Gray Rhino

#12: On China's debt and property crisis.

This post is the first in a two-part series on the ongoing Chinese debt crisis. This week focuses on China’s financial and property markets up until today. Next week, we will discuss the challenges on the horizon.

On June 17th, 2017, the front page of the People’s Daily, the official mouthpiece of the Chinese government, warned of a “Gray Rhino”.

The term, coined in a similarly titled book by Michele Wucker, refers to a highly probable, high impact yet neglected threat - a cross between an elephant in the room and a black swan.

The obvious, probable threat that the Daily warned of was excessive debt, which posed risk to the country’s financial stability. The editorial urged China to “strictly prevent risks from liquidity, credit, shadow banking and abnormal capital market fluctuations, as well as insurance market and property bubbles.”

The article grabbed the attention of local and international media as it was a striking rebuke of the economic engine that propelled the world’s most populous country to superpower status.

In the wake of the 2008 global financial crisis, China’s government unleashed a wave of fiscal spending and monetary expansion to maintain the country’s economic growth as the rest of the world languished in recession. Credit growth in China expanded rapidly, plugging the hole created by credit contraction in the US and elsewhere.

This approach was successful - China’s GDP would triple over the following decade, contributing to half of all global economic growth in the process.

But debt grew even faster.

By 2017, the total assets of the banking system (i.e. debt) had exploded to $38.4 trillion dwarfing the $16.2 trillion of assets held by US banks at the time, despite China’s substantially smaller GDP. In fact, half of all bank debt globally lived in China, yet the country accounted for only 15% of global production1.

In the words of the Center for Strategic & International Studies, “there is simply no historical analogy for a single country’s banking system expanding this rapidly compared to its own economy or to the global economy”.

Topline economic targets set by party leadership were achieved with brute force through endless investment in infrastructure and property. The cost was unproductive development, unsustainable debt, and financial risk.

Today, five years after the frontpage warning, China’s economy continues to expand2, debt continues to grow, and yet there has been nothing resembling a financial crisis.

But the Gray Rhino has only grown. China’s debt bubble is rotten and collapsing.

Confidence Game

The key to the China’s financial stability is also its greatest risk.

For many years the rapid expansion of debt came with very few defaults. Debts were always repaid. This impressive track record was not because of superior underwriting, but rather because of state support.

Lending to state-owned enterprises (“SOEs”), which make up the majority of industry, was the equivalent of lending to the state. It did not matter if these companies were profitable - many were not - because the credit was backstopped by the government. Even private companies were seen as having implicit support, given the de-facto state approval required to successfully operate a private entity in the country.

The backstop ensured financial stability, cheap credit and moral hazard.

While this dynamic worked well for a time, clearly it was unsustainable in the longer term as the costs of unproductive investment and graft would become too large to ignore. Beijing was faced with a dilemma: achieve growth targets through unproductive investment and inflate an ever growing debt bubble, or remove central support and test the sturdiness of the financial system.

Months after the Gray Rhino editorial, at the 19th National Congress of the Chinese Communist Party, Xi Jinping declared that houses are “for living in, not speculation”.

Together, these proclamations made the country’s intent clear and marked the beginning of a de-leveraging campaign that continues to this day. China would seek to rein in bubbles, roll back state credit support and reform its ballooning financial system3.

But talk is cheap - the critical question was whether debtors would be allowed to fail and lenders would be forced to suffer losses. If so, the ever expanding pile of debt would need to be re-priced for this reality, with financial upheaval a distinct possibility.

This question was answered by a growing drumbeat of defaults.

Cracks Emerge

The impact of Beijing’s de-leveraging pivot appeared quickly.

In 2017, HNA Group - a private conglomerate epitomizing the debt-fueled excess of the decade - began to collapse, ultimately leading to a protracted unwind that only recently concluded. HNA was the highest profile name among numerous private defaults from 2017 - 2018.

Then, in 2019 financial regulators were forced to take control of rural lender Baoshang Bank citing risks to the financial system; the first bank failure in 20 years. Despite Baoshang’s tiny size, the takeover sent shockwaves through the financial system. Eventually the Chinese central bank, People’s Bank of China (“PBOC”), was forced to intervene, providing liquidity injections to restore order to interbank money markets.

