Behind the Curtain

#100: I need your help! Plus, black and yellow gold.

I think there are four great motives for writing, at any rate for writing prose. They exist in different degrees in every writer, and in any one writer the proportions will vary from time to time, according to the atmosphere in which he is living. They are:

(i) Sheer egoism. […]

-Why I Write, George Orwell

Behind The Curtain

A grating tendency of blogs such as this, particularly ones that have seen some success, is that the blog becomes a bigger focus than the content itself. There is an understandable but self-congratulatory air to the whole thing — updates on subscribers, growth rates, annual revenues. Maybe it’s smart marketing, maybe it’s pure back-patting.

For the most part, I hope to avoid this temptation. Perhaps that’s a testament to humble restraint. More likely, it’s because I don’t have enough to brag about.

But since this is the 100th installment of The Last Bear Standing — nearly two years of continuous publication — I want to take the opportunity to pull back the curtain on my own process, and how I hope to improve moving forward.

Two years ago, I sat at dinner with two pals, fretting about the future. I had, in theory, decided to write this column but hadn’t started writing this column. First, I needed a foolproof master plan, a perfect vision of exactly what The Last Bear Standing would be. But big-picture brainstorming can be paralyzing and often serves as a convenient front for procrastination. In my case, both were true. A swift kick in the tush was required, and fortunately, my friends delivered.

The next week, The Last Bear Standing was born. The inaugural installment didn’t come with a foolproof master plan, but instead established the single cardinal principle which continues to guide the publication today — it comes out every Friday morning.

[A quick housekeeping note, some readers have reported issues receiving emails in recent weeks. Please let me know if this is the case so I can help troubleshoot. If you don’t see TLBS in your email inbox on Friday, the posts are always available at www.thelastbearstanding.com]

With the exception of its weekly distribution, there is no fixed template, consistent structure, regularly updated charts or signals. Every week, I try to choose a topic in finance or economics with sufficiently broad interest, for which I also have something original to add. I try to present information in an engaging and accessible manner and budget at least one chuckle. If I think I have found a good idea, I will write about it eagerly. Some weeks feel like striking gold and others feel like scraping pennies — oftentimes readers think the reverse. For better or worse, each week tends to be its own adventure, with only winking references to the running plot.

This latitude has allowed me to bounce between monetary and fiscal policy, macroeconomics, industry primers, market commentary, and single-stock analysis. Personally, I appreciate this flexibility and my impression is that some readers also enjoy the variety.

But this also comes with a cost. Over time, the tone and content ebbs and flows, partially due to the ever-changing landscape of relevancy, and partially due to my own evolving interests. Different readers sign up with different expectations, background knowledge, and intentions. And, of course, I am constantly feeling around for new angles, hoping to develop a compelling and successful product.

Dialing in on a winning formula has been a process of trial and error. The selection, research, and writing process is a black-box to readers. Meanwhile, the feedback I receive is mostly quantitative — denominated in likes, subscriptions, and conversions. But these signals can be contradictory and suffer from tiny samples and selection bias.

The biggest challenge, it seems to me, is that I just don’t know my readers well enough. There are thousands of people who at least open my weekly updates, but other than a select few, I have no idea who you are, why you are reading, and what you hope to get out of it.

So to help make The Last Bear Standing a better product for the next 100 installments, I’m asking you to take one quick minute to complete the very brief survey at the link below. I promise it is painless.

The Last Bear Standing Reader Survey

While I don’t anticipate a dramatic shift in format (unless it is widely demanded), I hope that a better feedback channel will make this publication more valuable for you. Frankly, I also just want to get to know you better.

Doubling Down

Other than a Friday distribution, a second parameter for The Last Bear Standing is a refrain I’ve repeated from the beginning: If you keep reading, I will keep writing. Or, so long as this column continues to attract readers and remains viable, I will continue to produce it.

