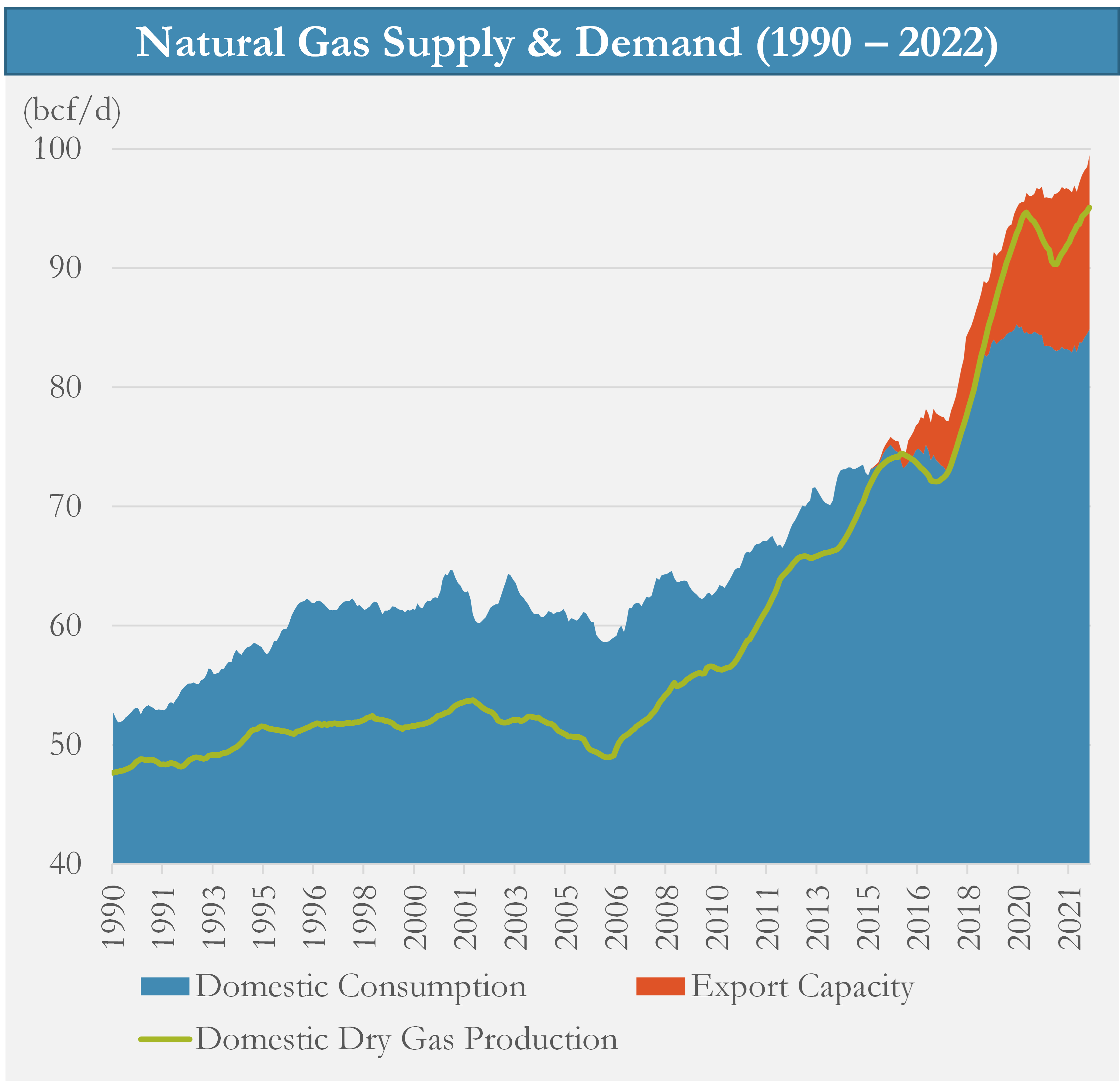

The shale revolution proved far more prolific than even its loftiest early projections. Shale production today has grown at a compounded rate of 18% per year since 2007, increasing 11-fold to nearly 80 bcf/d today.

