Banking on Pressure

#53: On policy, liquidity and solvency - and what comes next for U.S. banks.

A bank is just a pile of cash and a lot of math.

The pile of cash is important to cover daily needs like interest expense, customer withdrawals, or payroll.

The math is also important. Tallying up all the money that is owed to the bank and that the bank owes to others ensures that the cash pile will be sufficient in the future.

Both liquidity and solvency are critical. If bank customers or investors have concerns about either, they may pull their funds or dump the stock. Solvency concerns can lead to liquidity scrambles and vice versa.

For the U.S. banking sector today, there is pressure on both sides of the equation.

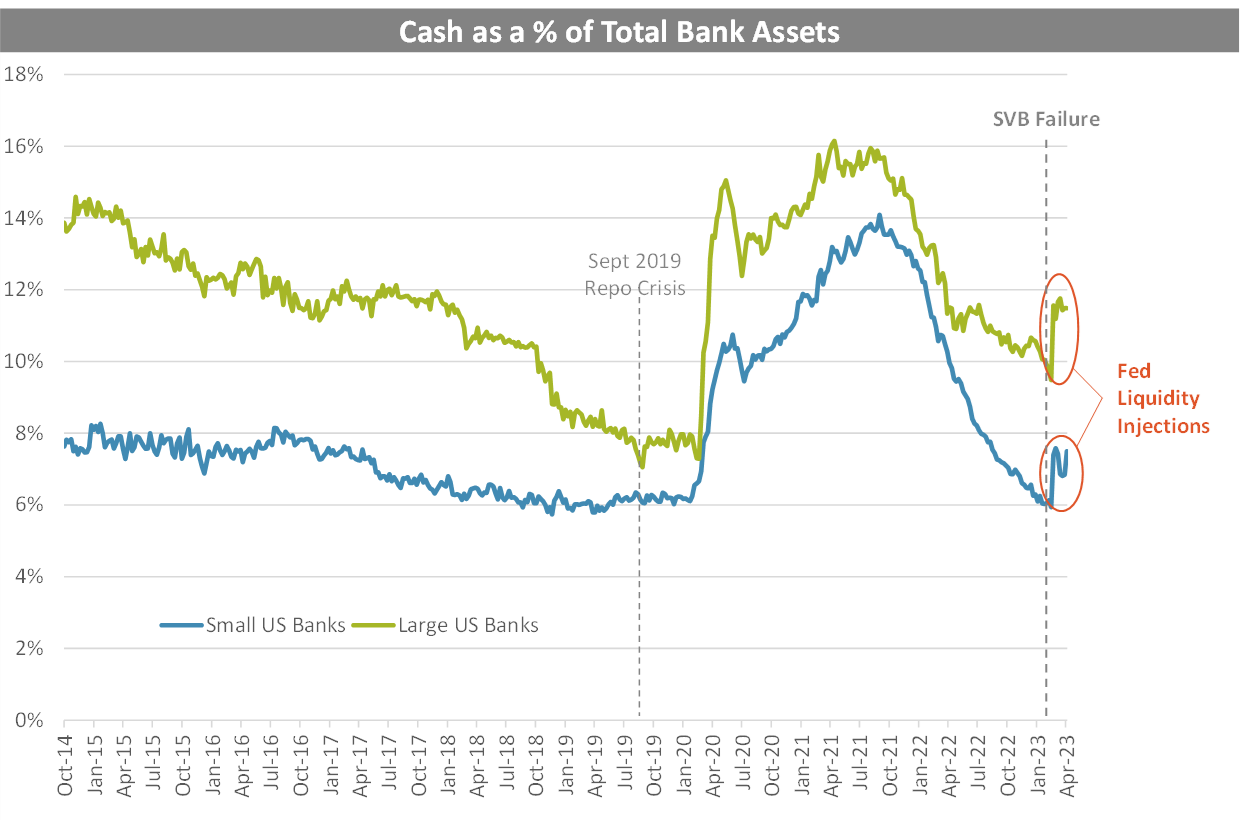

Cash liquidity in the banking sector has seen a remarkable round-trip during the past three years, surging during the pandemic but falling since late 20211. Even prior to the official wind-down of Quantitative Easing (QE), much of the “excess” liquidity at banks had already been absorbed by the Fed’s Reverse Repo Facility (RRP). Then, Quantitative Tightening (QT) began to shred dollars up to a maximum clip of $95 billion per month2.

By March 2023, cash as a percentage of total bank assets had fallen substantially, returning to near pre-pandemic levels. The week before Silicon Valley Bank’s (SVB) collapse, total cash in the banking sector fell below $3 trillion for the first time since October 2020.

While measures of aggregate liquidity may not appear stretched relative to the historical series, cash reserves are not equally distributed across all banks. The weakest link breaks first, especially when paired with solvency concerns.

Fear of insolvency at SVB prompted a digital bank run - an enormous demand for liquidity that could not be met through private means alone. Instead, Silicon Valley Bank, First Republic, and others tapped the lender of last resort - the Federal Reserve - including the discount window, Bank Term Funding Program (BTFP), and other channels3.

These temporary borrowings buoyed banking cash, albeit at high cost to the borrowers. While this band-aid added nearly $400 billion to the banking sector, the underlying dynamics that have drawn down bank liquidity for nearly 18 months have not changed. QT remains on schedule.

Meanwhile, higher interest rates have meaningfully impaired the market value of banking assets. The chart below shows the implied mark-to-market (MTM) equity capital of publicly traded mid-cap and regional banks, relative to their reported book equity balances (as of year end 2022).

