The Second-Half Script

#111: A mid-year check-in on markets.

We entered 2024 on a growing wave of confidence, fueled by easing interest rates, solid macroeconomic performance and thematic excitement for new technology. So far, there has been little negative news to derail the rally. Job growth and consumption have remained positive, and corporate earnings are rising. On Wednesday, U.S. stocks closed at all-time highs.

All major U.S. equity indices have notched positive performance, but the outsized returns of the Nasdaq and S&P 500 have been driven by the outperformance of mega-cap tech. The equal-weighted large-cap Dow Jones has provided only a marginal premium to the risk-free rate, while the small-cap Russell 2000 is nearly unchanged.

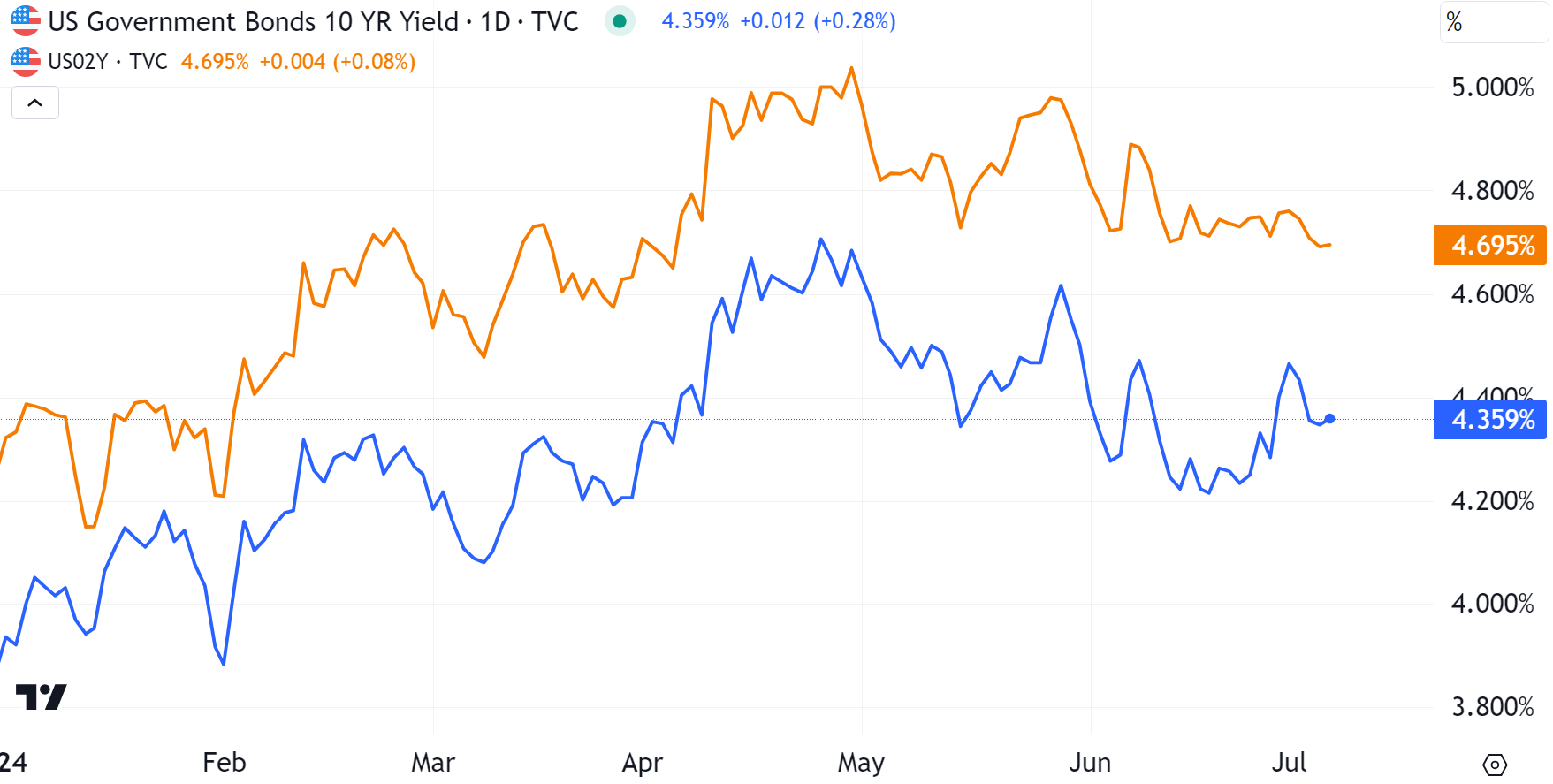

A series of hot inflation prints pushed U.S. Treasury yields higher through April — the likely culprit behind the only meaningful stock slump of the year. But cooler price prints combined with some growth concerns over the past two months have taken the edge off as bonds across the curve have rallied. The 10yr - 2yr spread has remained inverted for two full years — the longest streak in data going back to the mid-1970s — and shows few signs of reverting.

The rally has been global. All major stock indices around the globe have risen, though have generally lagged the S&P 500.

So far, markets have rewarded index riders, crowned momentum traders, and left skeptics screaming into the breeze. For plus-sized returns, buy the market and a daiquiri. For mega-performance, find a vertical chart and mortgage the farm. Heck, with cash at 5%, the yields on the sidelines aren’t too far behind. The only true sin has been to fade optimism — betting against market leaders, or betting against the economy with long-duration bonds.

In other words, go with the flow. While it may irk some readers seeking the titular promise of this column, I hope that my invisible hand nudged folks to the right side of these dynamics this year.

But easy markets don’t last forever. The 55% index rally over the past 20 months has been driven by a confluence of improving factors — rising valuations, easing volatility, stimulative policy, and steady economic growth. Having successfully climbed a wall of worry, where are the next rungs higher?

As we enter the second half at all time highs, here are the major themes that I expect to define the remainder of the year.