Has the Rally Peaked?

#32: Bracing for a reversal in rates, stocks, and volatility

I can’t help but feel like we’ve seen this pattern before. A downward pessimistic grind eventually gives way to a rebound of optimism. Asset classes ebb and flow in tandem, risk-off then risk-on. Undulations of bi-polar sentiment.

The market is nervously shifting its weight from the right foot to the left foot, as it considers inflation (and a tightening Fed), a potential recession (that hasn’t yet arrived), and surprisingly durable growth (in the meantime).

We have seen three distinct bear market rallies so far this year. The first rally peaked in late March, and the second peaked mid-August. I believe the third is now cresting.

Let’s consider the following components.

Interest Rates

Equities

Volatility

Interest Rates: The Duration Rally

Over the past six weeks, we have seen a massive rally in long-term treasuries1. Yields on the 10-year US Treasury have fallen from over 4.30% on October 21, to under 3.50% today, an 80bps rally. The 30-year Treasury has followed in lockstep.

This recent rally has pushed the 10-year yield far below short-term rates. The spread between the 10-year and 2-year Treasury stands at -83bps, the lowest point since 1981, while the spread between the 10-year and 3-month Treasury stands at -78bps, the lowest since 1999. In other words, the Treasury curve is now deeply inverted.

Let’s consider two possible explanations for these moves.

First, assume that the market is entirely rational and accurately re-calculates the fair-value of assets daily. Under this assumption, new information since October must have lowered long-term rate expectations by nearly a full percentage point, even while short-term expectations barely budged. Maybe you can conjure up an explanation that fits this mold, but it feels like a “goal-seek” to me.

At best, the recent data on inflation and the economy has been mixed. CPI and PCE readings have come in below expectation, but employment and wage growth remain strong. It's hard to think of any recent news that would suddenly justify a kink several years out on the yield curve.

Alternatively, it’s possible that the long-term rate market is not purely rational, and instead fluctuates based on positioning, sentiment, derivatives, structured products, and cross-asset volatility.

Yields on the 10-year UST rose dramatically since the summer, from 2.51% in early August to over 4.30% by mid-October. What if those who bet on higher rates (directly or via derivatives) have realized their gains, while a light softening in Fed-speak tilted sentiment, and dip-buyers rushed in to catch the falling knife? The result would be a short-term rally in rates, like what has happened over the past several weeks.

This feels more plausible. We’ve already seen this play out twice this year, in February/March and again in June/July. In both cases, the rally in duration fizzled as sentiment swung, and the market relented to a higher-for-longer Fed.

To be direct - at a 3.5% yield today, the 10-year assumes that inflation will be eradicated in relatively short order, and monetary policy will revert to a near-ZIRP regime for the rest of the decade2. In my view, this is too optimistic on inflation and too pessimistic on longer-term economic growth.

Rather, I expect the 10-year yield to rise in the near-term, at least until we see unequivocally bad economic data (rapid job losses or a meaningful contraction in consumption).

Equities: Between a Rock and a Hard Place

Since the September CPI report released on October 13th, stocks have marched higher, while rotating away from technology and into cyclicals and staples3. From trough to peak, the S&P 500 gained 17%, the Nasdaq 100 rose 16%, while the Dow Jones Industrial Average was up nearly 21% - only 6% off its all-time highs.

Déjà Vu? We saw a similar action this year in March and again in July/August4, which in hindsight we can definitely label “bear market rallies”. Will this time be any different?

My guess is no.

Third quarter earnings were not a disaster but declined sequentially. Recent gain in equities has been driven by higher multiples rather than higher earnings.

Plus, the outlook for both earnings and multiples isn’t very bright. Margins are already contracting, while topline growth is expected to slow in the coming year, putting pressure on earnings. Meanwhile, multiples could decline either due to lower growth expectations or higher discount rates.

Stocks are caught between a rock and hard place. Strong nominal growth (either via inflation or real gains) will force the Fed to hold rates higher and tighten financial conditions further. This is probably the preferable outcome for stocks. A worst scenario is an outright recession, with falling earnings, sentiment, and growth.

