Policy Error and Peak Liquidity

#97: FOMC recap, quantitative taper, and bubble watch.

For the peanut gallery, it was a two-fer.

There was a vanishingly small chance of any change to the Federal Reserve’s policy rate at Wednesday’s Federal Open Market Committee (FOMC) and, of course, no move was made. The effective Federal Funds rate holds at 5.33% for the sixth consecutive meeting, since the last hike in June 2023. A couple minor fidgets to the Summary of Economic Projections (SEP) was the only official change in the outlook.

Powell and the Plotters unsurprisingly held firm to their view that disinflation is intact. The spicy inflation data we have seen year-to-date is a product of new-year methodological adjustments and noise — a bump along the path to 2%. In response to increasingly incredulous questioning, Powell reiterated that financial conditions are indeed restrictive and doing their job to slow the economy. FOMC members, through their dot plots, confirmed their plans for rate cuts this year, and next, and next.

Little surprise, Powell testified to these dynamics just weeks ago in congress.

It was a two-fer, because talking heads got the chance to correctly predict the obvious rate decision, while also lamenting a perceived policy error in process.

To many hawkish observers, the Fed is simply sticking its fat head in the sand. How can disinflation be intact if the annual rate of change in CPI has risen over the past nine months, bottoming at the precise moment that the Fed stopped hiking? How is the supposedly data-dependent Fed choosing to ignore its own metrics like Median CPI or Core PCE Prices or National Financial Conditions or… in favor of its preferred narrative? Some invoked Arthur Burns.

Even in the typically stately press conference, there was a hint of tension.

Imagine an airplane, burning fuel as it circles its destination, desperate to touch its rubbery toes to tarmac. It was all finally coming together — the illusive, the vaunted, soft landing. Air-traffic and storm clouds have cleared and the nose has rotated back into alignment with the landing strip, but some damn yahoos are yelling to take another lap — conditions aren’t perfect, they say! Screw it, Powell is putting the bird down.

For the time being, I reserve judgement.

There is little doubt, in my mind, that the Fed’s own policy was central in creating the inflationary quagmire it now tries to escape. I acknowledge troubling signs that disinflation may have hit a wall. I also think the Fed’s bias towards accommodation (hot economy, hot inflation) and sluggishness to respond to inconvenient inflationary data is well established. But I appreciate the counters.

Relative to its initial forecast at the inflationary peak in 2022, the Fed remains ahead of schedule on delivering disinflation. And despite the recent hot prints, and the high likelihood that headline inflation increases again in March due to rising gasoline prices, I don’t see the conditions present that generated 9% inflation in the post-pandemic period, even if the 2% target remains elusive. And while nobody seems to have any real concern on the labor market, it is at least worth noting that unemployment at 3.9% has risen to the highest level in over two years. Finally, to the Fed’s credit, it has been fairly consistent in following through on its well-telegraphed plans, ignoring month to month fluctuations.

But to the stock market, the question of policy error is irrelevant. All that matters is that the rally has been blessed, yet again. Further, a policy error that favors inflation and growth is the markets’ gain. To reiterate some words from a recent post:

A charitable interpretation is that the Fed is correct, and inflationary concerns are simply misplaced. A less charitable interpretation is that the Fed simply prefers inflation to run above-target rather than risk recession. Either of these cases seem to bode well for equities.

