Rebound vs. Rally

#63: After recent outperformance, what's next for regional banks?

Regional Banks Rebounded

Cutting straight to the chase, we are pleased with the way our regional bank thesis has materialized. To recap, two weeks ago we made the case for an immediate opportunity in regionals based on the following points:

Regional banks have been among the worst performing stocks in the market following the failures of Silicon Valley Bank and First Republic

Despite legitimate headwinds, the blanket pessimism was overdone. Realtime data showed that banking conditions had continued to stabilize since March

2Q2023 earnings would provide a message of stability and a catalyst for a rebound from historically cheap valuations

Short covering would add fuel to a rally

We recommended the S&P Regional Banking ETF (KRE) and picked a basket of high quality banks that presented the most risk-averse path to play the thesis. Since the close of trading on Thursday, July 6th, each of these ideas has produced double-digit returns across ten trading sessions (11.2% - 17.9%), substantially outperforming the large-cap financial sector (XLF: 5.5%) and the broader market (SPX: 2.8%).

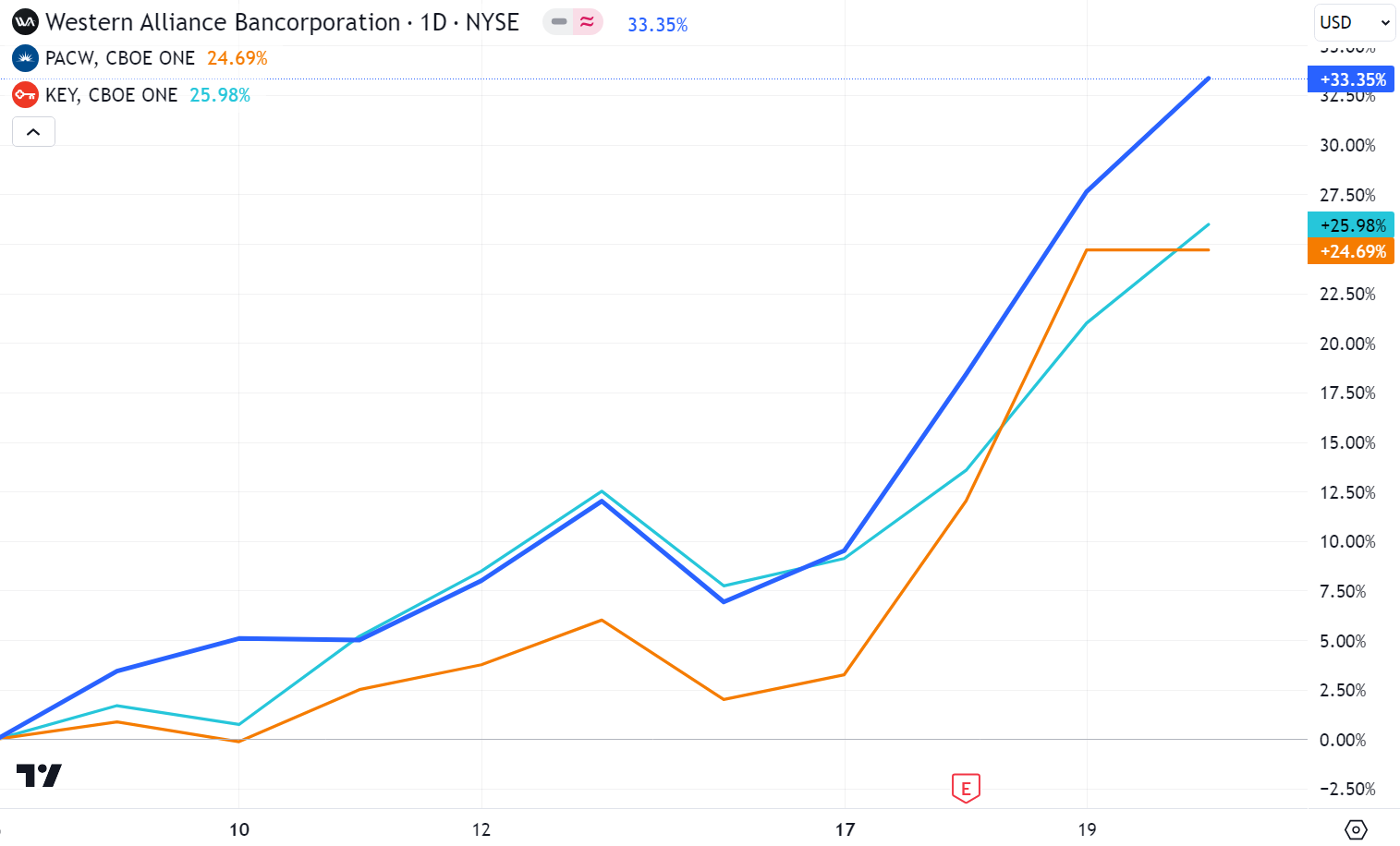

Existing momentum helped the case, but resilient earnings across the financial sector over the past week were necessary to validate the trend. Short covering also clearly provided a strong boost early this week, as popular shorts like Western Alliance (WAL), PacWest (PACW), and Keybanc (KEY) surged well higher than the broader regional bank index.

While these “high-beta” names lagged their peers heading into earnings, the massive surge this week - driven by Western Alliance’s strong results - put them ahead of the pack with outsized gains (24.7% - 33.4%).

With the benefit of hindsight, perhaps we didn’t go far enough. The rationale for picking high-quality individual names rather than the most downtrodden was to produce the best weighted-average outcome recognizing that a rebound was not guaranteed. In other words, we recommended banks that we’d be comfortable holding even if the short-term thesis did not materialize.

Yet, there is probably a lesson here - when you have a high conviction idea, sometimes it’s best to swing for the fences. Or, when buying the dip, buy the dippiest. All things considered though, it’s hard to nitpick.

In two weeks, KRE produced four years worth of returns of 10-year U.S. Treasuries at their current yield (3.8%) and came close to matching the heady YTD performance of the S&P 500 (18.6%). Even if we left meat on the bone, we didn’t leave hungry.

Now, will the winners continue to run?