Gems in the Junkyard

#98: Seven de-SPACs to keep your eye on.

Few financial vehicles have incinerated shareholder value quite like the modern SPAC. Or, more precisely, the de-SPAC.

(For background, a Special Purpose Acquisition Company or SPAC, is a publicly traded shell company that exists for the purpose of finding a private company and bringing it public. The private company merges with SPAC in a “de-SPAC” transaction, and steps into the SPAC’s existing public listing. This is a convenient backdoor into public markets, avoiding the pesky oversight and regulations that come with an Initial Public Offering.)

This comes as no surprise. The primary beneficiaries of the SPAC boom — when 861 SPACs went public from 2020-2021 — were the insiders who reached the exit liquidity of public markets and bankers who made fees along the way. Since the peak in February 2021, a broad index of de-SPACs has fallen 91%. Most of these companies are destined for the dustpan — hundreds have already been delisted.

But a select few — HIMS or GRND, for example — have risen from the ashes, delivered on business projections, and rewarded investors. It stands to reason that there are more out there, and this week I tried to find them.

I screened hundreds of de-SPACs that are trading below their initial merger price, looking for some combination of growth, profits, valuation, and share-price momentum. Most were crap, but some warrant further consideration.

The seven that I outline below cover a range of industries — software, consumer products, healthcare, fintech, transportation — but have some common threads. They are growing and have either recently turned a profit or have a defined path to profitability. On average, they have already rebounded 160% off their all-time lows, but remain 51% below their initial $10.00 SPAC price1. Several have made meaningful pivots in sales channels or end markets that seem to be underappreciated.

But these aren’t blue-chips. They are generally small, risky, and have much left to prove.

Of course, all the typical caveats apply — this is an idea ticklers, not investment advice. All the data is sourced from the companies’ public filings and forward projections are per management guidance.

Without further ado…

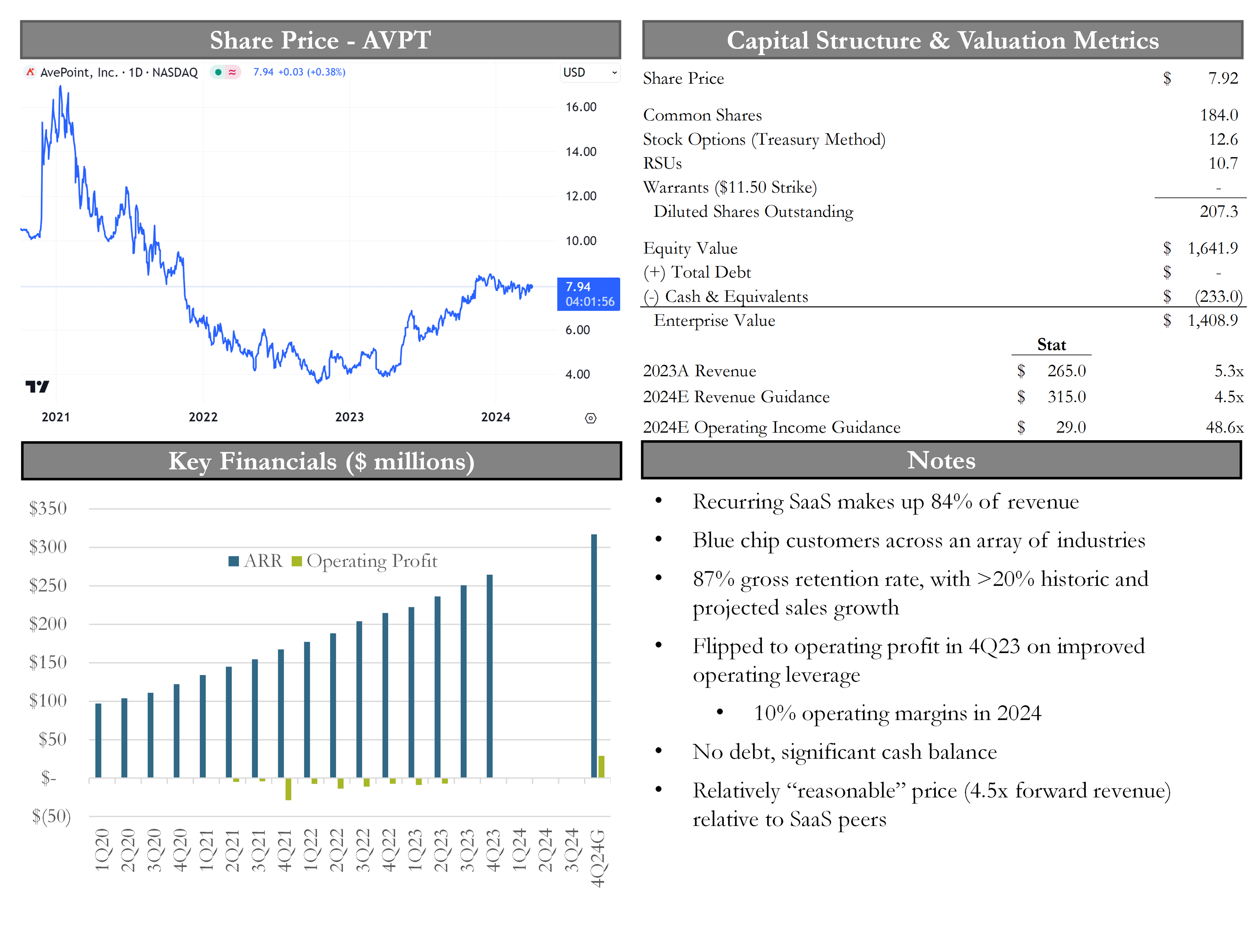

AvePoint, Inc (Nasdaq: AVPT)

Why? AvePoint, a data-management enterprise software company, stands out as one of the few legitimate SaaS companies that has entered the market via SPAC. It has one of the most consistent track records of revenue growth to boot. A blue-chip customer list and consistent retention statistics provides some reassurance of the quality of product. AVPT has no debt, a meaningful cash balance, and is flipping to profitability as it gains operating leverage against its overhead and sales & marketing costs. Its annual recurring revenue (ARR) is expected to grow 22% in 2024 — consistent with its historical trend. At 5.3x EV/LTM revenue and 4.5x forward revenue, it screens much cheaper than many SaaS peers with similar growth rates.

Why Not: Product relevance and competitive risk. It may seem expensive on an absolute basis, but hey, it’s SaaS.