Generac Recharged

#64: After a pandemic boom and bust, what comes next for energy solutions company Generac Holdings (GNRC)?

Executive Summary

Generac Holdings Inc. (NYSE:GNRC) is a manufacturer of power generation systems, solar battery storage solutions, and other energy services. Its core products are standby backup generators for residential and commercial customers.

At face value, Generac is a fallen star of the pandemic bubble - a durable goods manufacturer that benefitted from cash-flush consumers and a massive home-improvement investment cycle. After posting 50% revenue growth in 2021, the company’s sales peaked in 2Q 2022 and have declined for three consecutive quarters. Lawsuits and product defects have further impacted sentiment.

Since October 2021, GNRC is down 70%, reducing its $31.9 billion market capitalization to $9.3 billion today.

But Generac is the dominant market player in the growing standby generator market and is a leading provider of battery backup systems. Its sales have grown at a 16% CAGR since its IPO in 2010. The recent financial downturn is set to reverse.

Grid Concerns Grow: Grid reliability is worsening due to increasing demand, aging infrastructure, changing generation mix, and severe weather. The frequency of power outages will continue to increase and drive demand for traditional backup power solutions.

Inventory Bullwhip: Recent financial results are heavily impacted by inventory overstocking in 2022 and de-stocking in 2023. End user demand is far more consistent and will continue to grow.

Narrative Rebound: The rebound in financial results in 2H2023 should help improve sentiment and build on the recent positive momentum in share price.

Smart Energy Solutions: Heavy investment in battery storage and smart grid products positions the company for growth in distributed energy solutions and protects against the risk of technological obsolescence.

In this piece, we cover:

Company Overview

Industry Drivers

Financial Performance

Valuation and Trading

Risks

Away we go…

Company Overview

Founded in 1959 and headquartered in Wisconsin, Generac provides power generation equipment, energy storage systems, energy management devices & solutions, and other power products serving the residential, light commercial, and industrial markets (84% domestic / 16% international).

Generac’s largest products are standby power generators for homes and businesses. The company dominates the industry with a 75% market share for residential products and strong positioning in commercial products (i.e. 60% market share within telecom). Generac also produces mobile and portable generators, as well as other power tools and mobile appliances.

The company distributes its products through a wide range of channels including the largest direct dealership network in the country (8,600), industrial distributors and dealers, national and regional retailers, e-commerce partners, electrical/HVAC/solar wholesalers, and others. No single customer accounts for more than 4% of sales.

More recently, the company has invested heavily in clean energy, battery storage, and smart-grid products, both through in-house R&D and 15 acquisitions since 2017 which have primarily focused on acquiring technology. These offerings include battery storage, solar optimization, EV charging, smart thermostats, load-management, and other monitoring services.

Generac competes in the home battery storage market with its PWRcell product (formerly Pika Energy), which compares against products offered by Tesla, Enphase, and SolarEdge. PWRcell provides the highest level of peak (12kW) and continuous (9kW) power on the market and has modular capacity from 9kWh - 18kWh of storage.

While these products currently represent less than 10% of total sales, they expand Generac’s product suite and help mitigate the risk of battery solutions replacing traditional fossil fuel generators over the long term.

Yet they also come with challenges. The company has been subject to lawsuits and warranty claims based on faulty components in its SnapRS solar product. Generally, rooftop solar and related services have proven to be a challenging business for many operators, despite growth in the market and environmental appeal.

Overall, Generac has a dominant market position and track record of growth in its core generator products, an advantaged and growing distribution channel, and a foothold in emerging technology.

Industry Drivers

Demand for its core products - standby generators - is driven by power outages and concern over grid reliability. Today, electric grids in North America are under pressure from increasing demand, changes to generation mix, severe weather, and aging infrastructure.

Electricity demand growth is picking up after two decades of declines due to increasing electrification of transportation, heating, and appliances. Projected growth rates of electricity peak demand and energy in North America are increasing for the first time in recent years.

At the same time, increasing penetration of intermittent renewable resources and the retirement of firm generation will add increased variability to the grid.

