The Great Rotation

#112: Big-tech trounced, small-caps bounce, breadth gets bullish.

If you have been waiting for a tell, wait no longer. The great rotation is here.

On Thursday morning, the Bureau of Labor Statistics reported deflation. For the first time in nearly two years CPI fell sequentially, the lowest month over month reading dating back to May 2020. The dip in price levels pushed year-over-year inflation ever so slightly below 3%, reaching a two-handle for the first time since March 2021.

Maybe more importantly, Core CPI excluding food and energy eased to just 0.065% month over month (0.8% annualized), the lowest level since January 2021. And while the YoY change in core prices still lags headline CPI, the trend has resumed a decidedly disinflationary path after brief hesitation last quarter.

While stubborn inflation prints early in the year forestalled the eagerly-anticipated rate cutting cycle, a “data-dependent” Federal Reserve is no doubt dancing a little jig. Armed with several months of supportive data across CPI, PPI, the PCE price index, and ISM prices paid surveys, the United States may finally follow the lead of the European Central Bank, Bank of Canada, Swiss National Bank, and Sweden’s Riksbank in rate cuts. The dollar fell against global currencies on the dovish data.

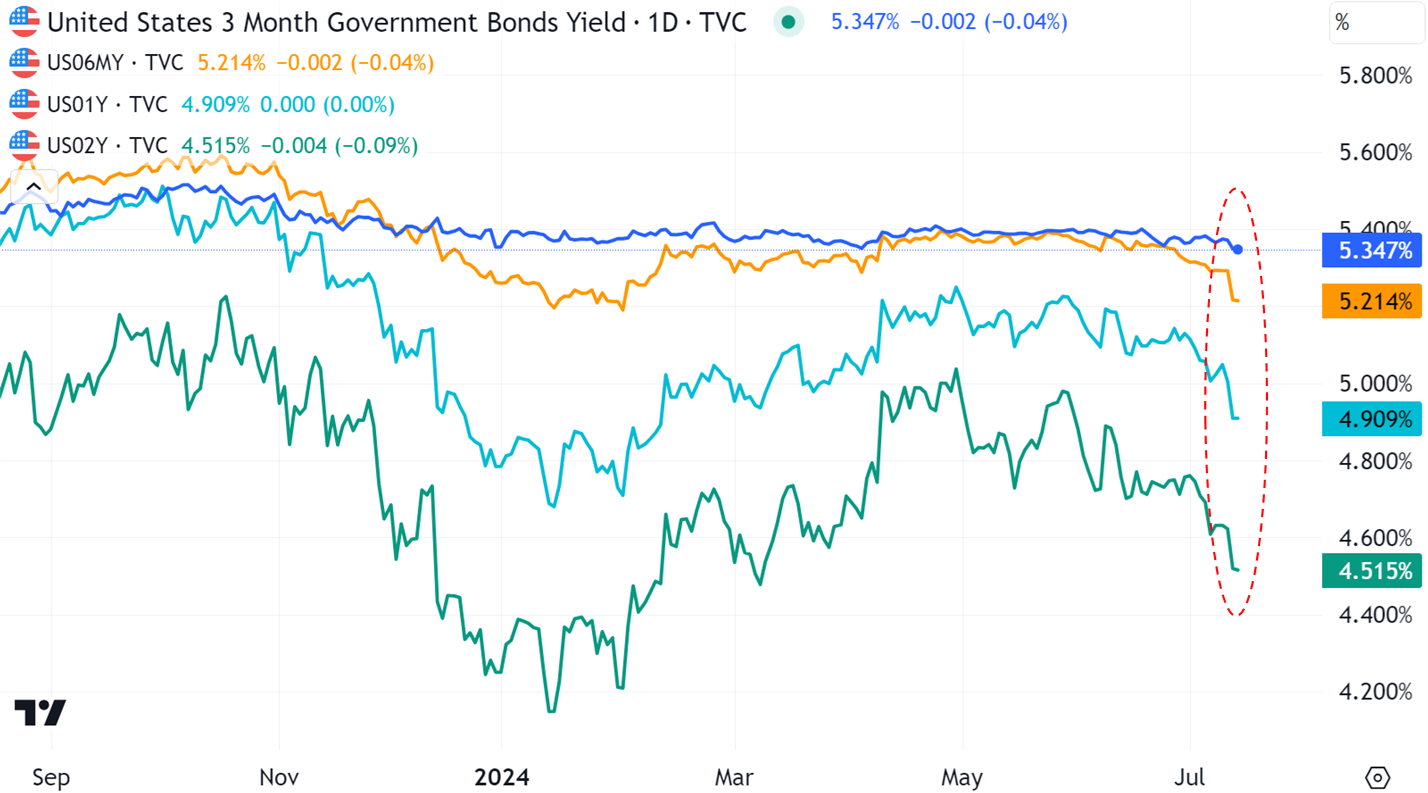

Even as the most recent dot-plot only showed a single rate cut in 2024, easing inflation combined with a creeping unemployment rate theoretically makes each upcoming FOMC a live meeting. Short term interest rates confirm. Both U.S. Treasury yields and SOFR futures plunged as the odds of rate cuts rise.

On the Treasury curve, the biggest move came in the 6-month to 2-year tenors, with the 6-month bill yields tumbling 8bps in the biggest move since the Silicon Valley Bank collapse. At a yield of 5.21%, 3-month bills point to a September rate cut — the first since early 2020 — with the current 6-month yield hinting at the possibility of a second cut by year end.

Similarly, monthly SOFR futures consider a July cut quite unlikely, but now price nearly a full cut by the October expiry, showing strong confidence in a 25bps cut at the September FOMC. By December, the market is pricing 44bps of cuts, running ahead of the Fed’s one-cut prognosis.

The news is even better for the beleaguered and over-levered. If you listen closely, you can hear champagne corks clinking off the ceiling.