Ironically, the goldilocks scenario implied by stocks is the opposite of the “efficient-market” explanation for the fall in long-term interest rates. A more cohesive explanation for the simultaneous rally in stocks and bonds is a swing in risk-on sentiment5 and a reduction in volatility across assets.

I expect the recent gains in stocks to be yet another bear market rally and that indices will fall further from here.

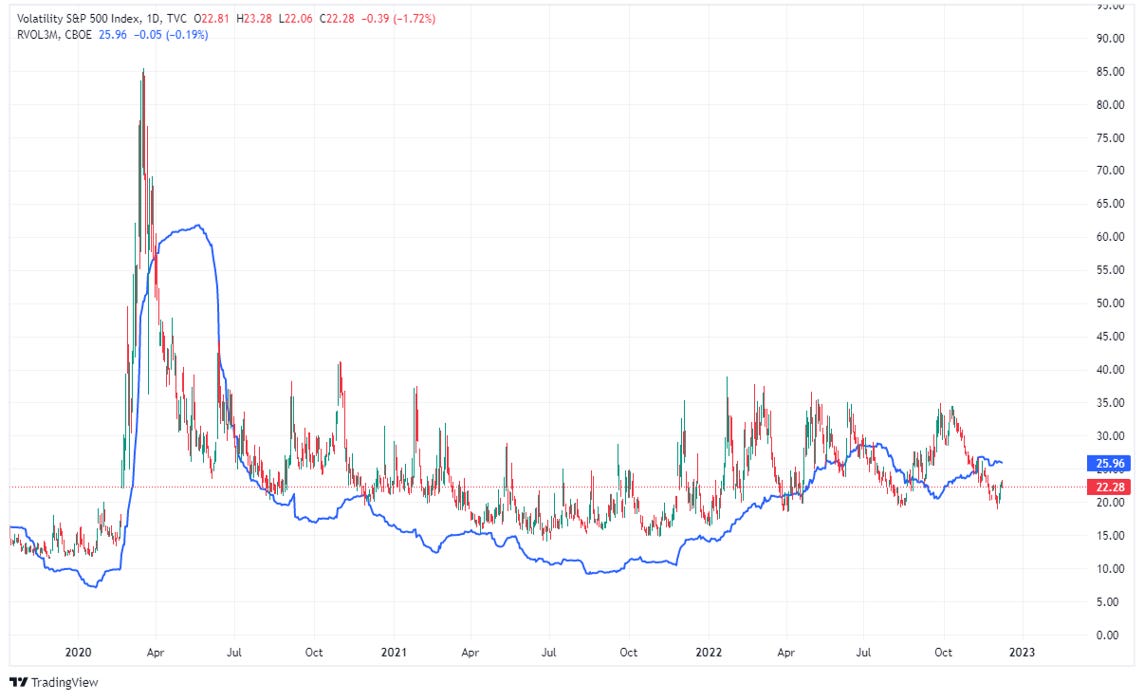

Volatility: Tails Aren’t Wagging

The rally since mid-October has coincided with a dramatic drop in stock and bond volatility (“vol”), a near certainty given the inverse relationship between price and vol. Therefore, if we expect stocks and bonds to fall moving forward, we should also expect a volatility to rise.

But volatility has been a bit of an enigma over the past year.

On one hand, both realized and implied equity volatility has risen substantially since 2021 (while bond volatility has also exploded higher).

Yet, despite a rise in the absolute level of volatility, long-vol products and strategies have mostly “underperformed” expectations. This is due to the unique, spiky nature of volatility, and how many utilize the product as a result.

It is no secret that volatility spikes dramatically in moments of true market panic. Therefore, a common hedge for tail risk (market crashes) is to buy vol tails - i.e. buy far out-of-the-money calls on the VIX index or long-vol ETPs (VXX, UVXY, UVIX), the prices of which increase parabolically in crashes.

