All Dogs Go to Heaven

#113: Will NextEra Energy Partners LP (NEP) be the next to ascend?

Somewhere along the line, someone got a bright idea.

Let’s say you are a big oil company. Your company has all kinds of variability and risk — cyclical exposure, commodity price risk, capex variability, and so forth — and so your stock trades at a measly 8.0x EBITDA. But not all your assets are risky. Within this big conglomerate there are really good stable assets! You have all these boring pipelines and infrastructure with reliable cash flow that are surely undervalued, hidden in your massive enterprise.

On their own, these stable assets provide reliable cash flow and equity investors should clamor at the chance of getting a piece of these stalwarts and pay you a premium for the opportunity. And it just so happens that such assets qualify for inclusion under a unique partnership structure - a Master Limited Partnership or MLP - that like REITs are exempt from partnership level taxes, an added bonus.

So the parent company, Oil Co (OC), creates Oil Partners LP (OCP), bestowing it with some initial assets and floating a portion of the limited partner (LP) units to the public. Oil Co, which trades at 8x, sells assets at a 10x purchase price to OCP, which itself trades at 12x, in what’s called a “dropdown” transaction. With the dropdown purchase price falling between the two public trading multiples, the deal is accretive to both OC and OCP. Oil Co has successfully opened a new, cheaper financing channel while investors in Oil Partners LP receive the prospect of growing distributions and a backlog of new acquisition opportunities from the parent. Magic!