While the COVID outbreak in early 2020 brought a temporary reprieve to the crackdown as authorities cushioned the blow of the virus induced slowdown, it proved to be brief.

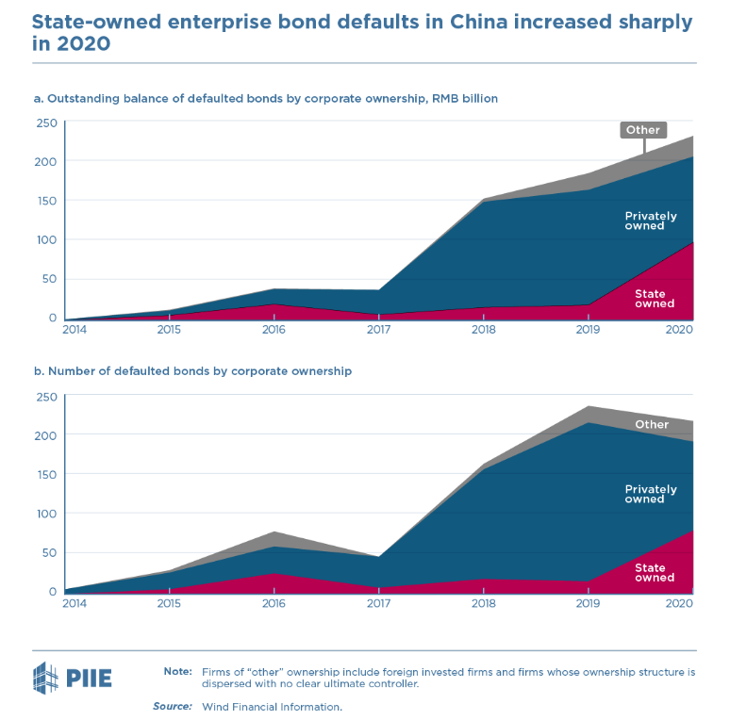

By the second half of 2020, it was clear the de-leveraging campaign would continue in full force. Defaults, which had been concentrated in private entities, spread to SOEs.

In late 2020, the defaults of AAA rated Yongcheng Coal and Electricity, backed by the Henan government, and Tsinghua Unigroup, owned by the Ministry of Education and central to China’s semiconductor ambitions, sent a clear message about the scope and resolve of the crackdown. No one was safe.

Meanwhile, in August 2020, authorities introduced the most consequential regulation yet, aimed at the heart of the country’s economy and the poster-child of speculation: property.