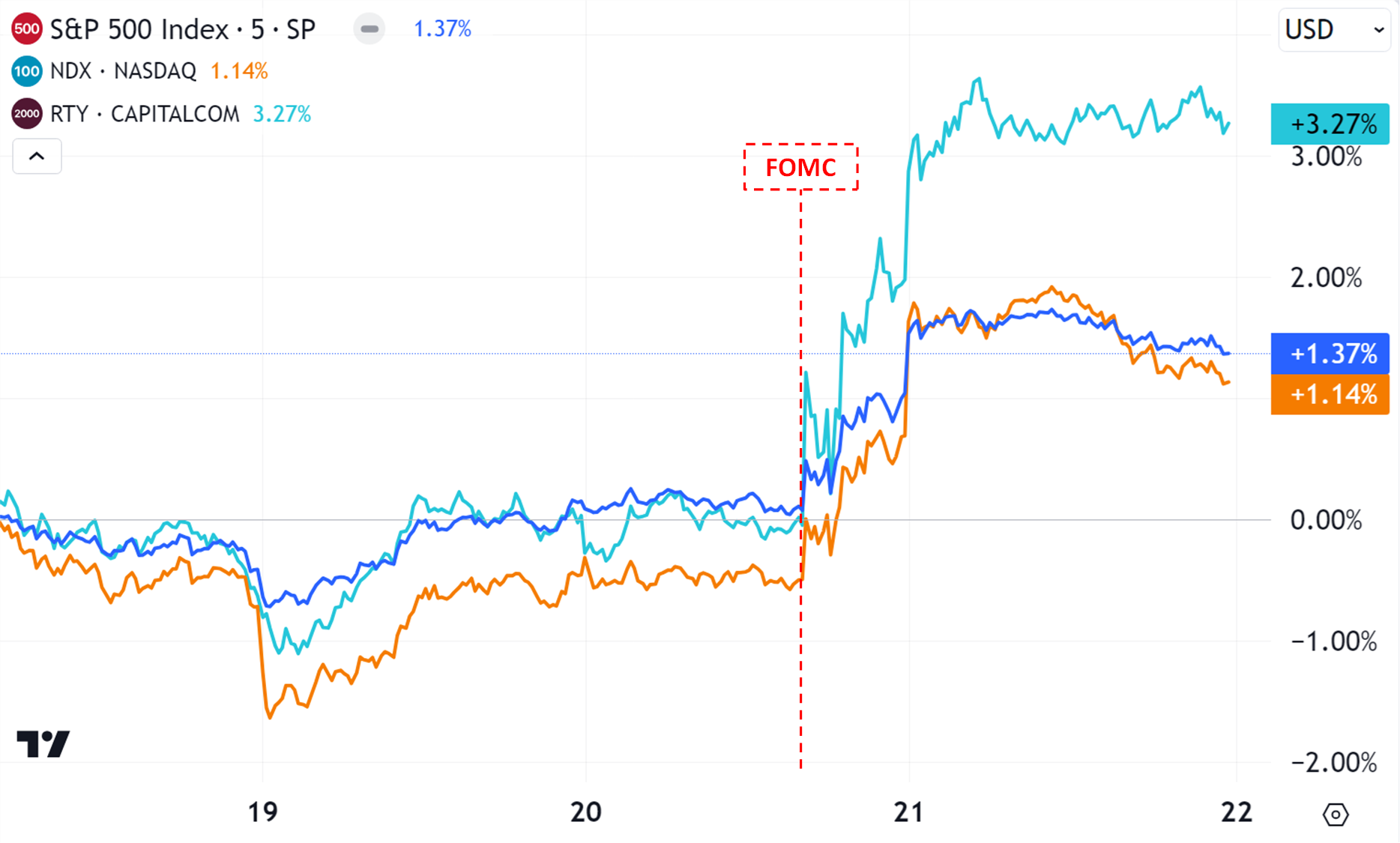

Stocks ripped as Powell waved the all-clear. While the S&P 500 and Nasdaq 1000 posted new records highs, small caps caught the biggest bid, which continued through Thursday’s session.

Meanwhile, the U.S. Treasury curve barely reacted to the event at all, apparently pre-pricing the non-event to perfection. Overall, yields drifted lower on the week.

On a longer-term scale, inflation agita has pushed rates higher since the turn of the year, but all things considered, rate-volatility has been muted and absolute yields remain well off the October 2023 highs.

Meanwhile, soft-dollar proxies bounced on the FOMC release, with gold briefly touching new highs.

For the time being, the 2024 playbook remains unchanged. The Fed is committed to easing. The curmudgeons and contrarians desperate to fight the Fed in the name of bubble-busting look on as puts are swallowed whole. So it goes.

There was, however, one legitimately new piece of information revealed in the post-announcement Q&A: Quantitative taper is coming.

Peak Liquidity and Quantitative Taper

Powell, in response to a reporter’s inquiry on balance sheet discussions, effectively announced that the Fed intends to slow the pace of quantitative tightening (QT) “soon” — a quantitative taper.