The Inside Game

#36: Insiders, Outsiders, and the Great Pandemic Bubble.

In a bubble, there are two games being played, an outside game and an inside game.

The outside game is the sermon of the true believer. You hear the outside game on podcasts, YouTube, Twitter, and from that wacky friend from college. The message will sound radical, almost too crazy to believe, but just take a moment to hear it out. Disruption. Innovation. A new paradigm. Everything is changing - what matters today will be worthless tomorrow.

The path of the true believer will be rough and windy. Only the most courageous soul will conquer. The cardinal rule is simple: Never sell. Diamond Hands. HODL.

The inside game is a bit more complicated. The inside game recognizes and exploits a zero-sum game of social contagion. The asset in question - and any concept of valuation - is irrelevant. What matters is how much hype you can generate and how many new outsiders you can lure. The essential tools are human emotions: greed, jealousy, and fear (of missing out).

Unlike the outside game, where the timing is supposedly irrelevant, the inside game is almost singularly focused on timing. And unlike the outside game, where selling is the cardinal sin, the entire goal of the inside game is to sell.

Outwardly, both players profess the same goals on the way up and believe they are on the same team. The positive feedback loop is mutually beneficial. More buyers drive prices higher, luring more buyers, and so on. Even at the top, both the insider and the outsider will feel rich, though with a critical difference.

The outside player feels rich because of the mark-to-market (MTM) value of their assets - the implied value of their portfolio, if they were to sell. The insider gets rich by selling. Ironically, MTM wealth is merely the outside player transitively and superficially experiencing the true profits of the insider.

Take Carvana (CVNA), the revolutionary used car dealer with its famous vending machines.

In less than two months from June to August 2021, insiders at Carvana sold 2.4 million shares for $802 million in proceeds - a weighted average selling price of $333.09 per share.

Today, the stock trades for $4.70, down 98% from its all-time high. The equity value of the entire company today barely exceeds the proceeds from those insider sales just over a year ago.

Take the King of SPACs, Chamath Palihapitiya.