Three Red Lines

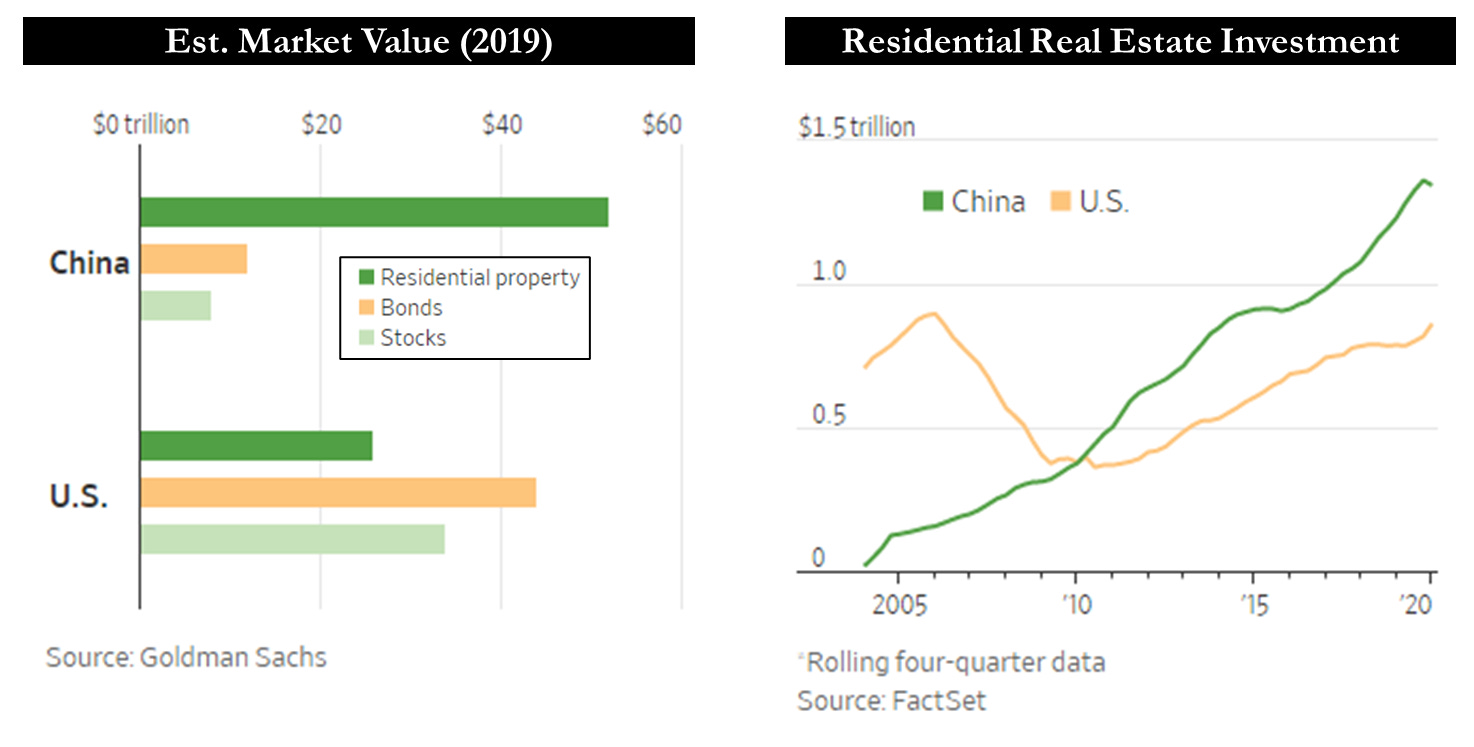

In China, property is the economy. In 2019, Goldman Sachs estimated the total market value of Chinese real estate at $52 trillion - making it the largest single asset class in the world, eclipsing the value of the entire US stock or bond market. The annual investment into residential real estate in China surpassed that of the peak US housing boom for seven years in a row.

Beyond its sheer size, property plays a critical role in the country’s development model.

Local governments auction state-owned land to real estate developers that use bank loans to fund the purchases. Land sale proceeds provide revenue to local governments that have limited access to tax revenue.

Developers then build massive apartment complexes on the land employing millions of construction workers and supporting an entire ecosystem of supply chains in the process. The apartments are sold to individuals who pay with mortgage debt or bank deposits. The majority of the wealth of billions of Chinese citizens is in property4, and it is not cheap5.

Property is the key channel for monetary circulation and economic development. It also represents the largest credit exposure of the financial system and the single largest abuser of cheap abundant credit.

In an attempt to rein in the industry and property bubble, financial regulators established the “Three Red Lines” in August 2020, which established strict limitations6 on property developers’ ability to borrow.

Very few developers could pass the three-pronged test, while many were on the wrong side of all three lines. As a result, developers were cut out of financing channels, which were critical for repaying existing liabilities and maintaining the broader monetary circulation chain described above.

Many of these developers were already insolvent but because of their access to financing, they managed to continue paying off old debt by incurring even larger sums of new debt. In other words, they were in a slow-moving debt spiral. Imposing leverage restrictions on a property developer in a debt spiral seals its fate.

Evergrande

In the same month that the Three Red Lines were announced, Evergrande Group, one of the largest and most indebted property developers in the country, sent an urgent letter to the Guangdong government. If a proposed financing fell through, it warned, the company may default on its debt, posing systemic risk to the $50 trillion financial system. When exposed in September 2020, the letter triggered a brief selloff in Evergrande bonds and related risky real estate debt.

The company managed to stay afloat into the new year, but by May 2021 reports emerged that it had begun to stop paying its suppliers. Bonds sold off steeply and would not recover. Today they trade at just 8 cents on the dollar.

During summer of 2021, all eyes were on Evergrande. While the company was clearly insolvent, the key question was how central authorities would handle the fallout. It was the highest stakes test of Beijing’s de-leveraging push.