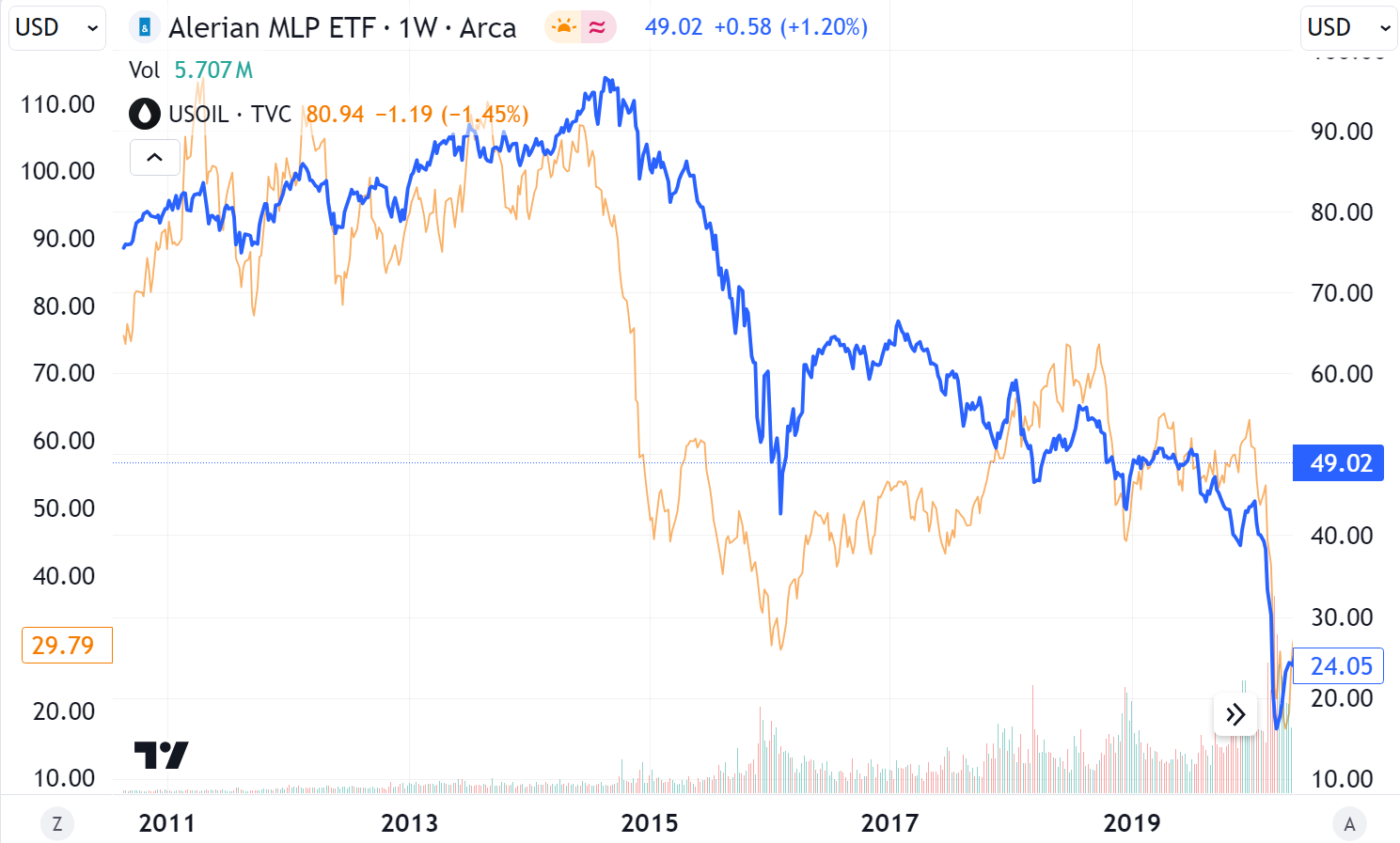

In the early 2010s, the shale boom brought sudden growth and wholesale changes to United States onshore oil & gas infrastructure. With it, came the MLP boom. In the heyday, several new MLPs were debuting on public markets every single week and there were plenty of investors eager to get a piece of both the distributions and growth that such vehicles promised. (As the industry expanded, so too did the definition of “stable” and “high quality” assets).

But these MLPs — financial engineering at their core — were more complicated than the simple dropdown arbitrage described above. Akin to the “teaser rates” in home mortgages in the 2000s, most MLPs were structured with Incentive Distribution Rights (IDRs), which meant that at the outset, common unitholders would receive 98% of cash distributions. But as the partnership’s distributions grew, more and more of the cash would flow back towards the parent company. Eventually, half of the partnership’s distributions would be skimmed by the parent company rather than flow to the MLP’s limited partners.

The early distribution growth rates which teased investors and initially allowed for cheap equity capital eventually ran into the overwhelming drag of IDRs. The cost of capital quickly ratcheted higher, breaking the dropdown arbitrage opportunity.

To fix the issue, many MLPs were forced to buy out these IDRs, with the partnership paying the parent to eliminate the preferential structure. Investors’ growing recognition of the structural challenges, combined with the massive oil slump from 2014 - 2016, reduced the appeal of the MLP and the trading premium critical to their purpose.

Before long, the bright idea of the MLP dimmed. No longer did they provide attractive financing for the parent nor bright growth prospects for investors, and so there was very little reason for their existence at all. Keep in mind that such “partnerships” are paper constructs — a slew of agreements determining ownership, control, and cash flow waterfalls, with little practical impact on the assets actual use within the parent’s wider operations.

And so, the MLP IPO boom was followed by a wave of consolidation. Parents absorbed their children, offering stock or cash consideration to public unitholders. The great financial engineering came full circle back to the status quo. And it just so happens that with a broken growth model depressing MLP unit prices, the acquisitive parents were buying back their own assets on the cheap.

Of the many MLPs born in the last decade, few still exist today. Data from VettaFi shows the number of publicly traded North American midstream companies falling from 83 in 2015 to just 35 in 2023, driven by the consolidation of MLPs.

But some still stand — for now. Of note, NextEra Energy Partners LP.

NextEra Partners

NextEra Energy Partners LP (NEP) debuted to public markets in 2014 as an offshoot of its parent NextEra Energy (NEE). An outlier in the MLP sphere, NextEra is unique as an electric company (rather than oil and gas), with both a regulated utility and renewables-focused power generation assets nationwide.