After two years, I’m happy to report that this column is viable and I’m always thrilled to hear encouraging words from readers. But I feel that it has only begun to scratch the surface of its potential.

Rather than taking my foot off the gas, I’m taking this milestone as an opportunity to double-down — to recharge and refocus on producing the best possible content moving forward. Reader feedback is a big part of that push, but much of it will simply come from my end.

Finally, I want to thank you for reading and supporting this effort to date. The best is yet to come.

Now, I wouldn’t leave you without some quick market talk, would I?

Black and Yellow

The inflation trade is back in full swing. The Consumer Price Index notched yet another hotter-than-expected print this week and economic data remains robust. Rate cuts continue to get priced out of the forecast, sending yields higher across the US Treasury curve. There is even a growing cadre that is adamant that the next Fed move will be higher not lower.

In the past two weeks, yields have risen ~20bps across the board. Since the turn of the year, the 10-year yield has risen 75bps driven by an increase in near-term rate outlook and now trades closer to five than four.

But unlike the back-half of 2023, where stocks and bonds rose and fell together, this year stocks have stomached the rise in rates with only slight indigestion. At the index level, the S&P 500 (blue), Nasdaq 100 (orange), and Russell 2000 (teal), have posted similar gains since rates peaked and stocks bottomed in late October, even as long-term bonds have traded off significantly (TLT in red below).

Underneath the surface though, there has been a significant rotation that reveals inflation agita. Hard commodities, in particular black gold and yellow gold, have ripped higher since early March.