Meanwhile, severe weather makes it harder to plan for extreme conditions. From North America Electric Reliability Corporation’s (NERC) 2022 Long Term Reliability Assessment:

Extreme temperatures and prolonged severe weather conditions are increasingly impacting the bulk power system. Extreme weather impacts the system by increasing electricity demand and forcing generation and other resources off-line. While a given area may have sufficient capacity to meet resource adequacy requirements, it may not have sufficient availability of resources during extreme and prolonged weather events. Therefore, long-duration weather events increase the risk of electricity supply shortfalls. In many parts of North America, peak electricity demand is increasing, and forecasting demand and its response to extreme temperatures and abnormal weather is increasingly uncertain.

NERC classifies wide swaths of the country at elevated or high risk of resource inadequacy from 2023-2027.

Even if power outages do not come to fruition, headlines about grid vulnerability increase consumer’s awareness of power concerns and the desire to proactively insure against disruption.

While the grid is under strain due to supply and demand dynamics, most prolonged power outages are due to major events - hurricanes, winter storms, wildfires etc. - which inflict extensive physical damage to powerlines and other physical infrastructure.

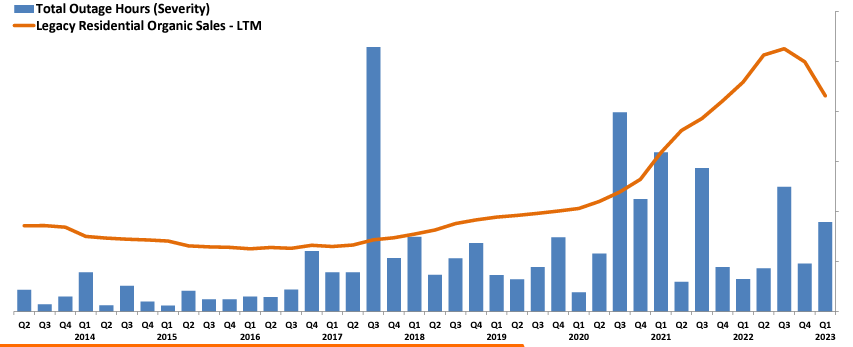

These major events make up the majority of power outages, and have increased over the past two decades (though with a high degree of variability from year to year). The EIA’s most recent data shows a growing trend over the past decade, driven by major events.

Generac’s quarterly data on outages is helpful in showing a growing baseline of outages, not merely occasional large events. Power outages in 1Q2023 were significantly elevated, supporting demand for backup solutions in the near term.

Meanwhile, increasing electrification of heating and transportation, combined with work-from-home means that consumers are more dependent than ever on reliable electricity. Businesses likewise are increasingly aware of the risk of power disruption and are investing in standby generators as a contingency plan. For example, telecommunication companies are increasingly putting standby generators on cell towers - a key market for Generac.

For major power outages, standby generators are a better solution than battery storage for most homeowners. A standby generator can run continuously for weeks at a time (assuming it is fueled) and can provide substantially higher wattage, supporting more energy intensive appliances. By comparison, a 12kWh battery cell can only power the average home for less than twelve hours (assuming a normal load) and costs twice as much as a significantly more powerful generator.

Battery storage paired with rooftop solar provides a better solution to longer term outages then a battery cell alone, depending on the solar irradiance of the region, the size of the array, and needs of the home. But for most consumers looking for a backup solution for a prolonged outage, both cost and reliability strongly favor standby generators. For businesses with larger power needs, generators are the only real alternative on the market today.

While different solutions fit different needs, both the battery storage and standby generator markets are growing. Today, most homes don’t have any source of backup power supply. Market penetration remains very low at only 5.75% (up from nearly zero in 2005), providing substantial room for ongoing growth.

Moving forward, distributed energy resources (DERs) such as rooftop solar, local battery storage, and smarter energy management will be a critical in addressing grid strain overall. Given their substantial recent investment in these products, Generac is poised to benefit from both the current struggles and future solutions for the energy grid.

Financial Overview

Generac’s recent financial performance paints a picture of rapidly deteriorating demand and shrinking margins. In 1Q2023, sales fell 22% from the prior year, driven by a 46% decline in residential sales. Likewise, margins shrank substantially over the past five quarters leading to a significant compression in earnings.

However, this significant drop in residential revenue is primarily a result of overstocked inventory channels and installation bottlenecks in 2022, rather than fading demand.

Generac sells products to its dealers and distributors who in turn sell to customers and provide installation. Given the rapid sales growth in 2021, the company increased production and achieved record sales into its distribution channels in 1H2022.

