Value to Mine

#126: An analysis of the large-cap gold miners.

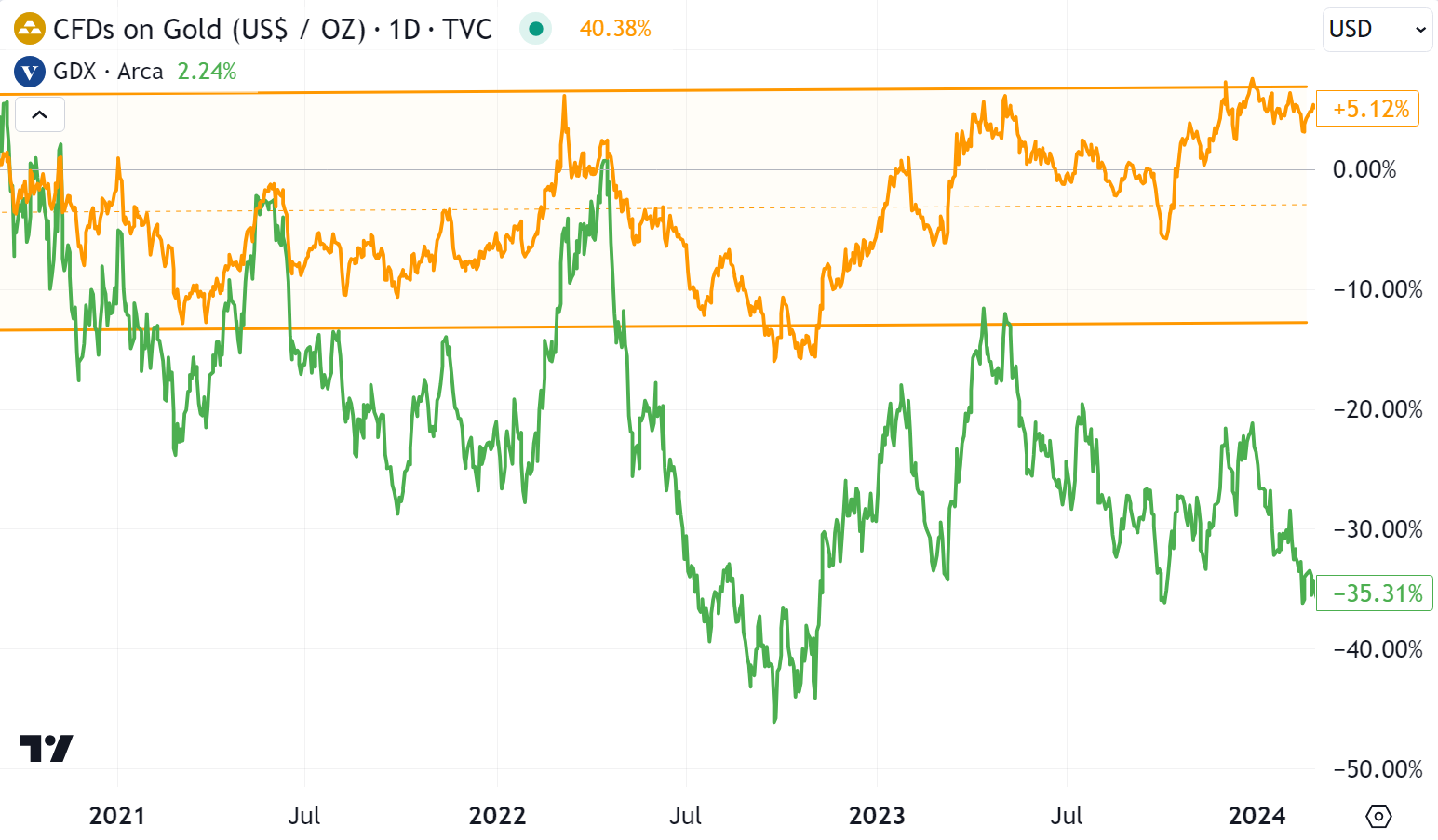

As the global monetary easing cycle begins, the price of precious metals has soared. Yesterday, gold traded at a new all-time high—over $2,700 per ounce—up 32% since the start of the year, even outpacing a monster year for U.S. stocks. Gold miners have followed bullion higher, rising 36% year-to-date.

Despite these gains, it’s unclear whether gold miners have fully priced in the rally. Higher sales prices directly increase top-line revenues, but operating leverage magnifies the impact on bottom-line profits. In other words, miners provide levered exposure to gold, potentially appreciating faster than the underlying.

But rising operating costs and capital requirements can offset the benefit of higher commodity prices. Over the past several years, increased costs for energy, capital equipment, and labor have significantly impacted mining earnings and stock prices, even while gold prices remained relatively stable from late 2020 to 2023.

Further, individual gold miners differ in key areas — margins, capital needs, and production growth. A simple correlation between the gold price and mining shares ignores these dynamics and can’t alone serve as a valuation. And today there is a significant gap between miners lagging financial results and current spot gold prices, complicating trading metrics.

In this 126th installment of The Last Bear Standing, I climb into the pits of seven of the largest publicly traded gold miners — representing a combined $212 billion in enterprise value. I segment these companies into three distinct tiers, project their earnings potential at today’s prices, and provide a valuation under a variety of conditions. One stock in particular stands out.

In short, there appears to be value in gold mining stocks today — if you know where to look.

Let’s dig in.