Various theories emerged. Some thought it was simply too-big-to-fail, that Beijing would not dare risk an uncontrolled implosion of such a massive company at the heart of the critical property sector. Others expected that state-owned developers would be directed to digest the remnants.

By September it became clear that authorities would do nothing. There was no bailout for the company or its creditors. Evergrande would simply fail.

Evergrande’s failure reverberated through markets in China and abroad. The first order impact was $291 billion of liabilities on the balance sheet with dim prospects for recovery7 (which roughly equaled the entirety of bank losses associated with the US subprime crisis).

But perhaps more impactful was the effect on the market. The property market, which thrived on confidence and readily available debt, froze, along with the financing channels of strapped developers.

While previously the financial position of each developer varied to some degree, by September 2021 the entire cohort was no different than Evergrande - insolvent, and rapidly becoming illiquid.

Contagion

Evergrande was not the first or last property developer to fall - stress appeared in weaker names earlier in the year. But Evergrande’s final crash in September 2021 was the point of no return. Contagion gripped the market.

Land auctions went bid-less, homebuyers retreated, and financers pulled back. Cash strapped companies that may have been able to hobble along suddenly saw their cash flow dry up entirely. The desperate fire-sale of assets to raise funds only made matters worse by depressing apartment prices.

Contagion is a bubble in reverse. Contagion is a disease of fear and self-preservation that spreads through a market. It’s easier to see than describe.

The chart above shows the total return of USD bonds for eight enormous property developers; Country Garden, Evergrande, Sunac, Greenland, Shimao, Kaisa, R&F and Aoyuan8. All of these bonds are trading at cents on the dollar, as bondholders mull the prospects of minimal or no recovery9. Over 40% of USD bonds issued by Chinese developers are in technical or actual default, and this number will only grow. Together, just these eight companies have over a $1 trillion of balance sheet liabilities, not including off-balance sheet debts and construction obligations.

Attempts to stimulate the property market have failed - there is no light at the end of the tunnel, only darkness. And yet…

The Horizon

Despite all of the turmoil to date, the Gray Rhino has yet to truly rear its head. Unless you own the equity or debt of Chinese property developers, the direct damage has been fairly well contained. There has yet to be a chaotic disruption to China’s broad financial system and its $50 trillion banking system remains in tact.

Today, one could argue that Beijing has succeeded in tamping down the property bubble and crushing its over-levered property players without causing a nationwide calamity. For an international observer, it may be easy to dismiss the entire ordeal as unimportant.

Unfortunately, the story is not over. It’s entering its most critical act.

Next week, we will discuss banks…

Source: Credit and Credibility. If you are interested in learning more on this topic I would highly recommend reading this report and subsequent follow-ups, which provides much of the background information and framework for this analysis.

Although just barely, according to official statistics.

The country’s monetary path since then has not been a straight line - there have been two monetary easing and tightening cycles, with corresponding acceleration/decelerations in credit growth. Financial reforms have also been targeted at different segments of the credit system - originally focused on shadow banking, while since expanding further into property and bank lending.

The personal exposure to property goes far beyond the houses folks reside in. 96% of urban citizens own their property, and a large majority of new mortgages are for second, third or fourth properties. In many cases these are purely investment properties which sit vacant and unfinished - which is meant to preserve re-sale value.

On an absolute basis (price per square meter), China’s Tier 1 cities are the highest in the world. On a relative basis (price-to-income ratios), it is even more expensive. The highest risk markets though are rural cities that simply have no need for the volume of housing constructed.

The Three Red Lines are (1) 30% minimum equity vs. total liabilities, (2) net debt can’t exceed equity, and (3) cash must exceed short term debt.

This figure excludes any off-balance sheet or hidden debt which we know to be substantial.

There are plenty more companies that would not fit on the chart, but you get the point.

There is an important distinction between onshore and offshore bonds that will be discussed next week. The bonds quoted here are offshore USD bonds because the data is more transparent and available.

Great article, looking forward to part 2. Your posts are a joy each Friday morning. Very much appreciated.

Fantastic! I really enjoy your work on the Chinese real estate bubble.