While the root cause is higher rates, the magnitude of the impact on equity balances depends on the managerial decisions of the bank - the duration, rates, and terms of its asset book. The worst offenders - FRC and SVB - have already gone under, but we see that numerous other banks have negative or minimal capital on a MTM basis. The average MTM equity capital of mid-size public banks is about half of their stated book value, if they were forced to sell their assets today.

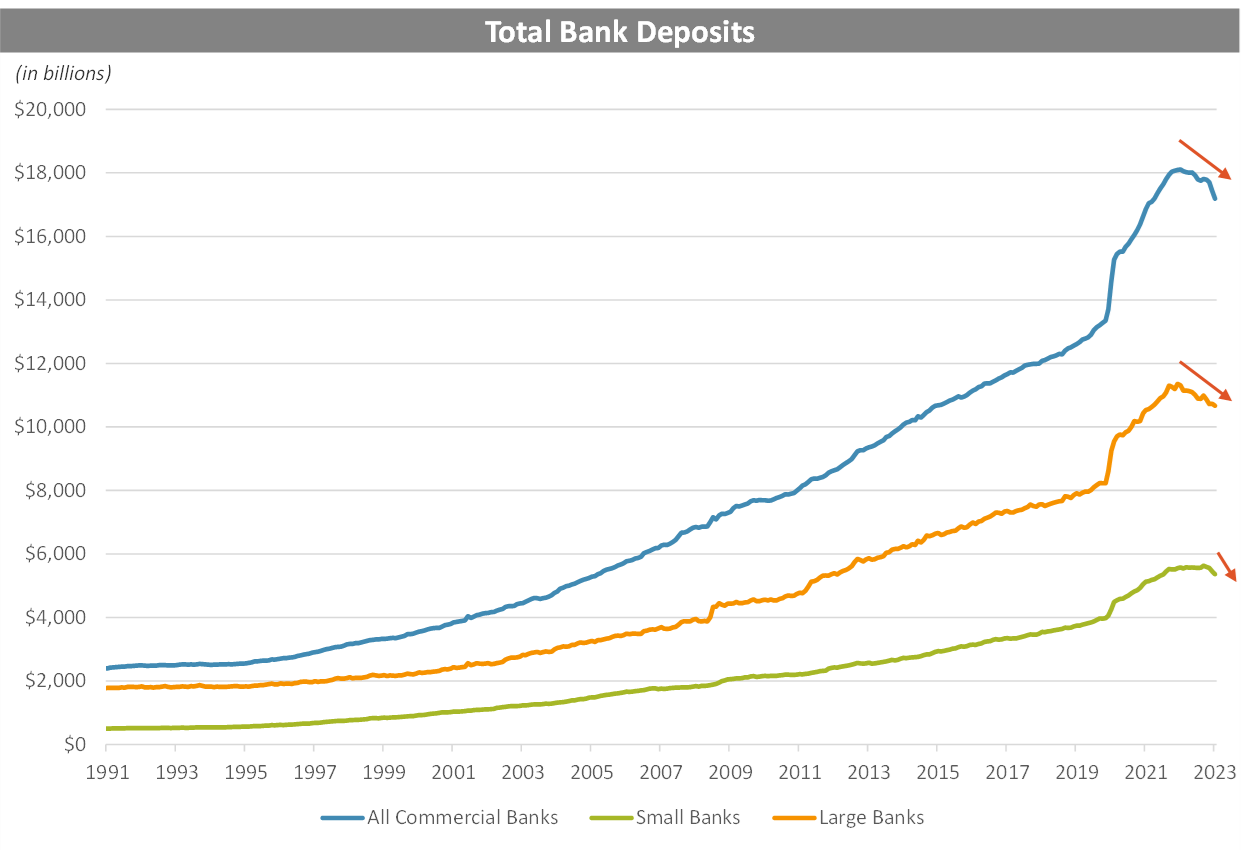

Normally, banks don’t need to sell assets. Bank assets grow constantly along with growing deposits. But we aren’t in a normal environment. Today, bank deposits are shrinking, and therefore banks are being forced to liquidate assets and crystalize losses.

Further, these MTM values are based on a deeply inverted yield curve. If the Treasury yield curve were to flatten towards the short-term policy rate of over 5%, it would render many of the weaker banks insolvent on a MTM basis and would push the overall average closer towards zero.

In other words, the solvency of a wide swath of mid-size banks depends on the market’s continued pricing of future rate cuts as well as the assumption of sticky deposits - neither of which are consistent with the Fed’s current policy.

Deposit Flight and Yield Chasing

In the wake of recent bank failures, there has been renewed focus on aggregate bank deposits. Bank deposits are falling for the first time since at least 1975 - the earliest date of the Fed’s dataset.

Yet, many explanations of this dynamic seem to miss the mark. Some have suggested that depositors have woken up to the de-facto government backstop enjoyed by large GSIBs and are pulling money from smaller institutions that lack such support. But this is backwards.

Aggregate deposits peaked all the way back in April 2022 and have fallen the fastest at large banks. In the case of SVB, it was the decline in deposits that forced the bank to liquidate its securities holdings, which wiped out its equity capital by realizing losses, which then spurred an acute bank run, putting money into the hands of JPMorgan and crew. The final phase was merely the dramatic finish, which would not have occurred without the slow-brewing and largely ignored bank stress of the prior year.

The true story of deposits is much simpler. Since the beginning of 2020, QE and QT have resulted in a nearly 1:1 change in aggregate bank deposits. The cumulative change in the Fed’s System Open Market Account (SOMA) portfolio (i.e. the total of Fed’s UST and MBS holdings) clearly explains both the creation of deposits during QE and the destruction of deposits during QT.