Yet, this new resource was a double-edged sword. In Windmills and Oil Wells, I used the phrase “The Bakken Dilemma” to describe a common predicament in natural resource development. To wit:

This is the challenge of resource extraction. New resource attracts development, increasing regional supply and reducing prices, particularly if takeaway capacity lags the production ramp. The gold rush crashes the market for gold. […] In the case of energy extraction, the bottleneck is often in takeaway capacity.

Quickly, the entire U.S. gas market was experiencing The Bakken Dilemma - a tragedy of riches. The rapid increase in production reduced both the need for imports and market prices along with it, kicking off a decade-long bear market in natural gas4.

For the last decade, the limiting factor for U.S. natural gas production was economics, not geology. There is no shortage of gas in the ground, but at sub $3 hub prices, only the best wells in the best regions are profitable5. For most gas drillers, it has been a depressing decade of rock bottom prices, bankruptcies and consolidation.

Natural gas exports have long been considered the light at the end of the tunnel for the gas market, but the infrastructure has been a slow process. The development of export infrastructure has been so gradual that we almost forgot it was happening.

But slowly, surely, it arrived.

By Land and By Sea

While drilling rigs dotted the Pennsylvania country side, a separate massive investment in infrastructure was underway to bring gas to the foreign market, both by land and by sea.

By land, a series of new pipeline expansions were built along the Southern border, bringing flow to Mexico. Since 2015, pipeline exports to Mexico have increased by nearly 4 bcf/d due largely to the Tuxpan Pipeline along the Texas/Mexico gulf coast, and the Trans-Pecos Pipeline running from the Permian Basin’s Waha Hub down to population centers in central Mexico.

By sea, the very same LNG facilities that were planned to import gas in the mid-2000’s were being reversed to serve as LNG export facilities. On February 24, 2016, the first shipment of U.S.-produced LNG left the Sabine Pass facility in Louisiana aboard the Asia Vision in route to Brazil.

Since Sabine Pass’ first production unit6 (known as a train) came online in early 2016, 18 more trains have followed. Today, the U.S. has 11 bcf/d of LNG export capacity.

Between pipelines and LNG, the aggregate export capacity of the U.S. has increased by nearly 15 bcf/d since 20157. For reference, this is enough to supply half of the entire U.S. power generation sector, or nearly double the entire gas demand of Germany.

It is tempting to think of export capacity as a release valve - a way to whisk away excess gas after local demand has been met, but this is wrong. Exports are a very firm source of demand, both economically and contractually. In the industry parlance, these infrastructure projects are demand-pull rather than supply-push.

Mexico now sources a large majority of its gas from U.S. pipes and is reliant on those flows. Firm volume commitments ensure this gas will cross the boarder.

Meanwhile, Europe and Asia are in desperate need of LNG. Due to long-term fixed volume contracts, as well as the arbitrage between U.S. and global natural gas prices, LNG export facilities have been running near full capacity (except for the early days of the COVID pandemic). This year, the U.S. became the largest LNG exporter in the world.

The Balance

When including new export capacity as a component of overall demand, we see a clearer picture of the dynamics at play in the gas market. Both domestic consumption and production remain at the pre-pandemic levels of late 2019. Yet in total, gas demand has reached an all time high, driven by 5 bcf/d of new export capacity since the start of COVID.

For the last decade, as new gas production ran ahead of demand, market prices served as a signal to gas drillers to cut further production. Today, prices are incentivizing production as demand growth outpaces supply growth. For the first time in a decade, the gas market has gotten tight.

As the completion of incremental export capacity pushes demand higher in the coming years, the U.S. must produce more gas8, increase its imports from Canada, or decrease domestic consumption to balance.

The opening of the U.S. market to foreign buyers means that local buyers face increasing price competition from the rest of the world which is in desperate need of gas. With export facilities providing firm demand, the marginal buyers of natural gas are now domestic consumers; power plants, industrial users, and residential customers.

Winners & Losers

As with any transition, a tighter U.S. gas market involves tradeoffs. Whether it is good or bad depends on who you ask.