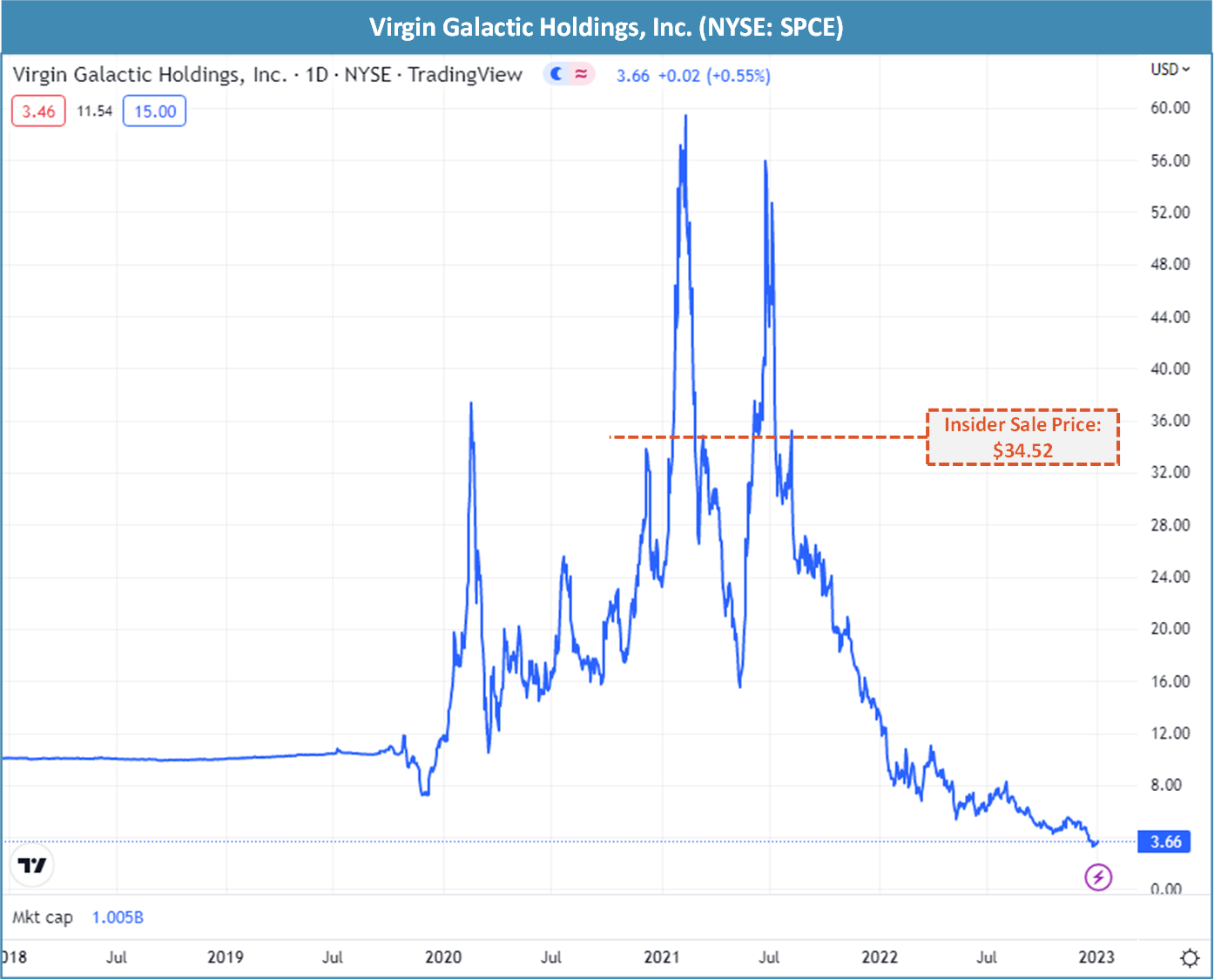

Just a month after proclaiming himself the next Warren Buffett while pumping his SPACs on national TV, Chamath sold $212 million of Virgin Galatic (SPCE) at a price of $34.52 per share. Today, the aspirational space company trades at $3.58, down 94% from its all-time highs and down 90% from the Social Capital chair’s selling price.

In the height of the mania, private company insiders’ urgency to access exit liquidity of public markets was palpable.