The Rotation

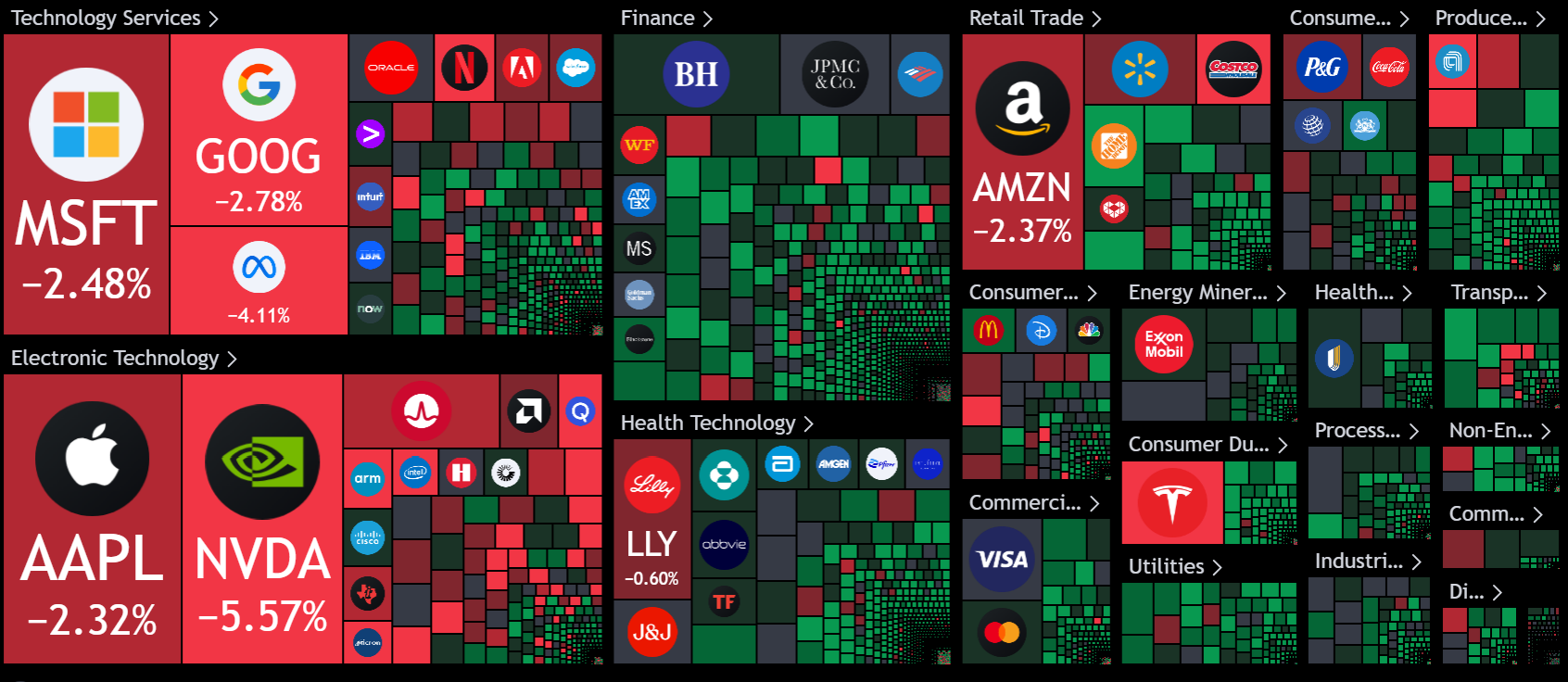

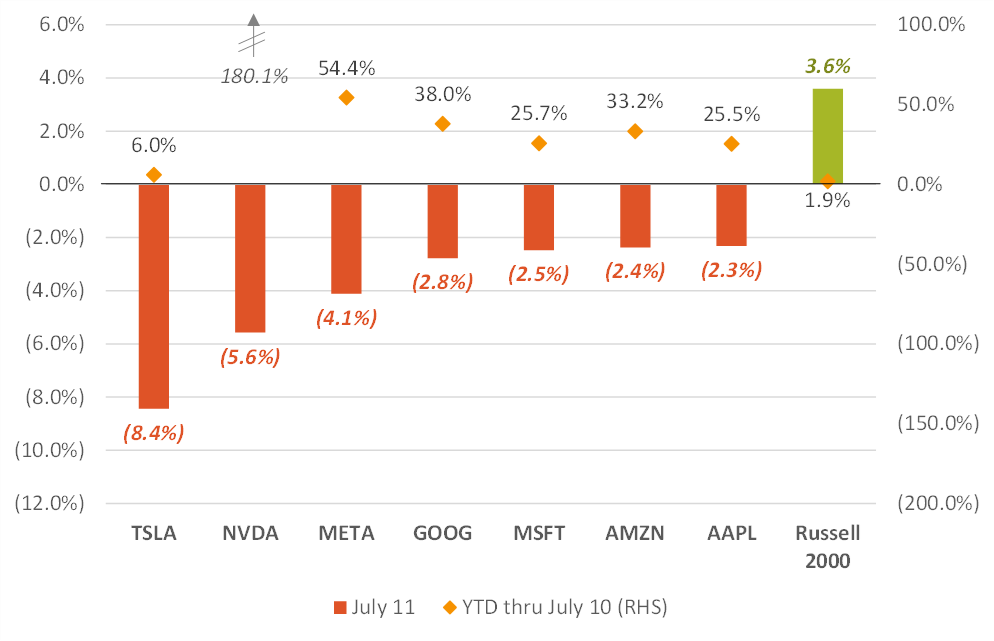

The market reaction in U.S. equities on Thursday was a defiant, even historic, trend reversal as investors dumped the Mag-7 and piled into small caps and rate sensitive sectors. The Russell 2000 surged 3.6% against a Nasdaq 100 flop of 2.2%, or a 5.8% relative outperformance in a single session — the largest gap in over twenty years. Across the market, equal-weighted indices trounced market-cap weighted counterparts.

And while the benchmark S&P 500 notched its worst decline since April, dragged down by the goliaths, the total market action can only be seen as bullish. Outside of mega-caps the market was quite literally a sea of green.