Big Fiscal, Big Funding, and Buybacks

#65: As fiscal spending propels the economy, Treasury issuance clouds markets.

Big Fiscal

Last week, the Bureau of Economic Analysis released its preliminary 2Q2022 GDP figure showing 2.4% real growth, well ahead of consensus estimates for a 1.8% gain. This sturdy figure is merely the latest upside surprise in economic data in 2023.

While growth was driven by both public and private gains, the rebound in government expenditures has continued to play a meaningful role in economic growth over the past year. Direct increases in government consumption and investment have contributed 26% of GDP growth over the last four quarters. Major subsidies have also helped promote private investment dollars, meaning that the true impact of government spending is understated.

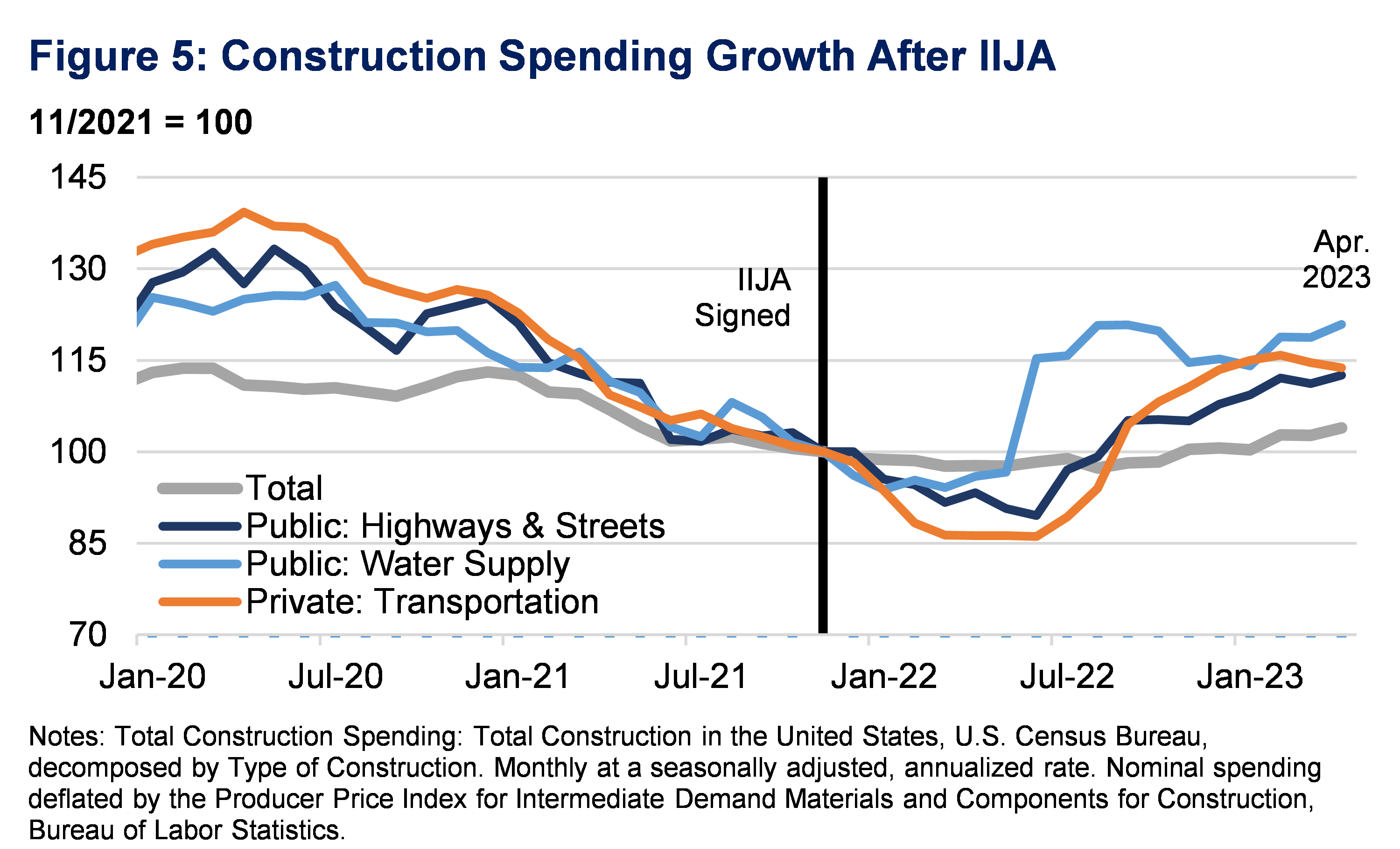

The rebound in government spending has helped stabilize slowing private economic activity and the effects of tightening monetary policy. In particular, three major investment-focused spending packages have kicked into gear, providing uplift to the economy, as shown in a recent U.S. Treasury report.

The broadly bi-partisan Infrastructure Investment and Jobs Act (IIJA), signed in November 2021, provided up to $715 billion in new spending for federal-aid highway, transit, highway safety, motor carrier, research, hazardous materials, and rail programs of the Department of Transportation. Public spending on water supply and roadways has increased 20% and 13% respectively, while private transportation spending has also rebounded.

Meanwhile bi-partisan CHIPS and Science Act (CHIPS Act) signed in August 2022 provided roughly $280 billion in new funding to boost domestic research and manufacturing of semiconductors in the United States. While semi manufacturing was rapidly accelerating prior to CHIPS, it was supercharged by the legislation. Subsidies help to spur private investment and boost the private component of GDP figures as well (the graph below only includes private construction).

Finally, the contentious budget reconciliation bill, the Inflation Reduction Act (IRA) signed in August 2022, authorized $891 billion in new discretionary spending to subsidize clean energy and healthcare costs, while also increasing government revenues through a number of means. While the effects of the IRA are less obvious in a single chart, these provisions encourage renewable energy investment at the utility scale while spurring consumer demand through subsidies for EVs, electric pumps, etc.

“Big Fiscal” is a major factor in today’s economic resilience. Meanwhile, inflation continues to subside.

Taken together, the narrative on fiscal spending has shifted dramatically. Last year, excessive fiscal spending was seen as a key driver of inflation. Today fiscal spending is heralded as a prudent counterforce to constrictive monetary policy.

But the notion that government spending can boost GDP is not novel. Nor is all fiscal expenditure created equal. The effect of fiscal stimulus depends in part on what it buys and how it is funded.

COVID provided a grand experiment in direct demand-side stimulus, funded by monetary expansion. In other words, the Federal Reserve printed money and the Treasury handed it out. While highly effective at immediately spurring consumption, the economy gained little in new productive capability - at least not directly. Instead, more money chased the same number of goods, driving up prices. The initial gain in spending power was quickly reduced in real terms.

By contrast, infrastructure spending helps drive economic growth by circulating savers’ money in the economy, while building productive assets in the process. Factories, power plants, roads, or bridges will provide some sort of return on investment in future economic activity. Even if the net benefit does not justify the total cost in the long run, there is at least some productive return.

Importantly, the Fed did not finance these more recent infrastructure investments with new money as it did (indirectly) with COVID stimulus. Rather, funds were raised by federal borrowing from the existing supply of money, which continues to shrink with quantitative tightening.

These key distinctions help differentiate the economic and inflationary impact of fiscal spending.

Big Funding

Yet “Big Fiscal” is also a bit of a misnomer. Real government expenditures and investment as a percent of real GDP has been declining since the 1950s, from well over 30% to under 20% over the past decade.