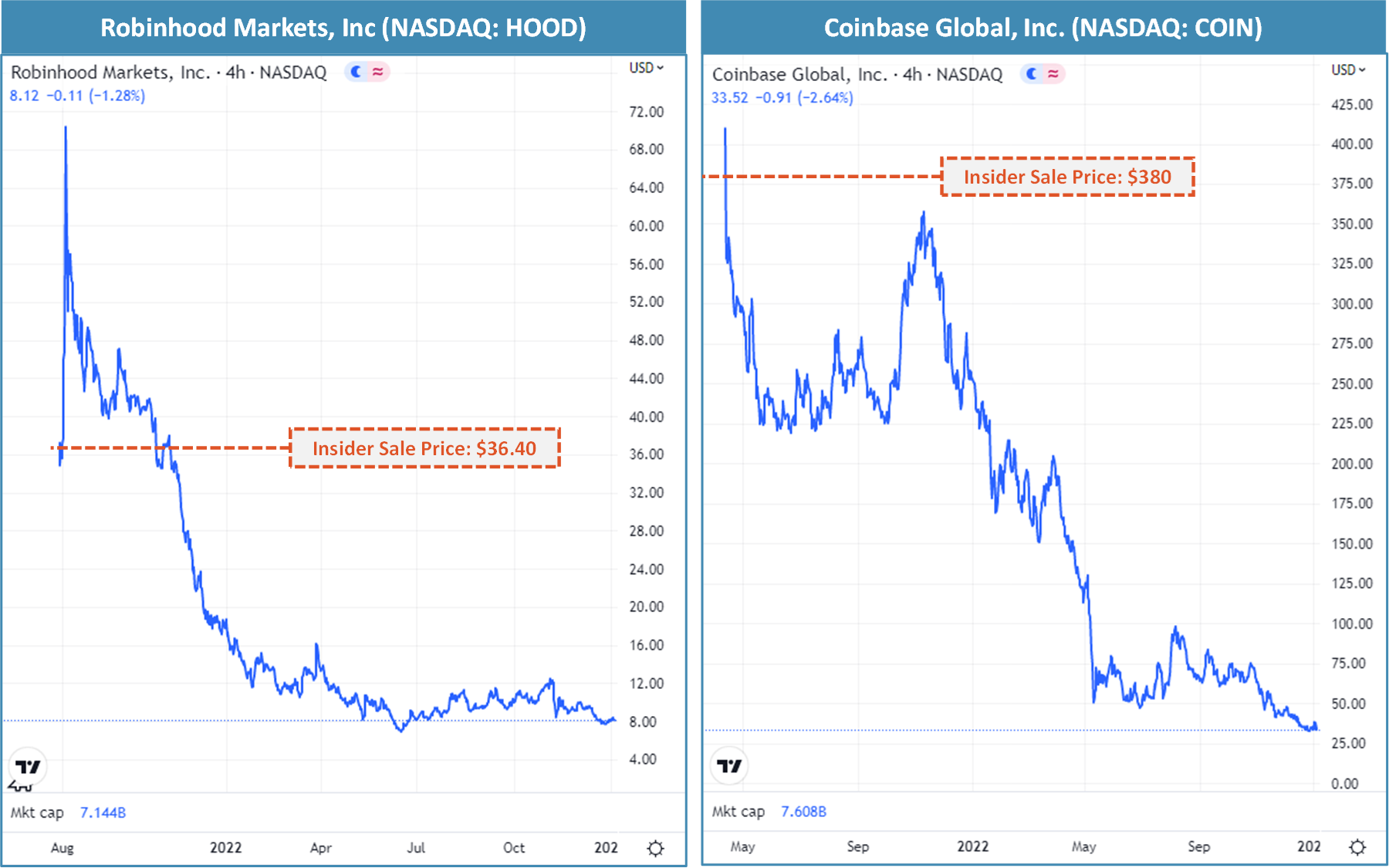

Take Robinhood (HOOD)1 or Coinbase (COIN) - each rushed to a public listing with unique terms, allowing insiders to avoid the pesky lock-up periods customary in IPOs.

In Robinhood’s IPO, insiders sold over $100 million, including $45 million apiece from its two founders. Today, HOOD trades at $8.11, down 78% from its IPO price.

In Coinbase's direct listing - a unique maneuver specifically designed to maximize insider sales - sophisticated VCs like Union Square Ventures and Andreessen Horowitz sold nearly $2.2 billion worth of stock in the first week at an average price of $380 per share. Today, COIN trades at $34.72, down 91% from that average sale price.

And, then of course, there is the Technoking of Tesla, Elon Musk. Elon began selling shares on November 8, 2021, just days away from Tesla’s all-time high. In total, Musk has liquidated his over 117 million split-adjusted shares for proceeds of $31 billion at a weighted average of $262 per share.

Today, TSLA trades at $110.34, down 57% percent from Musk’s sale price, and 73% off its all-time high2.

Sure, these insiders still hold equity in these downtrodden stocks today. Yet, rather than evidence of ongoing “skin-in-the-game”, it merely shows how wildly profitable it can be to sell into the peak of a bubble. You only need to get off a fraction of your ownership to make tens of millions or billions. Even if the rest goes to zero, you can still come out on top.

These handful of notable examples barely scratch the surface of similar examples on regulated securities exchanges. And we won’t even begin to discuss the realm of pink-sheets, penny stocks, crypto, NFTs, etc.

Opportunists and Opportunity

These examples have a few things in common. The companies were supposed disrupters of entire industries, set to usher in a “new era” for a “new generation” of consumers and investors. Their insiders were often high-profile personalities with social prestige and influence. And, of course, they generally came from the broader Venture Capital / Silicon Valley world, an entire industry based around profitably selling equity rather than profitably selling products.

Wall Street and asset managers were happy to clip unprecedented fees along the way.