But tail bets have not paid because the market hasn’t crashed. In fact, the intra-day high on the VIX for the past year occurred all the way back on January 24th, when the S&P 500 traded around 4,300. Even as each subsequent sell-off led to lower-lows in equities, each peak in the VIX has also been lower than the last. The VIX stopped spiking.

This has led to a striking divergence between a rising VIX and falling volatility-of-volatility (“vol-of-vol” or “VVIX”). Year-to-date, the VIX has risen 31% while the VVIX has fallen 22%. In absolute terms, VVIX reached a three-year low at the end of November, far below any point during the pandemic.

There are a number of reasons why the market hasn’t crashed; dip-buyers have stepped in forcefully, corporate earnings have held up, and the economy has remained strong.

But a contributing factor may have been that the cost of tails was too high. Today, crash protection has become significantly cheaper, despite the rise in the VIX. Tails are sold cheap as fewer people buy tails6.

Arguably, this sets the stage for the next Volatility Squeeze. But at the same time, volatility is reflexive. If there isn’t a sudden rush for protection (forcing shorts to cover), a squeeze won’t occur, and there is no telling when such demand will materialize.

To summarize directly, if stocks and bonds fall in the near term, then the VIX will rise, but it doesn’t mean the tail will start wagging. If, however, you’d like to take a gamble on the tail, the buy-in has rarely been cheaper.

Conclusions

My personal expectation is for a reversal in duration, stocks, and volatility as the third bear market rally crests.

The recent rally in long-duration treasuries seems more likely a result of positioning, sentiment, and dip-buying, rather than a rational decline in long-term rate expectations.

Equities similarly have seen gains of 15% - 20% in the past two months, though appear to be stalling out at lower-highs. Whether by the Fed or by recession, prices will fall from here.

Volatility remains the most challenging to predict. I believe the short-term path in volatility is higher, but the big question is in the tails. Will we eventually see a major spike in the VIX? I can’t say for sure - but it’s possible that complacency has finally bred opportunity.

Of course this is just one person's analysis. These predictions could take days, weeks, or months to play out - or may prove wrong entirely. There are also a number of important economic releases and a Fed meeting in the coming weeks which could shift sentiment unexpectedly. Only time will tell.

So, what should you do with this analysis? Chew on it, swish it around, see if you like the taste. Take it together with any and all information you can get your hands on, and come to your own conclusions. What do you believe?

As always, thank you for reading. If you enjoy The Last Bear Standing, like this post and tell a friend! And please, let me know your thoughts in the comments - I respond to all of them.

-TLBS

Recall, that the price of a bond moves opposite its yield. Falling yields means increasing price.

While interest rate spreads typically invert before a recession, they expand dramatically throughout the recession. By the beginning of the recovery, the 10yr - 3yr spread usually peaks around 3.5% - 4.0%. In other words, if the Fed cuts rates to zero, we would still expect the 10-year to trade around 3.5% in the early recovery period - exactly where it prices today. The exception would be if the Fed embarks on another unlimited QE bonanza, driving long-term rates down as it did during the pandemic. But I would be surprised if the Fed takes such an aggressive path again after awakening inflation from a decades-long slumber.

Interestingly, the Dow has now outperformed the Nasdaq 100 relative to their March 2020 lows.

With perhaps the distinction of relative performance of tech vs. cyclicals.

Normally, bidding long-duration treasuries would be considered a “risk-off” move, but I don’t think that holds in today’s market. Rather, it is speculative dip-buying of a falling asset, hoping for a rebound in price. If it’s yield you are looking for, short bonds pay much more.

It’s also possible that interest in volatility in recent years was borne of the same speculative fervor as meme-stocks or crypto, just betting on the opposite direction. Now, as speculative enthusiasm wanes, there is less interest in volatility.

RRP declines suggest plenty of liquidity left for bonds and stocks purchases. Any thought on how/why RRP balances could stabilize/grow again (and vacuum liquidity away)?

sell offs in fixed income now missing the FED bid so more of a two way market