Winners:

U.S. Gas Producers: The gas business was long overdue for some good times. Higher gas prices mean strong cash flow from existing production and the ability to grow further. Gas drillers have already seen a massive rebound in stock prices - EQT the largest producer in the Marcellus has seen an 8x price appreciation since the COVID lows9.

The U.S. Government: Swinging from energy imports to exports has turned a liability into an enormous geopolitical and economic asset. Today, as the world’s largest exporter of LNG, the U.S. is filling the energy needs of Asia and Europe.

Foreign Energy Consumers: Cheap U.S. gas supply should result in lower global prices over the long term. In the short term, it will be necessary to keep the lights on in many countries this winter.

Coal: Cheap gas has arguably been a bigger coal killer over the past decade than “ESG” or regulation. As the most directly substitutable fuel in power generation, higher natural gas prices make coal more competitive.

Losers:

U.S. Energy Consumers: The main beneficiary of cheap gas has been U.S. consumers who have enjoyed globally advantaged energy prices (and feedstock for industrial production). The relative advantage of U.S. energy prices will shrink as export capacity grows10.

Foreign Energy Producers: Nations now can begin reducing their dependence on Russia, and other less friendly commodity-producing countries. Even friendly energy producers must compete economically with U.S. LNG supply.

The Conclusions

After years of anticipation, the natural gas export infrastructure has finally caught up with the explosive growth of shale gas. The U.S. has taken center stage in global energy production, as the largest global producer of oil and now the largest supplier of LNG.

The U.S. has an enormous supply of gas reserves, ensuring it will be able to maintain its own energy dependence while supplying the rest of the world with natural gas for years to come. However, the increasing demand of export infrastructure, combined with flat domestic production during the COVID pandemic has resulted in the tightest gas market in fourteen years.

With export demand set to grow, producers must ramp up volumes, imports must increase, or domestic consumers must reduce consumption. As always, price will balance the market.

Energy units are unfortunately confusing. Mmbtu is an energy measure meaning “million British thermal unit”. Think of one Mmbtu as one “unit” of gas. Throughout this post, I will refer to gas quantities in Billions of Cubic Feet per day or “Bcf/d” which equals a daily flow of ~1 million units of gas.

Oil, a liquid at normal temperature, can easily be loaded on tankers and shipped globally. Methane (natural gas) is much less dense in its gaseous state and therefore uneconomic to transport in vessels, limiting its transportation to pipelines rather than seaborne vessels. However, by supercooling natural gas to its dense, liquid form, large quantities of gas can be loaded onto ships and transported economically. LNG export terminals are “liquefaction” terminals - where gas is super cooled and loaded on vessels. LNG import terminals are “regassification” terminals. Critically, these are one-way streets.

Including research assistance from the Department of Energy to improve natural gas production.

The development of shale oil made matters worse for gas producers. Oil drilling in the Permian produces a significant amount of associated natural gas that floods the market and is largely agnostic to gas prices.

Regional differentials and transport costs mean that actual realized prices of producers is far below benchmark Henry Hub prices.

With an operating capacity of 0.6 bcf/d.

Beyond the current capacity, there is an additional 5.6 bcf/d of capacity currently under construction expected to be ready over the coming two years. Including projects under construction, total new export capacity will increase to over 20 bcf/d. Behind that, there is yet another 7 bcf/d of FERC-approved projects that are in various stages of development pre-FID. FID or “Final Investment Decision” is the final go/no-go decision that puts a project fully in motion.

Which, to be clear, the U.S. has ample capacity to do. Even if gas prices were to fall 50% from current levels to ~$5, there would still be a strong price signal to produce across several basins.

Though, still has not eclipsed its all-time high set in 2014 at the peak of Shale Mania, when producers were rewarded largely for growing production rather than cashflow, and before associated gas from the Permian began to supplant Northeastern gas supply.

Though, even with higher absolute prices, energy in the U.S. is still cost-advantaged by global standards.

>Coal: Cheap gas has arguably been a bigger coal killer over the past decade than “ESG” or regulation. As the most directly substitutable fuel in power generation, higher natural gas prices make coal more competitive.

This is the most underrated part of the article. Coal wasn't killed by ESG, it was killed by nat gas. I'm heavily positioned into Australian coal producers for the coming year.

One of the best quality Substack out there!