It is reasonable to question the ethics of these folks, even if their actions were strictly legal. Maximizing hype and luring new outside investors is a critical ingredient to success. Many of these investments were aggressively and directly marketed to the most easily persuaded and inexperienced investors in interviews and on social media. We are rich, don’t you want to be like us?

All, to some extent or another, were preaching the outside game while playing the inside game.

But that also isn’t the full story. Even ethically dubious opportunists must be presented opportunity. It takes two to tango.

In normal circumstances, IPOs don’t double on their debut, unprofitable companies don’t fetch $100 billion valuations, and car companies don’t trade at 100x earnings. These conditions are rare and only occur when wide swaths of the market and broader public throw caution and reason to the wind.

For every spoonful of overvalued equity, there was a mouth eager to gobble it up. Both players ultimately motivated by the same end goal - get rich, The American Dream. But some played the inside game, and others were fooled.

And we would be remiss to not mention perhaps the biggest losers of them all - the sorry skeptic who saw asset values becoming unanchored without recognizing the powerful force behind the movement. The lone martyrs who tried to run against the stampede were trampled in the earliest innings.

Herd Immunity

Nothing in the Great Pandemic Bubble was new. Financial bubbles are studied by academics and taught in school. Tulip-mania, the South Sea bubble, the roaring twenties, and the dot-com mania are all common cultural touchstones. Pump-and-dump scams are featured in Oscar-nominated blockbusters like The Wolf of Wall Street.

Remember Aerotyne International?

It is a cutting edge high-tech firm out of the Midwest awaiting imminent patent approval on the next generation of radar detectors that have both huge military and civilian applications now. Right now, John, the stock trades over-the-counter at 10 cents a share. And by the way, John, our analysts indicate it could go a heck of a lot higher than that. Your profit on a mere $6,000 investment would be upwards of $60,000!

But both biological viruses and social viruses spread easily through an uninoculated population. Perhaps it’s not a coincidence that the last true stock bubble came twenty years earlier - one full generation.

There is a difference between reading about a bubble and living one - feeling the tug of emotion on the way up, the feeling of being left behind, and thinking this time may really be different. And like a biological virus, it is only after a critical mass has been infected that cases rollover and begin to fade away.

Now the insiders have cashed out, outsiders hold bags, and sorry skeptics are still being scraped off the pavement. Perhaps this generation has finally earned its herd immunity from the madness of the crowd.

See you in 2040.

As always, thank you for reading. If you enjoy The Last Bear Standing, like this post and tell a friend! And please, let me know your thoughts in the comments - I respond to all of them.

-TLBS

Robinhood, in my opinion, is the epitome of the brazen deception of the inside game. Every single aspect is almost too on-the-nose. The name implies the poor will steal from the rich. In reality, Robinhood's customers are the world’s largest hedge funds, and the product is novice traders who have been steered into options trading. Reading HOOD’s IPO marketing materials should make a decent person blush. Even the timing of the IPO, snuck in just under the wire before being required to provide 2Q21 earnings (which were a disaster). I’m sure some analysts at lead underwriter, Goldman Sachs, were probably sitting there thinking, “wow, this seems kinda messed up”. But hey, it’s Wall Street not Sesame Street.

It is fascinating today to watch the most public Tesla promoters now lashing out at Musk, and Musk simply trolling them with tweets of NPV formulas and “Securities 101” lessons, as if to say “did you not know what game we were playing?” I had always assumed that these promoters were “in on it” or at least savvy enough to take profits.

Your writing is just incredibly good. It took all of my willpower during this mania to avoid becoming an outsider bag holder, and I quickly learned not to stand in front of an oncoming train either, so I avoided the fate of the sorry skeptic too. A large part of this was due to voices like yours, wafting silently through the orgasmic shouting of the euphoric bulls. Thank you!

This analogy is fantastic! “But both biological viruses and social viruses spread easily through an uninoculated population. Perhaps it’s not a coincidence that the last true stock bubble came twenty years earlier - one full generation.”

Really super piece as usual. Particularly, with my 28 years in FM’s it rings exact.

Wishing you, health, patience and prosperity for 2023.