However, installation capacity could not keep pace with production capacity as dealers struggled with adequate labor and installation equipment. When combined with slowing demand growth (relative to 2021), field inventory ballooned throughout 2022, creating a significant headwind for new sales to distributors until the backlog of existing inventory cleared.

Field inventories peaked in 3Q2022, at roughly 2.0x normal levels. This excess inventory decreased to 1.7x by 4Q2022 and 1.4x by 1Q2023 as installations have outpaced new sales to distributors. Today, field inventory has likely normalized, removing this meaningful overhang.

Meanwhile, indications of end user demand remains strong. Installations in 1Q2023 were only down slightly year-over-year (compared to a 46% sales drop) which the company attributes to (ironically) severe weather limiting construction and an abnormally strong comparison period.

In-home consultations (IHCs) - a key sales lead figure - increased strongly in the first quarter of this year compared to both the prior quarter and prior year period while conversion rates also improved as lead times have shrunk. Strong sales momentum continued through April. Further, the dealership network grew by 500 dealers compared to the prior year, increasing the company’s footprint and installation capacity.

Outside of residential, Generac reported strong results in 1Q2023, as commercial sales grew 30%, its international sales rose 19%, and other services grew 32% (driven by acquisitions).

As a result, Generac anticipates a return to year-over-year revenue growth on a consolidated basis in 2H2023.

In addition to revenue headwinds, margins also compressed in 2022 driven primarily by higher raw input and logistics costs and lower sales volumes given the inventory glut. Gross profit margins fell from 36.4% in 2021 to 33.3% in 2022, while Adjusted EBITDA margins fell from 23% to 18%.

But 1Q2023 marked the low point in margins. The company expects margins to improve substantially into the second half of the year based on higher selling prices, reduced input costs, and higher sales volumes.

The midpoint of 2023 full year guidance implies $4.2 billion of revenue and $735 million of Adjusted EBITDA. Yet both of these figures understate the underlying run-rate of the business given the inventory headwinds through the first half of the year. To the extent that the company achieves 10% revenue growth through 2024 (which should be achievable given the weak comparison) and maintains its expected year-ending margins of 20%, it will post a new record Adjusted EBITDA well over $900 million next year.

Valuation and Trading

With a market capitalization of $9.2 billion and enterprise value of $10.6 billion, Generac appears attractively priced on a forward EPS or EV/EBITDA basis, when considering its growth rate, leading market share, and diversified product offerings.

After falling over 80% from its peak in late 2021, the stock found a floor around $100 - a level that I think is firmly supported by the underlying valuation. Since its 1Q2023 earnings, which confirmed its guidance for a second half rebound and provided upbeat data on end-user demand, the stock has rallied 47% from $102 to $148.

If the company’s financial performance is turning the corner, sentiment on the stock appears to be as well.

Generac reports its 2Q2023 earnings before market open this Wednesday, August 2nd. Beyond its financial results, positive comments around field inventory levels, sales leads, and margin outlook could be meaningful catalysts.

Risks

Legal Contingencies: Generac is facing multiple lawsuits, including a product liability claim from Power Home Solar and several putative class actions alleging warranty breaches related to their new energy products (worrisome) and securities law violations (less worrisome). Generac also received a grand jury subpoena regarding a DOJ investigation into their emissions regulation compliance for a small number of portable generators (small but worrisome).

Weather Variability: Even if severe weather events are increasing on average, they are inherently unpredictable and highly variable. During periods of grid stability, demand for generators may fall.

Macroeconomic Conditions: Standby generators are a major durable goods purchase, often exceeding $10,000 with installation costs. Weakening economic conditions or consumer sentiment would negatively impact product sales, other things equal. Note: revenue was flat from 2007 - 2009, which is better than one might assume.

Technological Evolution: Improvements in battery storage technology and cost could increase suitability as a backup power solution and impact demand for traditional generators. While Generac competes in these markets, it is unlikely to capture the market share it enjoys in traditional generators.

Conclusions

Generac’s financial and market performance experienced a pandemic boom and bust. But the underlying demand for the company’s products have grown consistently over the past two decades and is likely to continue.

Today’s trading price is supported from a fundamental valuation perspective and a turnaround in company performance should improve sentiment. While not without risk, momentum now favors the upside and the stock may continue appreciate.

Thank you for subscribing to The Last Bear Standing. If you like what you’ve read, hit the like button and share it with a friend. Let me know your thoughts in the comments - I respond to all of them.

As always, thank you for reading.

-TLBS