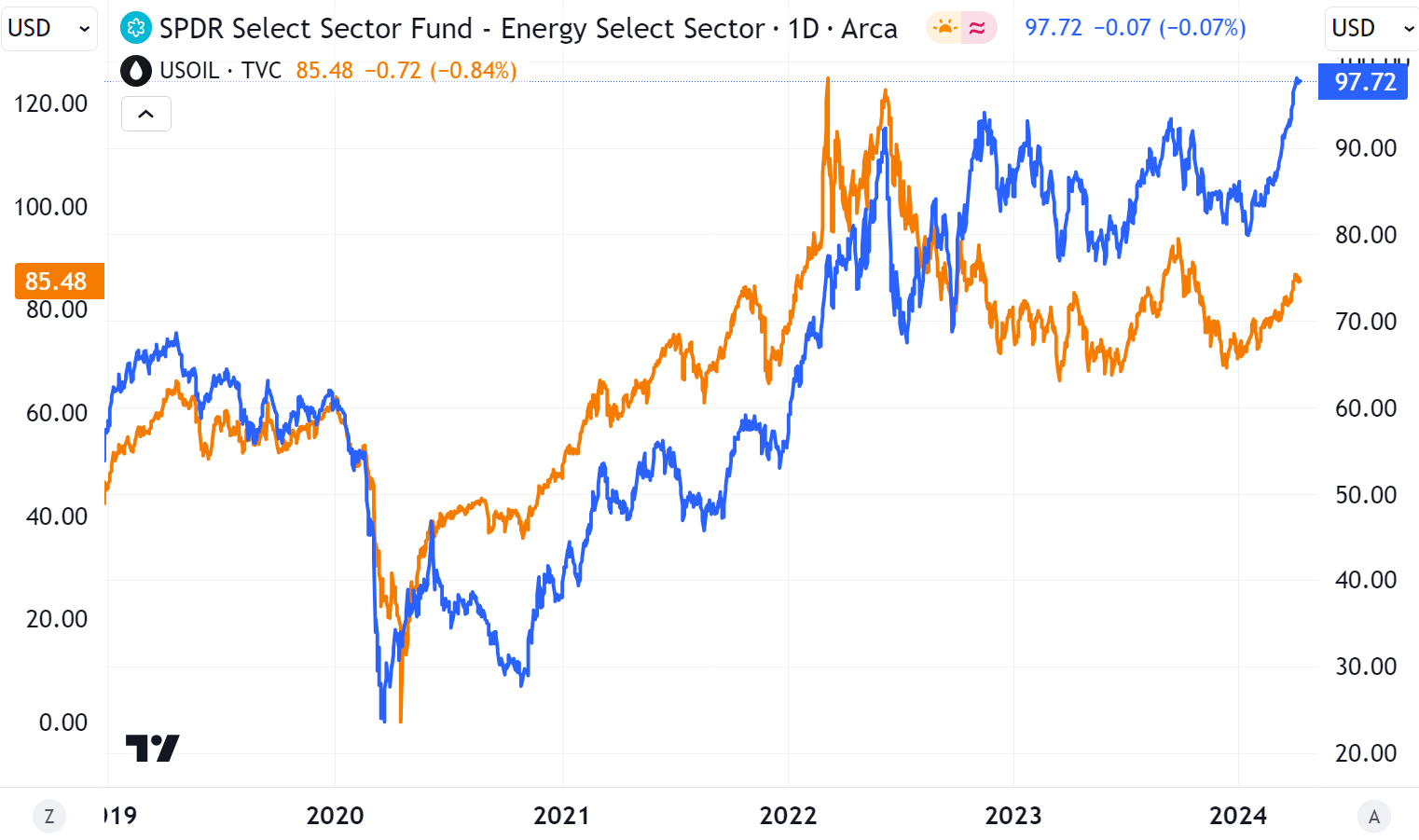

The energy complex (XLE, yellow line below) is now the best performing S&P 500 sector year-to-date (+15.3%), while rate-sensitive real estate is the only sector in the red.

Energy has broken out to new all-time highs, even as WTI crude hovers below $90 per barrel, well below 2022 peaks. But don’t call it pricey yet. At 13.2x 2024E operating earnings, it is still the cheapest sector in the index at a ~40% discount to the average multiple of 21.9x (per S&P Global).

Interestingly, XLE seems to trade with a stronger (inverse) correlation to long-term interest rates (shown via TLT in red below) than it does to the underlying commodity, oil (orange above).

Precious metals have also caught a massive bid over the past two weeks, with gold and silver now outperforming stocks on a year-to-date basis. After a rough start to the year, even the miners (GDX, GDXJ) have caught back up to the underlying commodities.

While gold, silver, and miners were featured in my 2024 trade ideas, I clownishly renounced the idea in mid-February on poor performance, just before it got started. So it goes.

But on a longer term perspective, the gap between gold and gold miners continues to widen, perhaps the subject of a future deep dive.

Broadly though, there does seem to be a regime shift afoot. The joyous rally that has propelled stocks since October has been endorsed by the expectation of a soon-to-be-easing central bank. But now even staunch disinflationary activists have been forced to acknowledge that progress towards a 2% target has stalled out quite prematurely. The balance of evidence increasingly points towards higher inflation moving forward, not lower. The Federal Reserve seems to be the only truly sanguine party, but this fortitude will be tested if the inflation readings don’t subside very soon.

As I’ve written over the past several months, a strong-growth / high-inflation is not necessarily a bad backdrop for stocks. But given that valuations have already jumped several turns in this rally, it does seem like some consolidation is appropriate. Indeed, most sectors are mostly flat over the past six weeks. But maybe more interesting to watch is whether the rotation into inflation winners (commodities) continues as rate-cut hopefuls (banks, real estate) are forced to contemplate the possibility of >5% long-term yields.

Finally, if you skipped it above, here is the link to the reader survey again. Other than your hard-earned money, what do I ever ask of you?

The Last Bear Standing Reader Survey

It has been a great challenge and privilege to write for you. Thank you, as always, for reading.

Gratefully,

The Last Bear Standing

Love reading this substack first thing every Friday morning. Keep up the great work

Dear John,

I am looking for excellent writers about among others nuclear energy. I want to translate your articles into Dutch (which I'll pay).

Could you reach out to me via pieter@compoundingquality.net?